Top 5 IRS Audit Red Flags Every Small Business Must Know

You know, if you’re a small business owner, there’s one three-letter agency you really, really don’t want getting in touch with you: the IRS. Just the thought can cause that little nagging feeling in the back of your head, wondering if a notice is on its way. Well, believe me, you are not alone. And right now, that concern is a bigger deal than it’s been in a long, long time. But here’s the good news: you can turn that anxiety into a solid plan. Let’s get into it! 😊

The $80 Billion Elephant in the Room: Why IRS Audits Are on the Rise 🐘

So, what’s all the fuss about? It comes down to one number: $80 billion. That’s the recent budget increase the IRS received, and you better believe a huge chunk of that cash is going straight to hiring more auditors and seriously ramping up enforcement. More resources for them means way more scrutiny for us.

But let’s demystify this whole “audit” thing. At its core, a tax audit is simply a verification process. The IRS is checking to make sure the numbers you reported—your income, your deductions—are accurate. It’s not an automatic accusation. However, certain things you do (or don’t do) can definitely move you to the top of their list for that verification.

The Big “Don’ts”: Top Red Flags That Attract IRS Scrutiny 🚩

Okay, so let’s talk about those triggers. What are the red flags that might as well be a big, flashy invitation for the IRS to come take a closer look at your books? Once you know what they are, you can make darn sure you steer clear of them.

Red Flag #1: Income Reporting Errors (The Easiest Catch)

This is the big one. The absolute number one mistake that gets people flagged is messing up their income reporting. This could be not reporting some cash you took in, having your numbers not match a 1099 form someone sent you, or even a simple mistake like reporting your net income instead of your gross revenue. These are the easiest things for the IRS computers to spot.

How do they catch this so easily? It’s all automated. When a client pays you over a certain amount (like $600), they are often required to send a Form 1099 to you and a copy directly to the IRS. The IRS computer system then does a simple match. It looks at the expense your client claimed they paid you and compares it to the income you reported. If those numbers don’t match? Boom. That’s an instant, automatic red flag.

Red Flag #2: Playing Fast and Loose with Expenses

Of course, it’s not just about income. Other things can get you noticed, too:

- Unusually High Expenses: Claiming expenses that are way, way higher than other businesses in your specific industry.

- The “Miscellaneous” Black Hole: Being lazy and lumping a ton of different costs under a vague “miscellaneous” category.

- 1099 Over-Reliance: Relying almost entirely on 1099 contractors can look suspicious to the IRS, as if you’re trying to dodge payroll taxes.

- Just Being Late: Honestly, simply filing your taxes late is a really easy way to get on their radar.

Red Flag #3: Suspicious Cash Transactions

Listen, this automatic tracking isn’t just about tax forms. You’ve got to be super mindful of large cash transactions. Anytime you deposit or withdraw more than $10,000 in cash in a single day, your bank is required by law to report that to the government. They *have* to. A pattern of these transactions (or a pattern of transactions *just under* $10,000) will absolutely draw some unwanted attention.

Building Your “Audit Shield”: Proactive Ways to Reduce Risk 🛡️

Knowing all the red flags is defense, right? It’s about knowing what *not* to do. But you know what they say: the best defense is a good offense. So, let’s switch gears and talk about the proactive steps you can take to make your business a much, much tougher target in the first place.

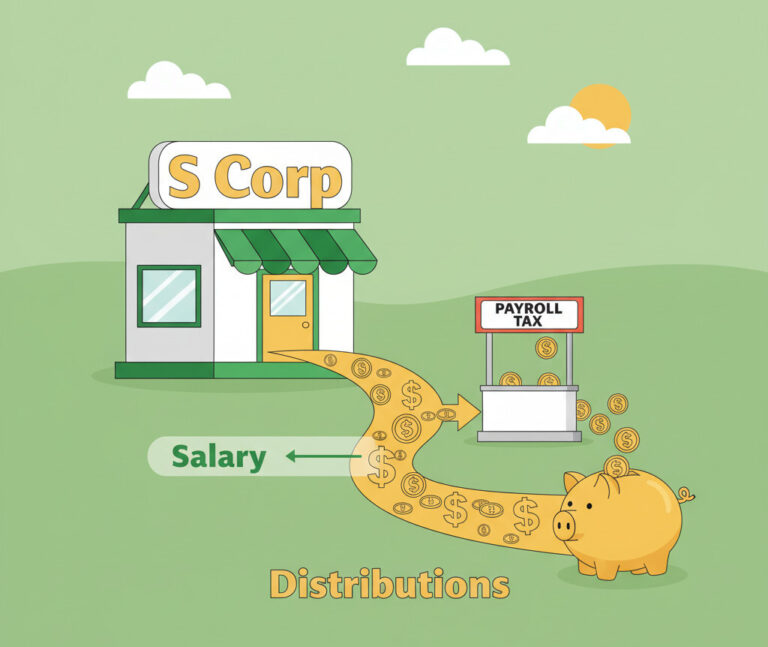

Your Business Structure: The 15x Difference

This right here is a big one. It’s probably one of the most important strategic choices you can make. Statistically, for years, sole proprietors who file what’s called a Schedule C are audited at a much higher rate than corporations (like S-Corps or C-Corps).

How much of a difference? While the IRS doesn’t publish exact numbers, some studies suggest that properly setting up your business as a corporation can lower your audit risk by as much as 15 times compared to being a sole proprietor. Think about that. 15x! That’s a massive drop in risk.

Why? It’s because that Schedule C form directly mixes your business and personal finances all in one place, which just creates way more room for error and, well, scrutiny.

If you *do* operate as a sole proprietor and use a Schedule C, you have to be extra careful about reporting losses year after year. If you do, the IRS is going to look at that and start to wonder, “Hey, is this a real business, or is it just a hobby that they’re using to write off losses against their other income?” You don’t want them asking that question.

The “No Round Numbers” Rule (This is a great tip!)

Here is a super simple but incredibly powerful tip. Trust me on this. When you claim an expense for exactly $500.00, it just looks like an estimate. It feels like a guess, not a documented fact. It kind of suggests you might not have the receipts to back it up.

On the other hand, a specific number, like $534.21, screams accuracy. It tells a story. It says, “I have a receipt for this, down to the penny.” And that is exactly the impression you want to give.

Consistency is King 👑

Finally, you have to make absolutely sure that all of your different tax filings are telling the exact same, consistent story. Remember those computers? They will cross-reference everything.

The payroll expenses you claim on your income tax return need to perfectly match what’s on your payroll tax forms. The total you claim you paid to contractors has to perfectly match the sum of all the 1099s you sent out. Everything has to line up. Consistency is key.

The Ultimate Defense: Your Best Shield is Simpler Than You Think 📓

After we’ve gone through all these red flags and strategies, it really all boils down to one simple, core idea. When you strip everything else away, this is what’s left. This is the foundation of it all.

Here it is: Meticulous, accurate, well-documented bookkeeping isn’t just good business practice. It is your single best defense. It’s your shield. It’s your armor. Because with great records, even if you *do* get selected for an audit, it just becomes a simple, boring process of showing them your work. No panic. No stress.

IRS Audit-Proofing 101

Conclusion: Is Your Business Ready? 📝

So, I’ll leave you with this question: If the IRS came asking tomorrow, are your records truly ready to be your shield? Is your business prepared?

The thought of an audit is scary, but you don’t have to operate from a place of fear. By understanding the red flags and, more importantly, building a strong, proactive defense, you can turn that anxiety into confidence. Thanks for joining us!

If you have any questions or your own tips for staying prepared, feel free to ask in the comments~ 😊