Hobby vs Business: IRS §183 Nine-Factor Test Explained

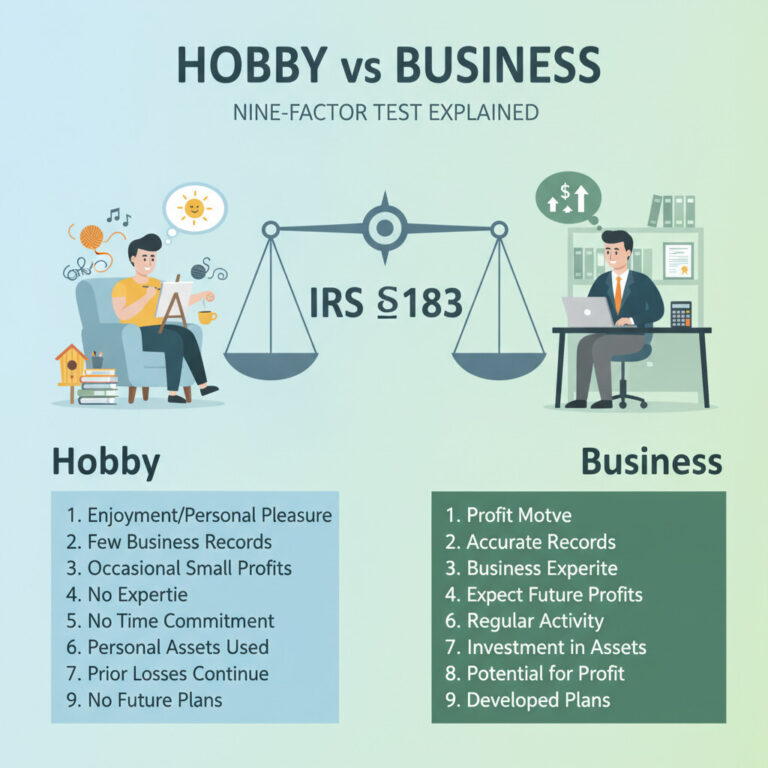

Is your side activity a business or a hobby — and why does it matter to the IRS? Under Internal Revenue Code §183 (the “hobby loss” rule), if an activity is NOT engaged in for profit, you cannot deduct its losses against your other income. A real business reports on Schedule C and can deduct…