Receiving startup stock? File this first for tax savings! The 83(b) Election

If you’ve just joined a startup, congratulations! You’ve probably heard the stories—that little piece of paper, that “equity promise,” that could be a lottery ticket. But let’s be real: that same offer letter can be the key to making you a millionaire, or it could land you with a completely unexpected, massive tax bill. It all comes down to understanding what you have and, more importantly, a single decision you have to make *fast*. 😊

I’m going to break down exactly what you need to know about startup stock, the two main types you’ll encounter, and the one tax choice that separates a life-changing payday from an absolute financial nightmare. Let’s dig in.

The Startup Promise: More Than Just a Paycheck 💰

First, you have to put yourself in the shoes of an early-stage startup. They’re scrappy, they’re hungry, but they’re usually not flush with cash. They simply can’t go head-to-head with Google or Apple on salary. So, what’s their secret weapon?

They offer something potentially way more valuable: a piece of the pie. A piece of the company itself.

This is called equity compensation. In simple terms, it’s a non-cash payment that gives you an ownership stake in the company. By giving you this stake, the company makes its success *your* success. When the company’s value goes up, your slice of the pie gets bigger, too. It’s designed to be this incredible win-win for everyone involved.

The Two Paths to Ownership: Options vs. Stock 🗺️

But here’s the first thing you *have* to get right away. Getting equity isn’t just one simple thing. Nope. There are actually two main paths that startups use to grant it, and believe me, the differences between them are absolutely critical.

We’re talking about Stock Options versus Restricted Stock.

Let’s boil this down with an analogy. Think of it this way:

- Stock Options are like reserving your spot. They give you the *right* to buy shares down the road at a price that’s locked in today. It’s a future opportunity.

- Restricted Stock means you get the actual shares and ownership right now, from day one.

The feeling is totally different, and so are the tax implications.

Deep Dive: What Are Stock Options? 🎟️

Let’s dig into stock options first. Honestly, the best way to think about it is like a special coupon. The company gives you this coupon that lets you buy their stock at a fixed price (we call this the “exercise price” or “strike price”), no matter how high the real value of that stock might climb in the future.

This process is a three-step journey:

- Step 1: Grant. This is the official offer. The company grants you the *option* to buy a certain number of shares at a fixed price.

- Step 2: Vesting. You don’t get to use your coupon all at once. Over a period of time (usually a few years), you *earn* the right to use your options. This is called vesting.

- Step 3: Exercise. This is when you make it real. You pull out your *own money*, pay that fixed price, and officially buy the shares. Only at this moment do you become a shareholder.

Here’s the fine print, and it’s crucial. Until you exercise, you don’t own a thing. You’re not a shareholder, and you don’t have any rights. You also have to come up with your own cash to make the purchase, which can be a lot of money!

But here’s the biggest risk: If the company doesn’t do well and the stock’s actual value drops *below* your locked-in exercise price, that coupon is worthless. Your options are, quite literally, worth nothing.

Deep Dive: What Is Restricted Stock? 🎁

Okay, so that’s options. Now let’s talk about the other path, restricted stock. This is a whole different ball game. Instead of giving you the *right to buy* shares in the future, the company just *gives* you the shares on day one.

I like to think of it like being handed a treasure chest, but it unlocks over time. The treasure (the stock) is yours, but you can’t open the chest and sell it just yet.

Here are the key facts about restricted stock:

- You’re an owner now. From the moment you get it, you are a shareholder. You have voting rights, you can get dividends… the whole shabang.

- The “Restriction” is Vesting. The catch is that you can’t just turn around and sell those shares. They are “restricted” until they vest over time (sound familiar?).

- It Protects the Company. This vesting is a safety net for the startup. If you decide to leave after six months, the company has the right to buy back any shares that haven’t vested yet.

