Filed a Tax Extension? Don’t Make This $1,000 Mistake of Paying Penalty

It’s a story I see all the time, especially with self-employed folks. You have a fantastic, profitable year. You’re organized, so you file your tax extension (Form 4868) way before the April deadline. You breathe a sigh of relief, thinking, “Great, I have until October to figure this all out.” You might even take that extra cash you *thought* you had and reinvest it in your business, like buying a new piece of equipment or a vehicle.

Then, a few months later, you have a chat with your accountant. You proudly tell them about your extension and your smart new purchase. The accountant’s face drops. And that’s when the panic sets in. That feeling? That’s “The Tax Extension Trap,” and it’s a perfect (and perfectly awful) example of a common but very costly misunderstanding. If this sounds even remotely familiar, this article is for you. 😊

A Profitable Year’s Dilemma: A True Story 🤔

Let’s walk through a real-world story that I saw happen. We’ll call our business owner “Sarah.” Sarah is a freelance consultant, and 2023 was her best year ever. Her income was way higher than usual, which was fantastic! But it also meant her tax situation was more complicated.

Being responsible, she knew she wouldn’t have all her paperwork ready by April 15th. So, she did what she thought was the right move: she filed an extension, pushing her *filing* deadline all the way to October. With that “extra time,” she decided to make a smart business move and bought a much-needed new work van, using a good chunk of her cash.

Everything seemed great. She was proud of her success and her smart decisions. That is, until she sat down with her accountant in July to start pulling those October numbers together. The accountant asked, “So, how much of your 2023 tax bill did you pay back in April?”

Sarah was confused. “What do you mean? I filed an extension. My payment isn’t due until October, right?”

The look on her accountant’s face told her everything. That’s the moment the panic hit. She had fallen right into the trap.

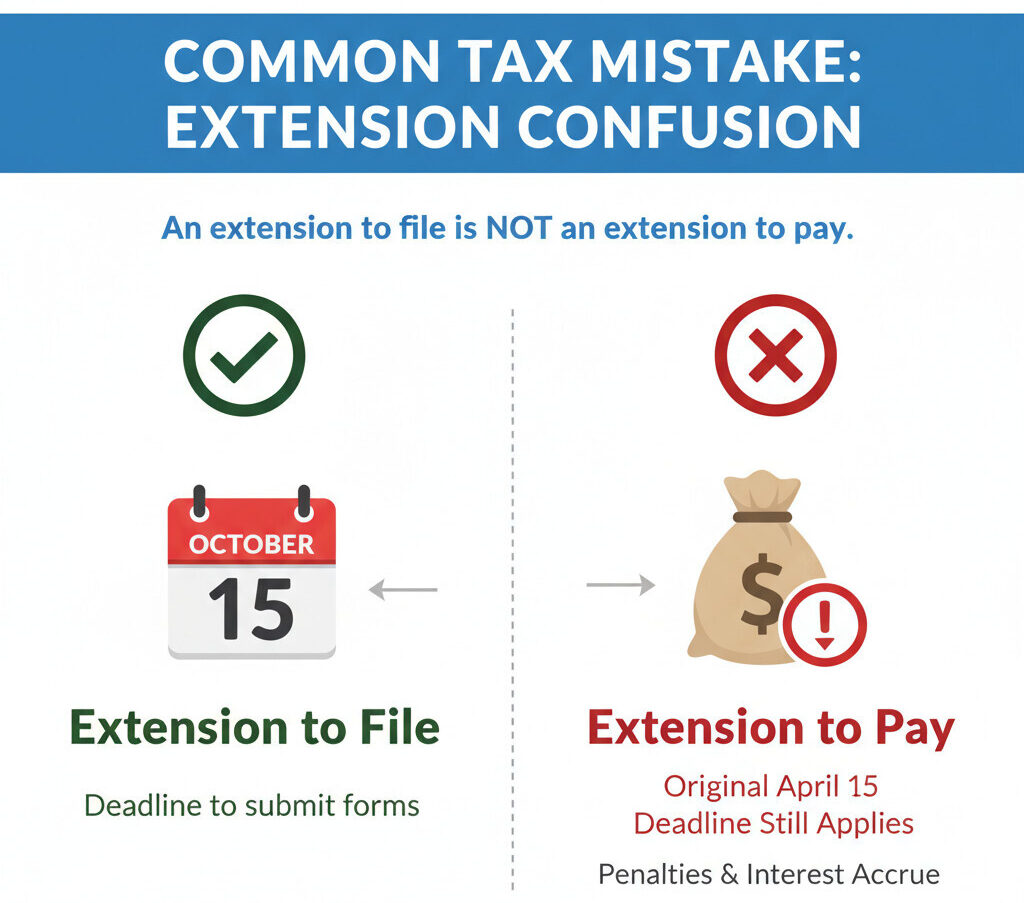

The Core Misconception: File vs. Pay 🚫

This is the absolute most important thing to understand about taxes, and it’s the root of Sarah’s panic. The IRS (and your state tax board) sees your tax obligations in two separate parts:

- An Extension to FILE: This is what you get when you file Form 4868. It gives you more *time* to get your paperwork together and submit your tax return. It moves your *filing* deadline from April to October. This is a real thing, and it’s very useful.

