OBBBA Tax Update: Which States Are Decoupling in FY26?

Let’s be honest, keeping up with tax laws feels a bit like trying to drink from a firehose lately, doesn’t it? 😅 Just when we thought we had a handle on things, the federal government passed the “One Big Beautiful Bill Act” (OBBBA), also formally known as P.L. [cite_start]119-21[cite: 53]. While the name might sound optimistic, the reaction from various states has been… well, mixed, to say the least.

I’ve been digging through the latest January 2026 updates, and the landscape is looking pretty fragmented. Some states are saying “no thanks” to the new federal rules, while others (shoutout to Texas! 🤠) are jumping right in. If you’re managing a business with a footprint across multiple states, you need to pay close attention to these divergences.

In this post, I’m going to walk you through exactly which states are decoupling from the OBBBA, what’s happening with bonus depreciation, and a few surprise “gotchas” like New York City’s cookie nexus. Let’s dive in!

Federal Highlights: The “Safe Harbor” & Excise Taxes 🏛️

Before we get into the messy state stuff, let’s quickly touch on what’s happening at the federal level.

First off, if you’re in the carbon capture game, there’s some good news. [cite_start]The IRS released Notice 2026-01, which provides a “safe harbor” for claiming the section 45Q carbon capture credit for 2025[cite: 13]. [cite_start]This is essentially a backup plan in case the EPA’s electronic reporting tool isn’t ready by June 2026[cite: 15]. It gives taxpayers a way to determine eligibility without being stuck in limbo.

Final regulations for the corporate stock buyback excise tax are here. [cite_start]The 1% excise tax applies to repurchases of stock by certain publicly traded corporations after December 31, 2022[cite: 24]. [cite_start]The final regulations generally adopt the 2024 proposals but include some significant modifications[cite: 26].

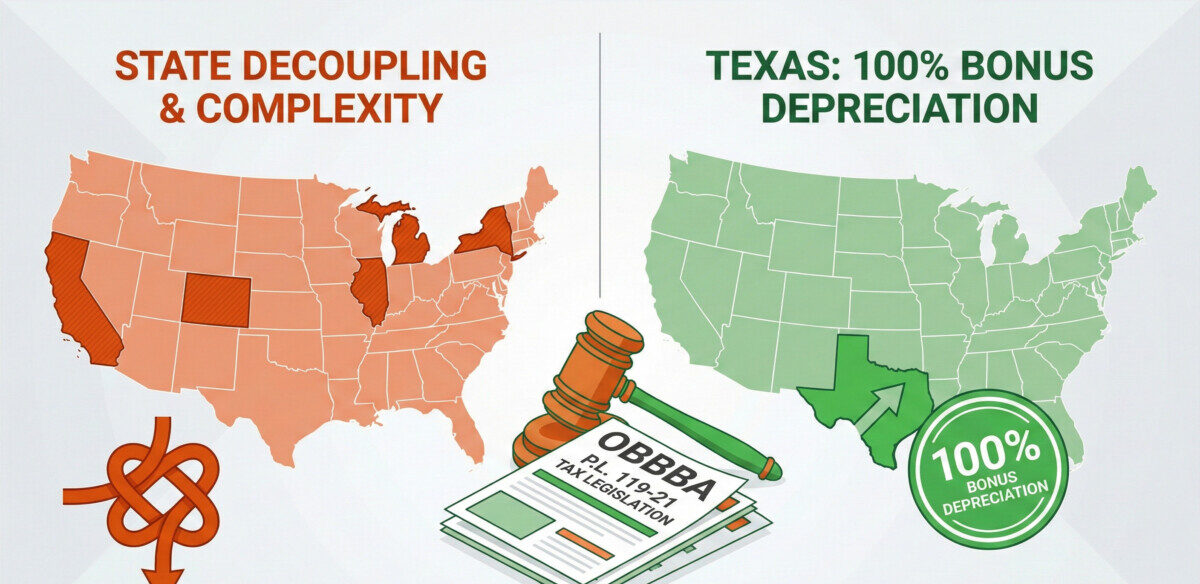

The “OBBBA” Divide: States Saying “No” 🙅♂️

Here is the biggest headache for FY26: Decoupling. The OBBBA introduced changes to R&E expensing (Section 174A), bonus depreciation (Section 168(k)), and interest limitations (Section 163(j)). However, many states are refusing to conform to these changes to protect their tax revenue.

