How to Deduct Auto Loans & Tips Without Itemizing: Schedule 1-A Breakdown

Let’s be real for a second: tax season is usually that time of year when we all collectively groan, gather up a chaotic pile of receipts, and hope for the best. I’ve been there, staring at a screen full of complicated IRS jargon, wondering if I’m somehow leaving money on the table. It’s stressful, right? But what if I told you that for the 2025 tax year, the IRS actually introduced something that could put a significant chunk of change back into your pocket? 😊

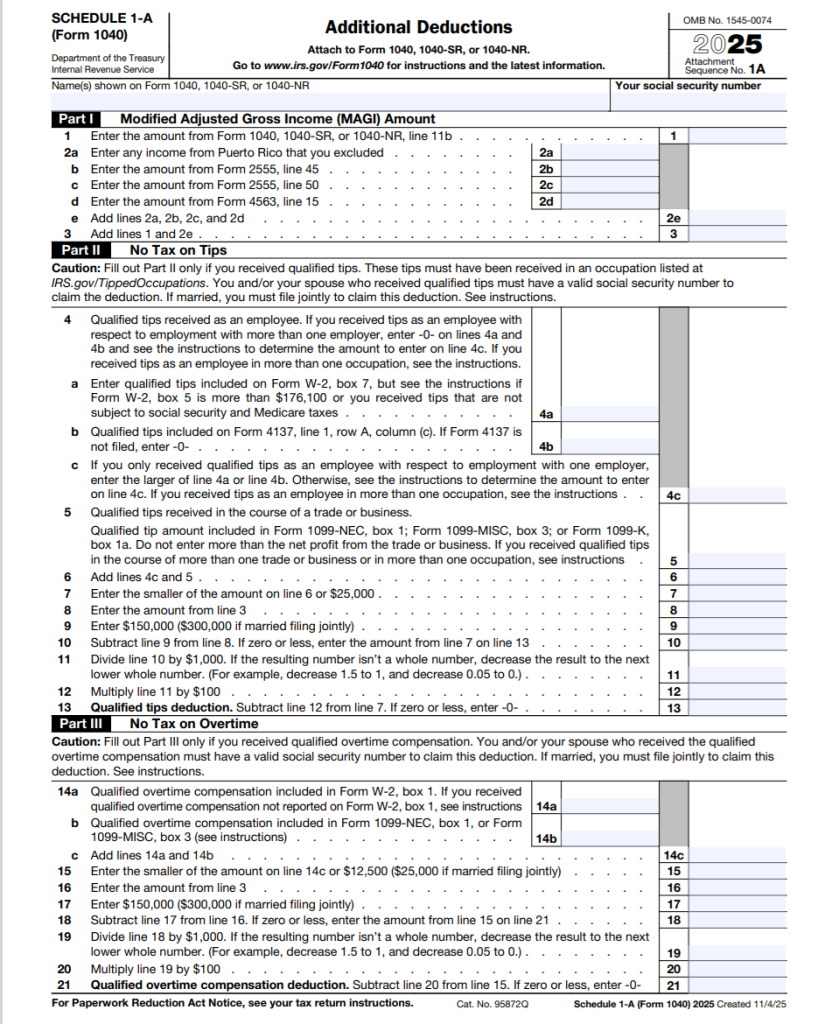

Last July, the government passed the One Big Beautiful Bill Act (OBBBA), and with it came a brand-new tax form that you absolutely need to know about: Schedule 1-A. The IRS officially published this form and its instructions this past Monday, taking it out of the draft phase we saw in September 2025 and making it a reality for your upcoming tax return.

Whether you’re hustling for tips, grinding out overtime hours, paying off a car loan, or enjoying your golden years, this new form is designed to give you a break. And the absolute best part? You don’t even need to itemize your deductions to claim these! You can take the standard deduction and still get these incredible tax breaks. Let’s dive deep into exactly how Schedule 1-A works and how you can maximize your refund this year.

What Exactly is Schedule 1-A? 🤔

Before we get into the nitty-gritty of the specific deductions, let’s talk about what Schedule 1-A actually is. Think of it as an add-on to your standard Form 1040. Historically, if you wanted to deduct specific expenses, you often had to itemize your deductions (using Schedule A), which meant giving up the standard deduction. For millions of Americans, itemizing just didn’t make mathematical sense.

