Hobby vs Business: IRS §183 Nine-Factor Test Explained

Side income is everywhere now — content creation, consulting, reselling, photography, farming, horses, crafts. The IRS’s hobby vs business determination under §183 decides whether your activity’s expenses and losses are deductible, and it’s a recurring audit issue. This guide walks through the general rule, the nine-factor test the IRS actually uses, the 3-of-5 profit presumption, and how to position a genuine business correctly.

At SW Accounting & Consulting Corp, we help Los Angeles area entrepreneurs, creators, and side-business owners classify activities correctly and document profit motive before the IRS asks. Below: the §183 framework, the nine factors, the presumption, and practical steps.

What is the §183 general rule? 📏

IRC §183(a): for an activity engaged in by an individual or an S corporation, if the activity is NOT engaged in for profit, no deduction attributable to it is allowed — except as §183(b) permits. Under §183(b), deductions are allowed only up to the gross income from the activity; excess deductions cannot offset income from other, unrelated sources.

In plain terms:

- Business — reports on Schedule C; deducts ordinary and necessary expenses; a net loss can offset wages, interest, and other income.

- Hobby — income is fully taxable, but deductions are severely limited and cannot create a loss to shelter other income (and in recent years hobby expenses have been largely nondeductible as miscellaneous itemized deductions — confirm current treatment for your year).

- Scope — §183 applies to individuals and S corporations; it also reaches partnerships (Rev. Rul. 77-320, applied at the partnership level) and is relevant to trusts and estates.

Hobby income is always taxable; hobby losses are not deductible against other income. So the stakes of the classification run one direction: a string of losses you’re deducting against W-2 wages is exactly what draws §183 scrutiny. If the activity is a genuine business, be ready to prove it.

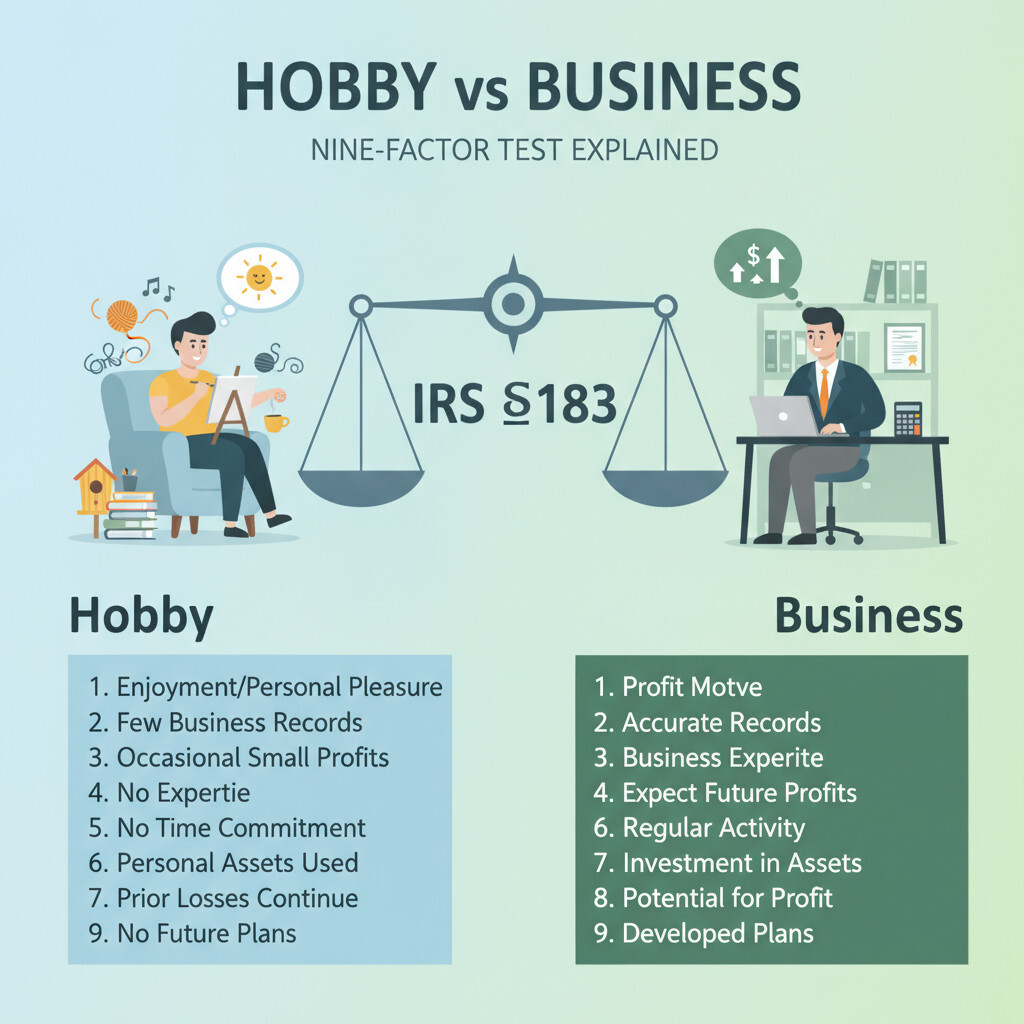

What are the nine factors? 🔍

There is no single test. The IRS weighs nine factors from Treas. Reg. §1.183-2(b), looking at all the facts and circumstances. No factor is decisive, and the list isn’t exhaustive — but these are what examiners actually develop.

