2025 U.S. Tax Outlook

2025 U.S. Tax Outlook: TCJA Sunset and Business Tax Implications

1. The “Tax Cliff”: Impact of TCJA Provision Expirations

Unless Congress acts, many temporary tax changes from the TCJA are scheduled to expire on December 31, 2025. If these provisions sunset, U.S. tax law will largely revert to pre-2017 rules, potentially leading to broad tax increases.

Impact on Individual Taxpayers

- Marginal Tax Rates: The current seven-rate structure (10%–37%) would revert to the pre-TCJA structure (10%–39.6%) with different income brackets.

- Standard Deduction: The nearly doubled standard deduction amounts would be significantly cut, returning to pre-TCJA levels.

- Personal Exemptions: The personal exemption, suspended under TCJA, would be reinstated.

- Child Tax Credit (CTC): The maximum credit would decrease from $2,000 to $1,000 per child.

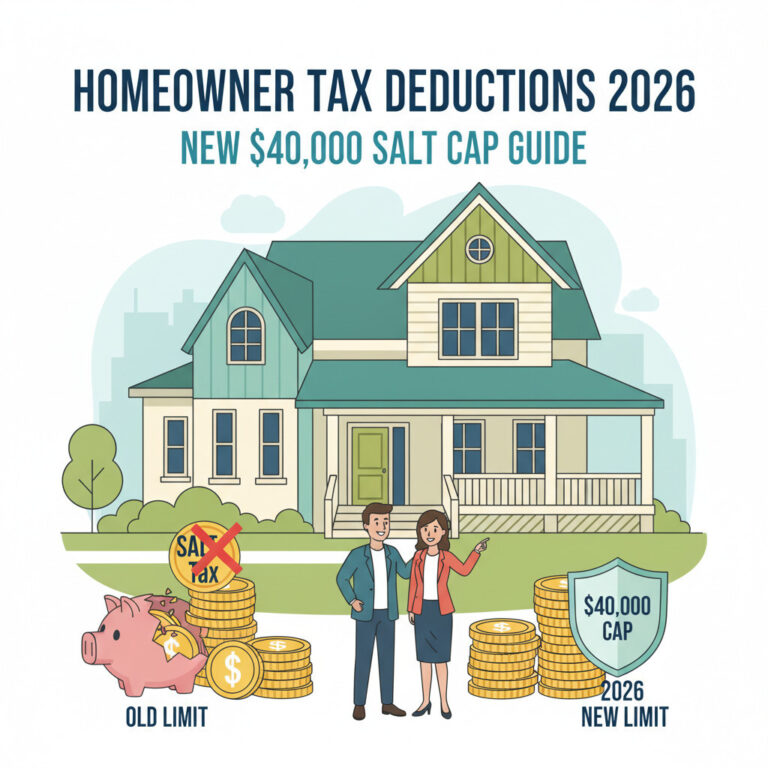

- State and Local Tax (SALT) Deduction: The $10,000 cap on itemized deductions for state and local taxes would expire, potentially allowing full deductions.

- Miscellaneous Itemized Deductions: Suspended deductions subject to the 2% AGI floor would be reinstated.

- Alternative Minimum Tax (AMT): AMT exemption amounts and phase-out thresholds would revert to lower pre-TCJA levels, potentially subjecting more taxpayers to AMT.

- Student Loan Debt Forgiveness: Federally forgiven student loan debt could become taxable income after 2025.

Implications for Businesses and Pass-Through Entities

- Section 199A Qualified Business Income (QBI) Deduction: This deduction, allowing up to 20% of qualified business income for many pass-through entities, is scheduled to expire, meaning this income would be taxed at ordinary individual rates without this significant deduction.

- Estate Tax Exclusion: The doubled estate and gift tax basic exclusion amount will revert to pre-TCJA levels (a $5 million base indexed for inflation), significantly impacting succession planning for family businesses and farms.

- Bonus Depreciation: While already phasing down, it will reach 0% after 2026 under current law.

The expiration of these TCJA provisions creates unprecedented planning uncertainty, making multi-year financial projections difficult.

2. Proposed Tax Legislation and Potential Reforms for 2025

The impending TCJA sunset has spurred discussions on new tax legislation. Understanding these proposals is crucial for anticipating the future tax landscape.

Potential Trump Administration Proposals

A potential second Trump administration would likely focus on making most TCJA tax cuts permanent, particularly business tax breaks. Key elements include:

- SALT Cap Alteration: Discussions include potentially altering the $10,000 SALT cap, with proposals for a $30,000 or $40,000 cap.

- Section 199A QBI Deduction: Proposals include increasing the QBI deduction from 20% to 23% and making it permanent.

- Business Tax Provisions: Making current rates for GILTI, FDII, and BEAT permanent at 10.5%.

- Tariffs as an Offset: The use of “reciprocal tariffs” to generate revenue, potentially offsetting the cost of extending TCJA provisions.

Elements from Past “Build Back Better” (BBB) Framework

While not enacted, some BBB proposals could resurface:

- SALT Deduction Cap: One proposal aimed to increase the cap to $40,000 with a phase-down for higher incomes, and to disallow certain state-level pass-through entity tax (PTET) “workarounds”.

- Business Interest Deduction: Proposed changes to redefine Adjusted Taxable Income (ATI) to be based on EBITDA, generally increasing the deduction.

- Section 199A QBI Deduction: Proposals also included making the QBI deduction permanent and increasing it to 23%.

These contrasting proposals highlight divergent tax policy philosophies, indicating significant tax changes are probable regardless of which political party holds power. This volatility makes long-term financial planning exceptionally difficult.

3. Special Considerations: Disaster Relief and Taxpayer Assistance

The IRS offers various tax relief measures for taxpayers affected by federally declared disasters. For example, victims of the California wildfires that began January 7, 2025, received an extension until October 15, 2025, for various individual and business tax returns and payments. This relief covers numerous deadlines, including individual income tax returns, estimated tax payments, and quarterly payroll returns.

Qualified wildfire relief payments for uninsured losses are generally excluded from gross income. Taxpayers in covered disaster areas typically receive this relief automatically. However, if a penalty notice is received, taxpayers should call the IRS to have it abated.

Reconstructing records after a disaster is crucial. All taxpayers should practice robust record-keeping, including regular off-site or cloud-based digital backups, to safeguard financial information.