The One Big Beautiful Bill Act changed the game. Schedule 1-A acts as an “above-the-line” deduction mechanism for four very specific categories. This means the deductions you claim here will directly lower your Adjusted Gross Income (AGI), which in turn lowers the amount of income you are taxed on. It’s a win-win.

To claim any of the new OBBBA deductions on Schedule 1-A, if you are married, you must file a joint tax return. These benefits are heavily restricted for married couples filing separately, so make sure you consult with a tax professional about your filing status!

The Tipped Worker’s Dream: Up to $25,000 Deduction 💸

If you work in the service industry—whether you’re a bartender, a server, a hair stylist, or a bellhop—you know that tips are the lifeblood of your income. The IRS knows this too, and Part II of the new Schedule 1-A instructions outlines a massive new benefit: a deduction of up to $25,000 on qualified tips.

To claim this deduction, there is one non-negotiable rule: your tips must be officially reported as income. You can’t deduct under-the-table cash that the IRS doesn’t know about. The instructions provide specific worksheets to help you calculate your tipped income accurately, ensuring you don’t miss a dime of what you’re owed.

However, there are income limits (phaseouts) you need to be aware of. The deduction begins to phase out if your Modified Adjusted Gross Income (MAGI) is greater than $150,000 for single filers, or $300,000 for married couples filing jointly. If you make below those thresholds, you can potentially deduct every single dollar of your tipped income up to the $25k cap!

The IRS has provided lists and categories of occupations where workers “customarily and regularly receive tips.” If your job falls into a gray area, be sure to review the official definitions of “qualified tips” in the Schedule 1-A instructions to ensure you are eligible.

Clocking Extra Hours? The Overtime Deduction Explained ⏰

We’ve all had those weeks where we put in 50, maybe 60 hours, sacrificing our personal time to get the job done. While the extra money is nice, getting taxed heavily on those hard-earned overtime hours always feels like a punch to the gut. Part III of Schedule 1-A is here to soften that blow.

Under the new rules, you can claim a deduction of up to $12,500 for overtime compensation (or a combined $25,000 if you are married filing jointly and both spouses work overtime). But here is where it gets a little bit technical, so stick with me.

The IRS defines “qualified overtime compensation” very strictly. It applies specifically to overtime paid as required under Section 7 of the Fair Labor Standards Act of 1938 (FLSA). This generally means the IRS is letting you deduct the “half” portion of your “time-and-a-half” pay.

For example, if your regular rate is $20 an hour, your overtime rate is $30 an hour. The $10 premium (the “half” portion) is what qualifies for this deduction. Your employer might list this on your pay stub as “overtime premium” or “FLSA Overtime Premium.” Just like the tips deduction, this benefit phases out if your MAGI exceeds $150,000 ($300,000 for joint filers).

Driving a Hard Bargain: Auto Loan Interest Deduction 🚗

Did you buy a new car recently? If so, Part IV of Schedule 1-A might be your new best friend. You can now deduct the interest paid on a qualified passenger vehicle loan. In an era of high interest rates, this is a massive relief for everyday commuters.

But, of course, the government has attached some strings to encourage domestic manufacturing. To qualify, the vehicle must meet the definition of an “applicable passenger vehicle,” which explicitly requires that its final assembly occurred in the United States. Furthermore, the vehicle must be strictly for “personal use.” If you bought a fleet of vans for your plumbing business, you’ll need to handle that on your Schedule C business deductions, not here.

Not sure where your car was assembled? You can easily check by looking at your vehicle’s VIN (Vehicle Identification Number) or by using the NHTSA’s online VIN decoder tool. If the first character is a 1, 4, or 5, it was assembled in the U.S.!

Golden Years Bonus: Enhanced Senior Deduction 👵👴

Last but certainly not least, Part V of Schedule 1-A introduces an enhanced deduction for senior citizens. Inflation hits those on fixed incomes the hardest, and this provision of the OBBBA is designed to provide some breathing room.

To qualify for this specific tax break, you (or your spouse, if filing jointly) must have been born before January 2, 1961. You must also have a valid Social Security Number (SSN). If you meet these criteria, you can claim a maximum enhanced deduction of $6,000 per person.

