Can I Claim Relatives from Abroad on My Taxes? A Complete Guide

Have you ever found yourself in this situation? You’re working hard in the U.S., and you’ve finally brought your parents or other relatives over to live with you. You’re supporting them, paying for their food, housing, and medical bills. As tax season approaches, a huge question pops into your head: “Can I claim them as dependents?” It seems only fair, right? But the rules, especially for non-citizens, can feel like a tangled mess. I’ve seen so many people leave thousands of dollars on the table because they just assumed it wasn’t possible. Well, let’s untangle this together and find out what you’re *really* entitled to! 😊

Why Bother? The Real Money You Save with Dependents 💰

First off, let’s talk about *why* this is so important. Claiming a dependent isn’t just about ticking a box; it’s about unlocking some of the most significant tax breaks available. We’re talking about real, tangible savings that can make a huge difference to your bottom line.

For starters, if you’re single, claiming a dependent could potentially allow you to change your filing status from “Single” to **”Head of Household.”** This one change is massive. It gives you a much larger standard deduction and wider tax brackets, meaning more of your income is taxed at lower rates.

But that’s not all. Dependents are your ticket to valuable tax credits. And remember, credits are *way* better than deductions. A deduction just lowers your taxable income, but a credit reduces your actual tax bill, dollar-for-dollar.

- The Child Tax Credit: If your dependent qualifies as a “Qualifying Child” under 17, this could be worth up to $2,000 per child (partially refundable).

- The Credit for Other Dependents: This is the big one for relatives who aren’t your young children (like parents, nieces, or older kids). This is a non-refundable credit worth **$500 per dependent**.

Add all this up—a better filing status, a $500 credit for your mom, a $500 credit for your dad, and maybe even a Child Tax Credit for a niece or nephew—and you can see why I said you could be missing out on *thousands*.

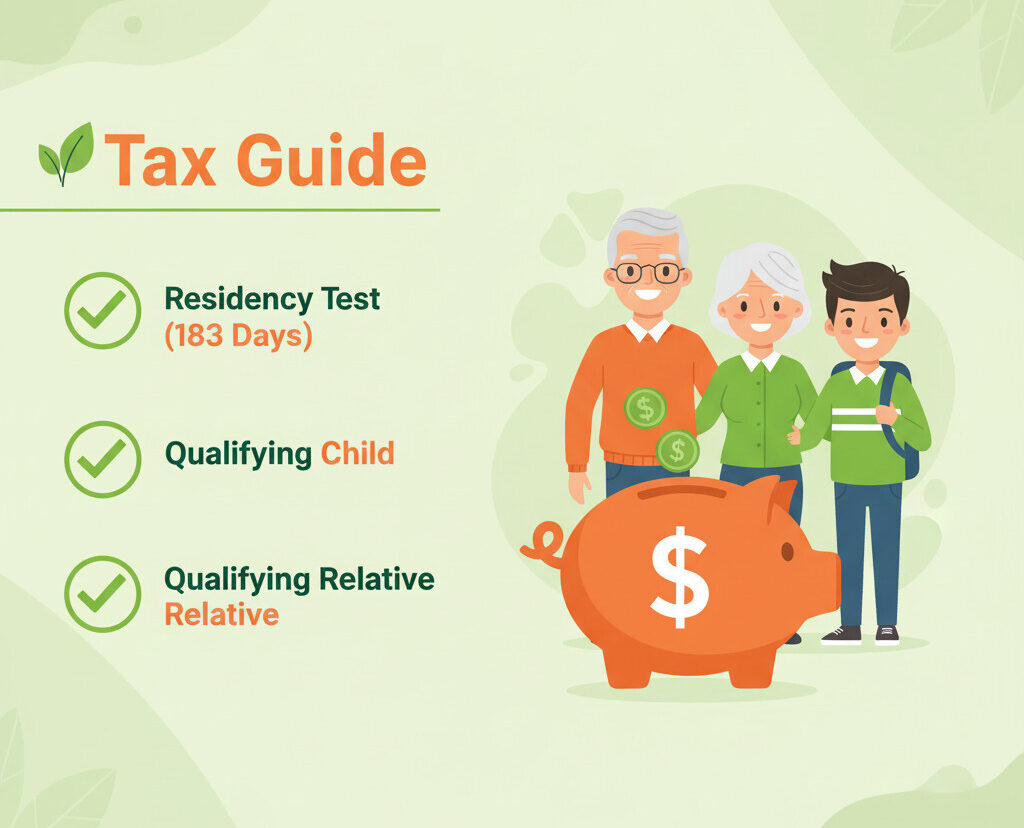

The First & Biggest Hurdle: The U.S. Residency Test 🛂

Okay, before we even dream about those credits, every single person you want to claim must clear the very first and most important hurdle. They must be considered a **U.S. citizen, U.S. national, or U.S. resident alien** for tax purposes.