| # | Factor | What helps your “business” case |

|---|---|---|

| 1 | Manner in which you carry on the activity | Businesslike: complete books/records, separate bank account, written plan |

| 2 | Expertise of you or your advisors | Study of the field; consulting experts and following their advice |

| 3 | Time and effort expended | Substantial personal time, or hiring competent people to run it |

| 4 | Expectation that assets will appreciate | A profit expectation including appreciation of land/assets used |

| 5 | Success in other activities | Track record of turning similar ventures profitable |

| 6 | History of income or losses | Losses in a startup phase or from external causes, not chronic |

| 7 | Amount of occasional profits | Real profits, even occasional, relative to losses and investment |

| 8 | Financial status of the taxpayer | Not relying on the activity’s losses to shelter substantial other income |

| 9 | Elements of personal pleasure or recreation | Enjoyment alone doesn’t make it a hobby — but heavy recreation weighs against you |

What is the 3-of-5 profit presumption? ✅

IRC §183(d): if an activity’s gross income exceeds its deductions in at least 3 of 5 consecutive tax years (ending with the year in question), the activity is PRESUMED to be engaged in for profit — shifting the burden to the IRS. For activities consisting in major part of breeding, training, showing, or racing horses, the test is 2 of 7 years.

Key points on the presumption:

- It’s a presumption, not a guarantee — the IRS can still rebut it, and failing it doesn’t automatically make the activity a hobby; the nine-factor analysis still governs.

- Horse activities get the easier 2-of-7 test — recognizing the long ramp to profitability.

- Form 5213 election — a taxpayer can elect to postpone the IRS’s profit determination until the end of the presumption period, giving a new activity time to meet the test (this also extends the statute of limitations for the relevant years — weigh the trade-off).

Profit motive is proven with contemporaneous records, not after-the-fact explanations. Keep a separate business bank account, maintain real books, write and update a business plan, track your expertise and the expert advice you followed, and document why early losses occurred and what you changed in response. Factor 1 (businesslike manner) is frequently the tipping point.

How do you protect a genuine business? 🛠

If your activity is a real business reporting losses, build the §183 record before an examiner ever calls.

- Operate like a business — separate bank account and credit card, bookkeeping system, invoices, and a written, updated business plan.

- Show profit-seeking behavior — marketing, pricing changes, cost controls, pivots in response to losses.

- Document expertise — training, credentials, and the experts you consulted and followed.

- Track the numbers — keep the multi-year income/loss history that the presumption depends on; know where you stand against the 3-of-5 (or 2-of-7) test.

- Consider Form 5213 for new ventures — but understand it extends the assessment period for those years.

Frequently asked questions about the hobby loss rule

Yes. Income from a hobby is fully taxable and must be reported. What’s limited is the deductibility of hobby expenses — they generally can’t exceed hobby income and can’t create a loss to offset other income.

Under the §183(d) presumption, profit in at least 3 of 5 consecutive years (2 of 7 for horse breeding/training/showing/racing) presumes a profit motive. Falling short doesn’t automatically make it a hobby — the nine-factor test still applies.

No. Personal pleasure is just one of nine factors. Many profitable businesses are enjoyable. Heavy recreational character weighs against you, but enjoyment alone doesn’t disqualify a genuine profit-seeking activity.

It’s the election to postpone the IRS’s determination of whether the presumption applies until the end of the 5-year (or 7-year) window — useful for a new activity that needs time to become profitable. Note it extends the statute of limitations for assessing those years.

How can SW Accounting help? 💼

At SW Accounting & Consulting Corp, we help LA-area creators, consultants, farmers, and side-business owners classify activities correctly under §183 — building businesslike records, documenting profit motive across the nine factors, tracking the 3-of-5 presumption, advising on the Form 5213 election, and defending business treatment under examination. If you’re deducting losses from a side activity, let’s make sure the record supports it.

📩 Schedule a hobby-vs-business classification review

Disclaimer: This article is for informational purposes only and is not legal or tax advice. Always consult a qualified professional regarding your specific facts. Primary sources: Internal Revenue Code §183; Treas. Reg. §1.183-2(b); IRS Publication 5558 (Activities Not Engaged in for Profit — Audit Technique Guide); Rev. Rul. 77-320; IRS Form 5213.