If you are married filing jointly, both spouses have valid SSNs, and both were born before that magic date in 1961, your household can claim a combined deduction of $12,000! Take note, however, that the phaseout limits are stricter for this category. The $6,000-per-person amount begins to reduce if your MAGI exceeds $75,000 for single filers, or $150,000 for married couples filing jointly.

At a Glance: 2025 OBBBA Deductions Summary 📊

That was a lot of numbers and rules to digest! To make things easier, I’ve put together this quick reference table so you can compare the four major deductions found on Schedule 1-A side-by-side.

| Deduction Type | Max Amount (Single / Joint) | MAGI Phaseout Starts At | Key Requirement |

|---|---|---|---|

| Tips | $25,000 / $25,000* | $150k Single / $300k Joint | Tips must be formally reported. |

| Overtime | $12,500 / $25,000 | $150k Single / $300k Joint | Applies to FLSA “half” premium. |

| Auto Loan Interest | No hard cap stated | N/A (check instructions) | Final assembly must be in the U.S. |

| Seniors | $6,000 / $12,000 | $75k Single / $150k Joint | Born before Jan. 2, 1961. |

*Note: The tips deduction max is $25k total, regardless of single or joint status, according to current guidelines.

Let’s Do the Math: A Real-Life Case Study 🧮

It’s always easier to understand taxes when you look at a real-world example. Let’s imagine a married couple, Sarah and Mark, filing jointly for the 2025 tax year.

Situation: Sarah & Mark’s Household

- Income: Their combined MAGI is $120,000 (well below the $300k phaseout limits!).

- Sarah’s Job: She works as a high-end restaurant server and properly reported $18,000 in tips for the year.

- Mark’s Job: He works in manufacturing and pulled a lot of overtime. The “FLSA overtime premium” (the half portion) on his pay stubs totaled $4,500 for the year.

- New Car: They bought a new U.S.-assembled SUV for personal use and paid $1,200 in auto loan interest in 2025.

- Age: Both are in their 40s (so they do not qualify for the senior deduction).

Calculation Process

1) Tips Deduction: Sarah’s $18,000 in tips is fully deductible since it’s under the $25k max and they are under the MAGI limit.

2) Overtime Deduction: Mark’s $4,500 FLSA premium is fully deductible since it’s under the $25k joint max.

3) Auto Interest Deduction: The $1,200 in interest is fully deductible because the car is U.S.-made and for personal use.

Final Result

Total Above-The-Line Deductions: $18,000 + $4,500 + $1,200 = $23,700

By simply filling out Schedule 1-A, Sarah and Mark reduce their taxable income by almost $24,000! Even if they take the standard deduction, they still get this massive reduction, potentially saving them thousands of dollars in actual tax liability.

Estimate Your Potential Tax Deductions 🔢

Curious about how much you might be able to deduct using Schedule 1-A? Use this simple, interactive calculator below. (Note: This is a basic estimation tool and assumes you are under the MAGI phaseout limits. Always consult a tax professional for exact figures!)

Schedule 1-A Quick Estimator

Key Takeaways of the Post 📝

To wrap your head around everything we just covered, here is a quick summary of what you need to remember about the 2025 Schedule 1-A:

- You Don’t Have to Itemize: The biggest advantage of the OBBBA is that these deductions can be claimed in addition to your standard deduction.

- Massive Tip Relief: You can deduct up to $25,000 in properly reported tips, protecting your hard-earned service industry money.

- Overtime Gets Rewarded: The “half” premium portion of FLSA overtime can be deducted up to $12,500 ($25,000 for joint filers).

- Buy American Cars: Interest on auto loans is deductible, provided the car was assembled in the USA and is for personal use.

- Senior Support: A $6,000 per person deduction exists for those born before Jan 2, 1961 (up to $12,000 for qualifying joint couples).

The OBBBA Tax Cheat Sheet

Frequently Asked Questions ❓

Disclaimer: I’m a tax enthusiast, not a licensed CPA! The information provided here is for general educational purposes based on the IRS Schedule 1-A instructions for 2025. Tax laws are incredibly nuanced and individual circumstances vary wildly. Always consult with a qualified tax professional before filing.

I hope this breakdown of the new Schedule 1-A deductions helps you keep a little more of your hard-earned cash this tax season! Are you planning to claim any of these new OBBBA deductions? Do you have any lingering questions about how the MAGI phaseouts work? Let me know down in the comments—I’d love to hear your thoughts! 😊