Annuity Proposals Explained: 4% Rule vs. a 7% Lifetime Guarantee

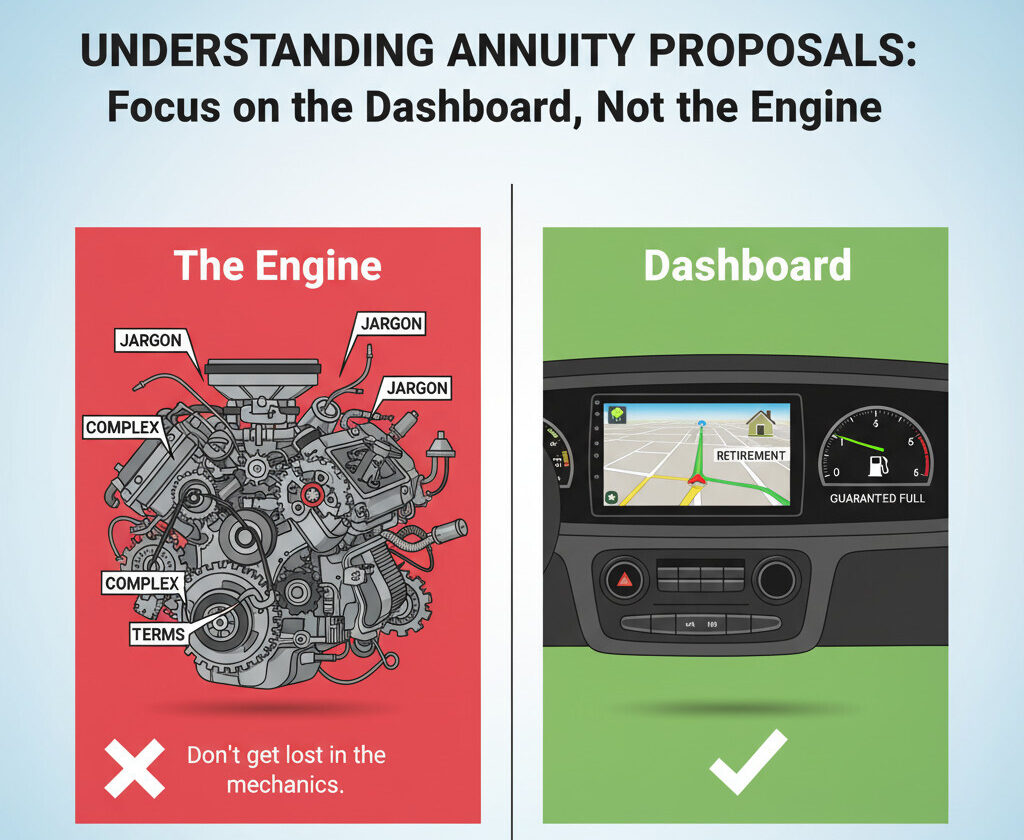

Let’s be honest, for most of us, seeing an “annuity proposal” is about as exciting as reading a car’s engine manual. It’s filled with jargon, confusing tables, and numbers that don’t always seem to add up. You’ve probably heard the fear-mongering—”it’s too complex!” or “you’ll lose your money!”—and it’s enough to make you just stick your money under a mattress.

But here’s a little secret: you don’t need to understand a car’s engine to drive it. The same is true for an annuity. You don’t need to be a financial wizard to understand what it *does* for you. An annuity is built for one thing and one thing only: to create a guaranteed paycheck for the rest of your life. Today, we’re going to tear down a real proposal, piece by piece, so you can see exactly how it works and decide if it’s the right “vehicle” for your retirement. 😊

What’s the “Engine”? (And Why You Don’t Need to Know) 🤔

When you’re shopping for a car, you’re probably focused on a few key things: What’s the gas mileage? How many seats does it have? What’s the safety rating? You’re not typically asking the dealer to explain the precise mechanics of the fuel injection system.

We’re taking that exact same approach here. We’re going to stay in the “driver’s seat” and focus on the three things that actually matter to you, the consumer:

- Money In: How much are you investing?

- Income Growth: How does your future paycheck get bigger while you wait?

- Money Out: How much are you *guaranteed* to get back, and for how long?

That’s it. Forget all the complicated stuff “under the hood.” Let’s focus on the dashboard.

The $100,000 Test Drive: A Real-World Simulation 🚗

Enough with the theory. Let’s make this real. We’re going to walk through a case study with a real $100,000 investment.

Meet our hypothetical investor, we’ll call him Mr. Hong.

- His Age: 56 years old.

- His Investment: A one-time lump sum of $100,000.

- His Goal: He doesn’t want to touch this money for 10 years. Then, at age 66, he wants to flip a switch and get a guaranteed paycheck that he absolutely cannot outlive.

When Mr. Hong gets his proposal, he sees a table with a bunch of columns. While they might have slightly different names, they almost always show these three key values:

- Account Value (or Cash Value): This is your “walk-away” money. It’s the actual cash value of your policy, which might go up or down based on market performance (if it’s a fixed index or variable annuity). This is *not* the number used for your lifetime income.

- Income Base (or Payout Base): This is the “magic number.” It’s a separate, special number used *only* to calculate your future paycheck. It typically grows at a guaranteed, high rate.

- Guaranteed Withdrawal: This is the “dashboard.” It’s the actual dollar amount the company promises to pay you every year for life.

The single most important column to watch, the one that makes this whole thing work, is the Income Base.

The “Magic Number”: How Your Income Grows 📈

So, what is this “Income Base” and why is it so special? You can think of it as a special calculator that the insurance company gives you. For those 10 years that Mr. Hong is patiently waiting (from age 56 to 66), the company gives him a rock-solid, contractual promise.