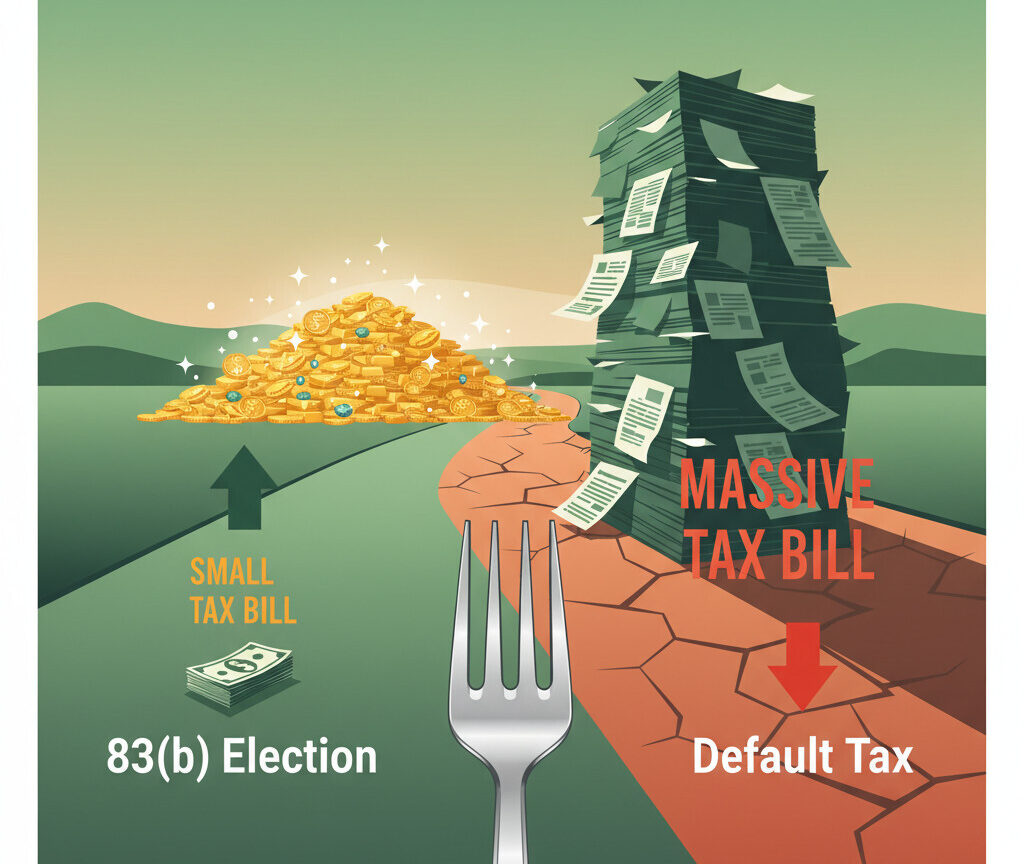

The $100,000 Mistake: Understanding the 83(b) Tax Choice 💸

Okay, everybody, lean in for this part. Because this is where things get really serious. If you get restricted stock, you are immediately faced with a monumental, super time-sensitive tax decision that, frankly, most people don’t even know exists.

Making the wrong choice—or just making *no choice at all*—can be an incredibly costly mistake. This is the costly pitfall.

So let me ask you: you get this stock today, it’s worth something, but it’s restricted for a few years. When do you think the IRS comes knocking for their share? Is it when you *get* it (at grant) or is it when those restrictions finally disappear (at vest)?

The default answer, and I’ll tell you right now, is *not* in your favor.

Case Study: Sarah’s Startup Stock 📝

Let’s walk through a quick story. It’s super simple but really powerful. Sarah joins a brand new startup and gets a grant of 100 shares of restricted stock. Here’s the timeline:

| Event | Time | Price Per Share | Total Value |

|---|---|---|---|

| Grant | Day 1 | $1.00 | $100 |

| Vesting | Year 2 | $1,000.00 | $100,000 |

| Sale | Year 3 | $1,500.00 | $150,000 |

The Tax Nightmare: The Default (No 83(b)) 😱

By default, here’s what happens to Sarah. And honestly, it’s brutal.

The IRS ignores her grant date. They wait until her shares *vest* in Year 2. At that exact moment, her 100 shares are now worth $100,000. The IRS looks at that and says, “Aha! That’s $100,000 of income for you,” and they send her a massive tax bill. This is often called “phantom income” because she hasn’t sold a single share or seen a dime of cash, but she owes taxes as if she just got paid $100,000 in salary.

Tax Calculation (Default Path) 🧮

1) At Vesting (Year 2): Sarah pays Ordinary Income Tax on the full $100,000 value. This is taxed at the highest possible rate, just like her salary. Let’s say her tax rate is 35%.

→ Immediate Tax Bill: $35,000 (due now, with no cash from the stock!)