This is where most people get confused. The IRS has its *own* definition of “resident alien” that has almost nothing to do with immigration status, green cards, or visas. For the IRS, it’s not about legal status; it’s about *physical presence*.

This determination is made by a specific formula called the **Substantial Presence Test**. Your relative must pass this test in the tax year (e.g., 2024) to be claimed as a dependent.

Breaking Down the 183-Day Rule

The Substantial Presence Test has two parts. The person must meet *both*:

- The 31-Day Test: They must be physically present in the U.S. for at least **31 days** during the current tax year.

- The 183-Day Weighted Test: They must be physically present in the U.S. for at least **183 days** during the 3-year period that includes the current year and the 2 years immediately before, using a weighted formula.

📝 The 183-Day Formula

Here’s how the IRS calculates the 183-day total:

(All days in the Current Year)

+ (All days in the First Prior Year × 1/3)

+ (All days in the Second Prior Year × 1/6)

If this total is 183 days or more, they pass this part of the test.

This is critical! Do not count days of presence for “exempt individuals.” This doesn’t mean exempt from tax; it means their days are *exempt from this test*. The most common examples are:

- Students temporarily present on an F, J, M, or Q visa.

- Teachers or trainees temporarily present on a J or Q visa.

For most students, their days in the U.S. literally count as ZERO for this test (usually for their first 5 calendar years). This means even if your student niece lives with you for 365 days, she will likely *fail* the Substantial Presence Test and cannot be claimed.

The Two Paths to Claiming a Dependent 👨👩👧👦

Okay, let’s say your relative *does* pass the residency test (or is a U.S. citizen). Great! You’re past the first hurdle. Now, you have to prove to the IRS that they are, in fact, your dependent.

The IRS gives you two possible paths to do this. You don’t get to choose; you *must* follow this order:

- Path 1: The Qualifying Child Test

- Path 2: The Qualifying Relative Test

You must *always* try the Qualifying Child test first. If a person meets the rules to be your Qualifying Child, you *must* claim them as such. Only if they fail this test for some reason (like being too old or not being the right relationship) can you move on and try to claim them as a Qualifying Relative.

Test 1: The Qualifying Child (It’s Not Just for Your Kids!) 🤔

This test’s name is a bit misleading. A “Qualifying Child” doesn’t have to be *your* child. It can be your brother, sister, niece, nephew, or grandchild, as long as they meet all four of the following tests.

| Test | Description | What it Means |

|---|---|---|

| 1. Relationship | The person must be your… | Son, daughter, stepchild, foster child, brother, sister, half-brother, half-sister, stepbrother, stepsister, or a descendant of any of them (e.g., niece, nephew, grandchild). |

| 2. Age | The person must be… | Under 19 at the end of the year, OR under 24 and a full-time student, OR any age if permanently and totally disabled. |

| 3. Residency | The person must… | Have lived with you for **more than half of the year**. (There are some exceptions for temporary absences like school or medical care). |

| 4. Support | The person must… | **Not** have provided more than half of their own support for the year. (This is different from the relative test! Here, the IRS just checks if *they* paid for themselves, not if *you* paid for them). |

Test 2: The Qualifying Relative (The Broader Category) 📊

So, what about your 65-year-old father or your 30-year-old cousin? They will clearly fail the “Age” test for a Qualifying Child. That’s when you get to move on to this second test: The Qualifying Relative.