In this real-world example, his $100,000 Income Base is guaranteed to grow by 7.2% compounded every single year. No matter what the stock market does. If the market crashes, his Income Base still grows by 7.2%. If the market is flat, it still grows by 7.2%.

Now, this next part is the most important concept in this entire article. Please read it twice.

This is the #1 thing people get wrong. The Income Base is not your money. You cannot walk away with it. It is not your cash value.

Think of it this way: The Income Base is just a calculator. It’s a special, separate number that grows at a high, guaranteed rate for one reason and one reason only: to determine the size of your future, lifelong paycheck. Its only job is to get as big as possible so your future income is as big as possible.

Let’s see the power of this. Mr. Hong’s initial $100,000 Income Base just chugs along, compounding at that guaranteed 7.2% for 10 years. By the time he’s 65 (at the end of the 10th year), his “magic number” has grown to just over $200,000.

Now, that $200,000+ number is going to fuel his income for the rest of his life.

The Payout: 4% “Rule” vs. 7% *Guarantee* 📊

Mr. Hong is now 66. His Income Base is over $200,000. So what? How does that turn into actual cash in his bank account?

Now we get to the best part: the payout phase. Here’s the big reveal: based on that Income Base, Mr. Hong is guaranteed to receive $14,000 a year. Every single year. For the rest of his life.

It doesn’t matter if he lives to be 90, 100, or 110. That $14,000 check keeps coming. That’s the promise.

How did they get that number? The math is actually really simple. The company takes his final Income Base (let’s say it’s $200,400) and multiplies it by a Payout Rate that’s *also* guaranteed in his contract. For his age (66), that rate is 7%.

📝 The Payout Formula

Final Income Base × Guaranteed Payout Rate = Lifelong Annual Income

$200,400 × 7.0% = $14,028 per year (for life)

But you might be thinking, “Is 7% any good?” Well, let’s compare it to one of the most famous rules of thumb in all of retirement planning: the 4% Rule.

The 4% Rule is a guideline suggesting that if you withdraw 4% from your investment portfolio (like a 401k or stock account) each year, you have a *high chance* of your money lasting for about 30 years. But as you can see, it’s a world of difference.

Comparing the Payouts

| Feature | The 4% Rule | Annuity Guarantee (This Example) |

|---|---|---|

| Type of Payout | A “rule of thumb” or guideline. | A legal, contractual guarantee. |

| Market Risk | 100% subject to market risk. (A crash can ruin it). | Immune to market risk. The check is guaranteed. |

| Duration | Designed to last *about* 30 years. | Guaranteed for your entire life. |

| Payout Rate | ~4% (of your *actual* cash value) | ~7% (of your *Income Base*) |

Answering the Big “What Ifs” (Addressing Your Fears) 🛡️

A lifetime paycheck takes care of the fear of *running out of money*. But life throws other curveballs, right? A good annuity also builds in protection against the other really big “what ifs” in retirement.

What if I get sick and need long-term care?

This is a big one. What happens if you get really sick and are suddenly facing those huge costs for long-term care? Well, this annuity has a feature built-in, often called a “multiplier.”

Check this out: If Mr. Hong gets sick and can’t do a couple of basic daily activities on his own (like bathing or dressing), his income can literally double. That’s right. His paycheck goes from $14,000 a year to $28,000 a year. This provides a massive financial cushion to help pay for care, and those bigger payments usually last until his original investment has been paid back to him.

What if I die early and “lose” my investment?

This is, without a doubt, the number one fear people have about annuities. “What if I put my $100,000 in and get hit by a bus a year later? Does the insurance company just keep all my money?”

Let me be crystal clear: Absolutely not.

Modern annuities have a death benefit for this exact reason. If you pass away, the company just does some simple math: They take your initial investment and subtract whatever income payments they’ve already sent you. The rest, whatever is left, goes straight to your family—to your beneficiaries.

Your initial investment is not lost.

Example: The Death Benefit in Action 📝

- Situation 1: Mr. Hong dies after 1 year (receiving one $14,000 payment).

- Calculation: $100,000 (Initial) – $14,000 (Paid) = $86,000.

- Result: His family gets a check for $86,000.

- Situation 2: Mr. Hong dies after 5 years (receiving $70,000 in payments).

- Calculation: $100,000 (Initial) – $70,000 (Paid) = $30,000.

- Result: His family gets a check for $30,000.

His family is guaranteed to get back *at least* his entire initial investment, either through his income payments or a combination of income and the death benefit.

The Final Verdict: Is It a Good Product? 🛣️

Okay, we’ve gone through the whole thing: the numbers, the guarantees, and the “what ifs.” This lands us at the big question: Is this thing actually a good product?

The answer, like most things in finance, is that it’s a trade-off.

This product is NOT for someone who’s trying to swing for the fences and get the highest possible returns in the stock market. You are trading away some of that high-risk, high-potential upside.

This product IS for someone who has decided they want to take a chunk of their savings and turn it into a predictable, worry-free, guaranteed paycheck that they can *never* outlive. You are buying certainty. You are buying peace of mind.

At the end of the day, it all comes down to this one question. When you think about your retirement, what do you value more: the potential for maximum returns (which always comes with risk) or the guarantee of lifetime income?

That choice is up to you.

Annuity Proposals: Key Summary

Frequently Asked Questions ❓

I hope this deep dive helped clear up the fog! By focusing on the “dashboard”—what you’re guaranteed to get—you can make an informed decision without needing an engineering degree in finance. If you have any more questions, feel free to ask in the comments~ 😊