California Tax Residency: How to Legally Shield Income When a Spouse Moves to a No-Tax State

Alright, let’s talk about something that happens all the time in our mobile world. Picture this: you and your spouse live in California. One of you lands an *amazing* job offer—a huge promotion, great pay, exciting new role… but it’s in another state. Let’s say, Washington or Texas, a state with zero income tax. What do you do? Maybe your job, family, or roots are firmly planted in California, so you decide to live apart, at least for a while. It’s a “two-state household.”

This is a super exciting time, but it opens up a massive, and I mean *massive*, financial question that most people don’t think about until it’s too late: **How do you stop California from taxing your spouse’s new income?** If you’re not careful, you could end up paying California’s high income tax on money that was *never even earned in California*. Sounds crazy, right? Well, it’s a real risk. But the good news is, there’s a specific, legal strategy to prevent it. Let’s dive in. 😊

The Two-State Tax Dilemma 🤔

Let’s use a clear example. We’ll call our couple Maria and David.

- Maria has a stable job she loves in Los Angeles, California.

- David gets a fantastic 2-year contract position with a tech company in Seattle, Washington.

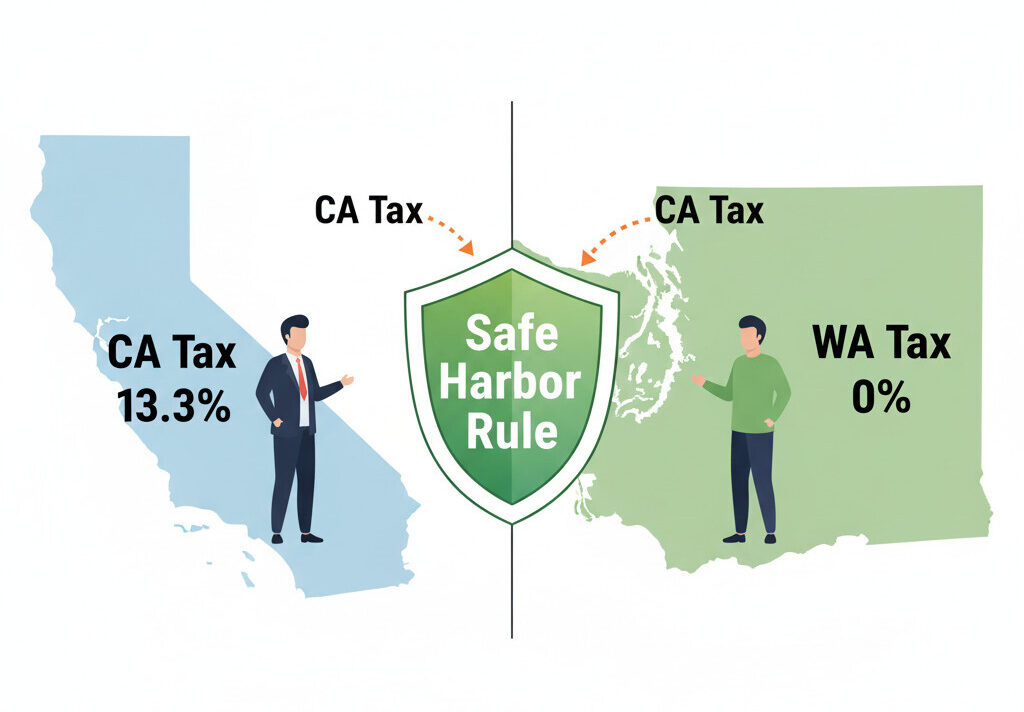

The financial contrast is stark. California has one of the highest state income tax rates in the country, topping out at 13.3%. Washington, on the other hand, has zero state income tax. None. Zilch.

David moves to Seattle, gets a new apartment, and starts his job. Maria stays in their home in Los Angeles. When tax season rolls around, they face the terrifying question: Does Maria’s presence in California mean they have to add David’s entire Seattle salary to their California tax return? If so, they’ll instantly owe 10-13% of it to the state of California, even though he earned it 100% in Washington. This one problem could wipe out the financial benefit of David’s new job.

California’s “Taxing Reach”: The Power of Residency 🌍

To understand the solution, you first have to understand the problem. And the problem boils down to one powerful word: **”Residency.”**

California’s tax authority, the Franchise Tax Board (FTB), has two sets of rules for taxing people. It all depends on your residency status.

- If you are a CA Resident: You are taxed on your *entire* worldwide income. It doesn’t matter if you earned it in California, Washington, or on the moon. If you’re a CA resident, you pay CA tax on it.

- If you are a CA Non-Resident: You are only taxed on your “California-source” income. This is money you *actually* earned while physically working in California.

So, the entire strategy is simple: We must *legally and provably* change David’s status from a **CA Resident** to a **CA Non-Resident**. If Maria (the CA resident) and David (now a non-resident) file jointly, his non-CA income is *still* pulled in. But if David can *prove* he is a non-resident, his Washington salary is *not* California-source income, and the FTB can’t touch it.

Why California is So Skeptical (And What They Look For) 🕵️

Here’s the catch. California doesn’t just take your word for it. The FTB is famously skeptical, especially when one spouse remains in California. They will, by default, presume David is *still* a California resident who is just “temporarily absent.”

The FTB’s main question is: “Is this a temporary move for a tax advantage, or a permanent change?” With a spouse still in CA, they will almost always assume it’s temporary.