[cite_start]For instance, Michigan has explicitly decoupled from five key federal changes, including the immediate deduction of R&E expenses and the increased business interest deduction[cite: 192, 193, 196]. [cite_start]By reverting to pre-OBBBA rules, they estimate avoiding a revenue loss of about $540 million for FY 2025-26[cite: 190].

California is also holding the line. [cite_start]While they updated their conformity date to January 1, 2025, the new law specifically excludes federal tax law enacted after that date, meaning OBBBA provisions do not apply[cite: 66, 67].

State Decoupling Snapshot

| State | Stance on OBBBA | Key Decoupling Areas |

|---|---|---|

| California | [cite_start]Does NOT conform [cite: 67] | Entire OBBBA act (Bonus dep, R&E, etc.) |

| Delaware | [cite_start]Decoupled [cite: 91] | [cite_start]R&E expenses (174A), Bonus Dep (168k), Special Dep (168n) [cite: 93, 94] |

| Pennsylvania | [cite_start]Decoupled [cite: 299] | [cite_start]R&E expenses, Interest limitation (163j), Special Dep [cite: 300, 301] |

| Rhode Island | [cite_start]Decoupled [cite: 322] | [cite_start]Business interest, R&E expensing, Depreciable asset caps [cite: 325, 326] |

| Michigan | [cite_start]Decoupled [cite: 190] | [cite_start]IRC 174A, 168(n), 168(k), 163(j), 179 [cite: 190] |

If you are filing in Florida, they haven’t addressed OBBBA yet. [cite_start]The legislature will likely consider these amendments in the session beginning January 2026[cite: 127]. For now, keep your eyes peeled for updates.

The Outliers: Texas & New York City 🤠🏙️

While many states are saying “no,” Texas is saying “yee-haw” (sorry, I had to!). [cite_start]The Texas Comptroller has announced that they will align franchise tax depreciation rules with the bonus depreciation provisions of the OBBBA[cite: 386].

This is a big deal. [cite_start]Effective with the 2026 report, businesses can deduct the full cost of qualifying fixed assets acquired after Jan 19, 2025[cite: 388]. [cite_start]This move is intended to eliminate the burden of maintaining two different sets of books for federal and state taxes[cite: 389].

New York City: The “Cookie” Rule 🍪

Meanwhile, in New York City, things are getting stricter for digital businesses. [cite_start]The Department of Finance released proposed regulations stating that placing internet “cookies” on a customer’s device to gather information for product development or inventory adjustment is NOT a protected activity[cite: 284].

[cite_start]This means simply having those cookies on a user’s computer in NYC could create nexus, making you liable for the Business Corporation Tax (BCT)[cite: 284].

🔢 Texas Bonus Depreciation Estimator

Estimate potential deductions under the new Texas alignment with OBBBA (100% bonus depreciation).

International & Other Considerations 🌍

It’s not just the US making moves.

-

[cite_start]

- OECD Pillar Two: A “side-by-side package” was released on Jan 5, 2026, regarding global minimum tax rules[cite: 425]. [cite_start]It includes guidance on safe harbors and substance-based tax incentives[cite: 426]. [cite_start]

- Brazil: A new 10% withholding tax on dividends has been introduced, effective January 1, 2026[cite: 459]. [cite_start]

- Illinois: The state is shifting from the “Joyce” to the “Finnigan” method for apportionment[cite: 133]. This changes how sales are thrown back or thrown out, so check your numerators!

Key Takeaways: Staying Compliant 📝

We covered a lot of ground, but here are the absolute essentials you need to remember for this tax season.

- Decoupling is the Norm: Do not assume your state follows the OBBBA. CA, MI, PA, DE, RI, and DC have all decoupled from major provisions like R&E expensing and bonus depreciation.

- Texas is an Opportunity: If you have assets in Texas, you can likely utilize the full 100% bonus depreciation thanks to their alignment policy.

- Digital Nexus Risks: Be very careful with internet cookies in New York City; they can trigger tax liability.

FY26 Tax Update Cheat Sheet

Frequently Asked Questions ❓

Managing tax compliance across multiple states is never boring, especially this year! If you’re feeling overwhelmed by the decoupling rules, you aren’t alone. If you have any questions about how these changes affect your specific business, feel free to ask in the comments or reach out! 😊