- An Extension to PAY: This… well, this is not a thing. It literally does not exist.

Let me repeat that, because it’s critical: An extension to file is NOT an extension to pay. Your tax payment is *still* due on the original deadline, which is usually April 15th, regardless of when you actually file your forms.

This is the trap. Millions of people, just like Sarah, believe that filing for an extension magically pushes back *all* their tax obligations. It doesn’t. The IRS still expected to receive their money in April, and when they didn’t get it, they started a clock… a penalty and interest clock.

Your Three Core Tax Duties 📊

To make sure you never fall into this trap, it helps to think about your taxes the way the IRS does. You don’t just have one “tax day.” You actually have three separate and distinct duties all year long.

- The Duty to File: This is your duty to submit your tax return (your Form 1040 and all the other schedules) by the deadline. An extension gives you more time to fulfill *this specific duty*.

- The Duty to Pay: This is your duty to pay the taxes you owe for the year. The deadline for this duty is almost always the original deadline (e.g., April 15th). An extension does not change this deadline.

- The Duty to Pre-Pay: This is the one that really trips up business owners. The U.S. has a “pay-as-you-go” system. The IRS doesn’t want to wait a whole year to get their money. They want you to pay your taxes *as you earn income* throughout the year.

If you’re a regular W-2 employee, this is easy. Your employer handles it for you with paycheck withholding. But if you’re self-employed, a freelancer, or have significant income from other sources (like investments), the responsibility is all on you. You are expected to fulfill this “Duty to Pre-Pay” by calculating and sending in quarterly estimated tax payments throughout the year (usually in April, June, September, and January).

Sarah’s “higher-than-usual income” is what made this so dangerous. She likely hadn’t pre-paid enough through her quarterly payments to cover her massive tax bill, and she was (incorrectly) counting on her extension to give her time to pay the large remaining balance.

The High Cost of Delay: Understanding the Penalties 🧮

So, what happens if you mess this up? Why did Sarah panic? Because the IRS doesn’t just send a friendly reminder. They send a bill, complete with penalties and interest.

When you get this wrong, you can be hit with two major penalties. And one is *way* worse than the other.

Penalty Comparison: Filing vs. Paying

| Penalty Type | Rate (per month or part of a month) | Maximum Penalty |

|---|---|---|

| Late Payment Penalty | 0.5% of your unpaid tax | 25% of your unpaid tax |

| Late Filing Penalty | 5.0% of your unpaid tax | 25% of your unpaid tax |

Look at those numbers. The Late Filing Penalty is 10 times worse than the Late Payment Penalty. This brings us to a crucial point that we’ll see in Sarah’s story: filing that extension was *still* a super smart move!

It gets worse. On top of those penalties, the IRS also charges interest on the unpaid amount (both the tax and the penalties) from day one. And if you failed in your “Duty to Pre-Pay,” they can *also* hit you with a separate Underpayment Penalty. It’s a brutal combination that can make a tax bill grow frighteningly fast.

The Path to Resolution: Back to Our Story 👩💼

Okay, so let’s circle back to Sarah, who is now panicking in her accountant’s office. Now that we know the rules, we can see exactly what’s happening.

By filing her extension, Sarah completely avoided the brutal 5.0% per month Late Filing Penalty. This was a huge win, even if she didn’t realize it. She fulfilled her “Duty to File” (or at least, the extension part of it). That extension was her shield against the most aggressive penalty.

The Bad News: The Smaller Monster is Growing.

Because she didn’t fulfill her “Duty to Pay,” the 0.5% per month Late Payment Penalty clock started ticking way back on April 16th. So, by the time she met her accountant in July, she already owed the original tax bill PLUS…

- A Late Payment Penalty for April-May

- A Late Payment Penalty for May-June

- A Late Payment Penalty for June-July

- …and interest on all of it.

This is why she was in a panic. The money she used for the van should have gone to the IRS. Now she owed *more* than she did in April, and she didn’t have the cash on hand to pay it.

The Solution: Stop the Bleeding.

For Sarah, and for anyone else in this boat, the solution is painful but simple: Pay as much as you possibly can, as soon as you possibly can. Every single day you wait, that penalty and interest bill just keeps growing. The only way to stop the clock is to pay the underlying tax bill.

The Tax Extension Trap: Key Takeaways

Conclusion: Are You Protecting Your Finances? 📝

At the end of the day, understanding the difference between your “Duty to File” and your “Duty to Pay” isn’t just some boring tax rule. It’s about protecting your wallet. That panic Sarah felt is awful, and it’s completely avoidable.

Knowing your three core duties (File, Pay, and Pre-Pay) is genuinely your best defense against these nasty, unexpected costs. So, take a look at your own tax plan. Is your understanding protecting your finances?

I hope this story helps you avoid the trap! If you’ve ever been confused by this, or have your own story to share, I’d love to hear about it in the comments. We can all learn from each other! 😊