This test has four *different* rules. Your relative must meet all of them.

| Test | Description | What it Means |

|---|---|---|

| 1. Not a Qualifying Child | The person must… | **Not** be your Qualifying Child and not be the Qualifying Child of any other taxpayer. (This is the “failed the first test” rule). |

| 2. Relationship or Member of Household | The person must… | Either be related to you in one of the many ways (parent, grandparent, aunt, uncle, in-laws, etc.) OR must have lived with you **all year long** as a member of your household. (Note: Relatives like parents don’t have to live with you!) |

| 3. Gross Income | The person’s… | Gross (total) income for the year must be **less than a specific amount**. For 2023, this was $4,700. (This amount is indexed for inflation, so check the current tax year’s limit!) Tax-exempt income like Social Security generally doesn’t count. |

| 4. Support | You must… | Provide **more than 50%** of the person’s total support for the year. This includes all costs: housing, food, clothes, medical care, etc. You’ll need to do some math here. |

Let’s Solve Our Case Study: The Niece & The Parents 📚

Okay, let’s go back to our original example: You’re supporting your 15-year-old niece and your retired parents, all of whom just moved to the U.S. and live with you. Let’s assume they all pass the Substantial Presence Test (183+ days) and are *not* on student visas.

📝 Case 1: The 15-Year-Old Niece

We *must* try the Qualifying Child test first.

- 1. Relationship: She’s your niece. (PASS)

- 2. Age: She’s 15 (under 19). (PASS)

- 3. Residency: She lived with you all year (more than half). (PASS)

- 4. Support: She’s a teen with no job, so she didn’t provide her own support. (PASS)

Verdict: She is your **Qualifying Child**. You can claim her for the (up to) $2,000 Child Tax Credit and file as Head of Household.

The Plot Twist: What if she *was* on a student visa?

Remember that student visa exception? If she was here on an F-1 visa, her days wouldn’t count. She would *fail* the main Substantial Presence Test. Even though she passed all 4 Qualifying Child tests, she would fail the *first* hurdle (Residency). You could not claim her at all. This one detail changes everything!

📝 Case 2: The Retired Parents

First, we try the Qualifying Child test. They fail the “Age” test immediately. So, we move on to the Qualifying Relative test.

- 1. Not a Qualifying Child: Correct, they failed the age test. (PASS)

- 2. Relationship: They are your parents. This is a valid relationship (and means they don’t even have to live with you, though in our case they do). (PASS)

- 3. Gross Income: They are retired and have $0 income. This is less than the $4,700 limit (for 2023). (PASS)

- 4. Support: You are paying for 100% of their support (more than 50%). (PASS)

Verdict: Both parents are your **Qualifying Relatives**. You can claim the $500 Credit for Other Dependents for *each* of them ($1,000 total) and file as Head of Household.

“But They Don’t Have a Social Security Number!” 👩💼👨💻

This is the final, and most common, question I get. “My parents just got here, they don’t have an SSN. I guess I can’t claim them, right?”

Wrong! Your relatives do **not** need a Social Security Number (SSN) to be claimed as a dependent.

They do, however, need a taxpayer identification number. If they aren’t eligible for an SSN, they must apply for an **ITIN (Individual Taxpayer Identification Number)**. The Child Tax Credit has some specific SSN requirements, but the $500 Credit for Other Dependents (which your parents would get) can be claimed with an ITIN.

An ITIN is a tax processing number issued by the IRS. It’s *only* used for filing federal taxes. It does **not** authorize work in the U.S. or provide eligibility for Social Security benefits. You apply for one using Form W-7, often at the same time you file your tax return claiming them as a dependent.

Conclusion: Key Summary 📝

I know that was a lot of information, but getting this right is so worth the effort. Don’t just assume you can’t claim your relatives. You might be walking away from thousands of dollars in tax savings.

Here’s what you need to remember:

- Hurdle 1: Residency. They must be a U.S. Citizen, National, or Resident Alien. For most, this means passing the **Substantial Presence Test (the 183-day rule)**.

- Hurdle 2: The Tests. You must check the **Qualifying Child** test *first*. If they fail (e.g., too old), you can then check the **Qualifying Relative** test.

- Watch for Exceptions. The student visa exception is a major trap that prevents many from being claimed.

- No SSN is No Problem. Most dependents can be claimed using an **ITIN**.

My best advice? Run the numbers. Check their visa status. Use a worksheet to calculate their days of presence and the support you provided. The rules are complex, but they are clear. You can do this!

Claiming Relatives: Key Summary

Frequently Asked Questions ❓

This can be tricky, but I hope this guide cleared things up! If you have any more questions about a specific situation, feel free to ask in the comments~ 😊