If you just *say* you’ve moved, you’ll likely face a dreaded residency audit. In this audit, the FTB will use a “facts and circumstances” test (also known as the “closest connections” test) to determine your *true* home or “domicile.” They look at where you have the most significant connections.

To win this audit, David would have to prove he moved his *entire life* to Washington, not just his job. The FTB would look at:

- Where is his driver’s license? (He’d need a WA license)

- Where is he registered to vote? (He’d need to register in WA)

- Where are his primary bank accounts? (He’d need to open WA accounts)

- Where does he see his doctor and dentist? (He’d need to find WA providers)

- Where is his “abode”? (He’d need a real lease/home in WA, not just a hotel)

- Where are his “near and dear” items? (Did he move his furniture, his dog, etc.?)

This is a *messy, subjective, and dangerous* fight to have. And with his wife (his closest connection!) still in California, it’s a fight David would likely *lose*. But don’t worry… there is a way to skip this fight entirely.

The “Safe Harbor” Rule: Your Golden Ticket 🎟️

Tucked away in California’s tax code is a beautiful, objective, black-and-white exception. It’s called the **”Safe Harbor” rule** for residents leaving the state. Think of it as a clear test that, if you pass, *proves* you are a non-resident. No messy “closest connections” audit needed.

California law states that you are automatically considered a non-resident if you leave the state for an “employment-related contract” that is for a specific, temporary period.

This rule was designed for people just like David. But there’s one critical condition. The contract must be for a long-enough period. What’s the magic number?

The employment contract must be for a period of *at least* 18 months (specifically, 546 days).

If your out-of-state job contract is for 18 months or more, you can qualify for this Safe Harbor. This is your “get out of jail free” card from the FTB. It’s the key to the entire strategy.

Case Study: Applying the Safe Harbor Rule 📚

Let’s apply this clean rule to our couple, Maria and David.

Situation of the Case Study’s Subject

- Subject: David

- Action: Moving from California to Washington.

- Reason: A new job.

- Contract Term: 2 years (which is 24 months).

Safe Harbor Analysis

1) Is the move for an employment-related contract? Yes.

2) Is the job outside of California? Yes.

3) Is the contract term at least 18 months? Yes! David’s 24-month contract is longer than the 18-month requirement.

Final Result

Success! David officially qualifies as a California non-resident under the Safe Harbor rule for the entire 24-month period. He doesn’t have to worry about the “closest connections” test. He has the contract, he has the proof.

This is a massive victory. But hold on, we’re not done. Qualifying is Step 1. You can still mess this up if you don’t *file your taxes* correctly. This brings us to the final, critical piece of the puzzle.

The Winning Filing Plan: Don’t Fall at the Finish Line! 🏁

Now that David is a legal non-resident, how does the couple *actually* file their taxes? This is where you have to throw out what you normally know about taxes. For 99% of married couples, “Married Filing Jointly” (MFJ) is the best way to go. But not here. In this specific case, it’s a trap.

If Maria (resident) and David (non-resident) file a *joint* California return, they are combining their incomes. California law states that if you file jointly, the total income of *both* spouses is used to determine the tax rate. Maria’s residency “pulls in” David’s non-resident income, and the FTB will tax it. All that hard work is for nothing.

The winning move? **Married Filing Separately (MFS).**

This is the only way to build a firewall between the two incomes. By filing MFS, you are telling the state of California that you are two separate financial entities for tax purposes.

Here’s how the winning plan works:

- Maria (The CA Resident): Files her California tax return as “Married Filing Separately.” She reports *her* Los Angeles income and pays her California taxes as usual.

- David (The WA Non-Resident): *Also* files a California tax return as “Married Filing Separately.” But on his return, he reports **$0** of California-source income (because he worked in WA). He attaches a statement explaining he is a non-resident under the Safe Harbor rule, referencing his 24-month contract.

The result? David’s entire Washington salary is 100% legally protected from California state tax. This is a *huge* win, potentially saving them tens of thousands of dollars.

Filing Plan Comparison

| Filing Status | David’s WA Income | California Tax Result |

|---|---|---|

| Married Filing Jointly | Combined with Maria’s | Taxed by California ❌ |

| Married Filing Separately | Reported Separately | NOT Taxed by California ✅ |

Key Strategy: Splitting States & Taxes

Conclusion: Key Summary 📝

Living in two different states as a married couple creates a complex tax situation, but not an unsolvable one. The absolute worst thing you can do is nothing—just filing jointly and letting California tax 100% of your out-of-state income. Here’s the winning playbook one more time:

- Residency is Everything: Understand that California taxes residents on worldwide income but non-residents only on CA-source income. The goal is to make the moving spouse a non-resident.

- Avoid the “Closest Connections” Test: Don’t let the FTB audit you on subjective factors. It’s a losing battle when your spouse is still in CA.

- Use the “Safe Harbor” Rule: This is your objective proof. Secure an employment-related contract for 18 months (546 days) or more. This is your non-negotiable golden ticket.

- File “Married Filing Separately”: This is the final, essential step. It’s the only way to build the legal tax firewall between your resident income and your non-resident income.

This strategy requires careful planning and perfect execution, but it’s 100% legal and can save you a fortune. State lines are also tax lines—it pays to know where they’re drawn!

Frequently Asked Questions ❓

Got more questions on this? Let me know in the comments! But for advice on your specific personal situation, please consult a qualified tax professional. It’s worth every penny! 😊