2) At Sale (Year 3): She sells for $150,000. Her “cost basis” is now $100,000 (the amount she already paid taxes on). So, she only owes tax on the *additional* profit.

→ Profit: $150,000 (Sale) – $100,000 (Basis) = $50,000

→ She pays Capital Gains Tax on $50,000. Let’s say that’s 30%.

→ Second Tax Bill: $15,000

Final Result (Default)

– Total Tax Paid: $35,000 + $15,000 = $50,000

– She lost a third of her total earnings to taxes, and she had to come up with $35,000 in cash long before she ever sold. What a nightmare.

The Smart Move: How the 83(b) Election Saves You 💡

But… what if there was another way? What if you could flip the script? What if you could go to the IRS and say, “Hey, forget about the vesting date. I want you to tax me *now*, on Day 1, when my stock is only worth $100 total”?

Well, that is *exactly* what something called the 83(b) Election lets you do.

By filing this simple piece of paper, Sarah tells the IRS to treat the $100 grant value as her income for the year. The tax on $100 is tiny, maybe $35. But look at what happens next.

Tax Calculation (With 83(b) Election) 🧮

1) At Grant (Day 1): Sarah files her 83(b) and pays Ordinary Income Tax on the $100 value.

→ Immediate Tax Bill: $35

2) At Vesting (Year 2): The stock is now worth $100,000. How much tax does she owe?

→ Tax Bill: $0.

That’s right. Zero. By filing the 83(b), she told the IRS to ignore the vest date. It’s no longer a taxable event.

3) At Sale (Year 3): She sells for $150,000. Her “cost basis” is the $100 she paid tax on at the start.

→ Profit: $150,000 (Sale) – $100 (Basis) = $149,900

→ She pays Long-Term Capital Gains Tax on $149,900. This rate is *much lower* than ordinary income tax. Let’s say it’s 20%.

→ Second Tax Bill: $29,980

Final Result (With 83(b))

– Total Tax Paid: $35 + $29,980 = $30,015

– By filing one form, Sarah saved herself nearly $20,000 and, just as importantly, avoided the “phantom income” tax bomb at vesting.

Let’s be crystal clear about what this is. The 83(b) Election is basically just a letter you send to the IRS. You are officially *choosing* (electing) to pay taxes on your restricted stock at its grant date value, not its future vest date value.

The magic of this is that it ensures all that future growth—all that appreciation from $1 to $1,500—gets treated as a long-term capital gain, which is almost always taxed at a much, much lower rate than ordinary income.

The Most Important Deadline: Your 30-Day Window ⏰

I absolutely cannot stress this enough. This is not a choice you can put off. You don’t have forever to think about it. You have an incredibly short, brutally strict window of time to act.

You have exactly 30 calendar days.

I repeat: 30 CALENDAR DAYS. Not business days. 30.

From the date your stock is officially granted, you have 30 days to get your 83(b) election filed with the IRS.

There are no extensions, no do-overs, and no “pretty please.” If your form shows up on day 31, it’s too late. You will have permanently and forever lost the chance to save what could be tens or even hundreds of thousands of dollars in taxes.

Your 83(b) Action Plan (Checklist) ✅

So, this is your playbook. This is what you do. The *very moment* you receive a restricted stock grant, your 30-day clock starts ticking.

- Day 1: Get the Grant. The clock is now running.

- Day 1 (Still): Act Immediately. Talk to your company’s HR or legal department. Talk to your personal tax advisor. Tell them you need to file an 83(b) election.

- Day 2: Get and Fill Out the Form. Your company should provide the form. It’s a simple, one-page letter. Fill it out accurately.

- Day 3: Mail it via CERTIFIED MAIL. Do not just drop it in a mailbox. You *must* send it via certified mail with a return receipt. This is your non-negotiable proof that you sent it on time.

- Special Note: If you are not a US citizen, you might have even more paperwork, so it’s even more urgent to act fast.

Your 83(b) Quick Guide

Conclusion: The Choice is Yours 🚀

Look, at the end of the day, this is on you. Your company provides the incredible opportunity with the equity, but figuring out the taxes? That responsibility is yours.

Making an 83(b) election is one of the single highest-leverage financial decisions you can make in your entire startup career. It’s the difference between a massive win and a massive, unexpected tax bill. The choice is yours. What will you do in the next 30 days? 😊