U.S. Residents with Non-Resident Family: Avoid Stock Sale Taxes with ‘This Method’

Imagine this: you’ve got a massive tax bill staring you in the face, maybe even millions of dollars, and you could just… make it go away. Legally. It sounds completely backward, doesn’t it? How can a *gift*, something you’re giving away for free, end up saving you a fortune in taxes?

Well, it’s all tucked away in a clever corner of the U.S. tax code. Today, we’re going to break down a really powerful strategy that global families use to do exactly that. We’re talking about huge investment gains, relatives living overseas, and literally millions of dollars on the line. Let’s dive in and see how it works. 😊

The Billion-Dollar Problem: Appreciated Assets 📈

To really get the solution, we’ve got to start with the problem. And look, it’s what you’d call a “good problem to have,” but it’s a huge one nonetheless. Let’s picture this: a father, who is a U.S. resident, had the incredible foresight to buy stock in a company like, say, Apple, way, way back in the day.

Fast forward to today, and that stock is worth an absolute fortune. But here’s the catch: if he decides to sell it to cash in on that amazing investment, he’s looking at a monster capital gains tax bill from Uncle Sam. So, the real question becomes, how does he unlock all that value without handing over a massive chunk of it to the taxman?

The Creative Solution: A Multinational Family 🌎

This is where the strategy gets really creative. What if the father doesn’t sell the stock at all? What if he just… passes the torch to someone else in the family to handle the sale? This is where things start to get really interesting.

Let’s add one more crucial piece to the puzzle: his son is not a U.S. resident. He lives in another country. So, the father gifts this super valuable, highly appreciated stock to his son. Then, the son turns around and sells it. Does that simple move really let them side-step that huge U.S. tax bill? Can you even do that? Is it legal?

The short answer is, yes, it can absolutely work. Under the right set of circumstances, this strategy is totally legal and can be unbelievably effective. It all comes down to a combination of two completely separate parts of the U.S. tax code.

The Two Key Tax Rules That Make It Work 🔑

So, how on earth is this possible? It’s not one single rule, but two key principles of U.S. tax law that, when put together, create this amazing opportunity.

Rule 1: The Capital Gains Tax Discrepancy

First up, we’ve got capital gains tax. This one’s pretty simple: when you sell an asset (like stock or real estate) for more than you paid for it, the government wants its cut of that profit. That’s the tax.

But here is where the magic happens. The rules are completely different for U.S. residents versus non-residents. This one little difference is “the whole game right there.”

| Person | U.S. Capital Gains Tax Rule |

|---|---|

| U.S. Resident (The Father) | Gets taxed on his investment gains from *anywhere in the world*. |

| Non-Resident (The Son) | Is generally not taxed by the U.S. on gains from selling U.S. stocks. |

Rule 2: The U.S. Gift Tax (and its Giant Exemption)

Okay, so we’ve established that if the son sells, there’s no U.S. capital gains tax. Great. But wait a minute, what about the act of the father *giving* the stock to his son in the first place? That brings us to our second big rule: the U.S. Gift Tax. This is a tax specifically designed to catch these huge transfers of wealth between people.

So, what’s the workaround for the gift tax? Well, here’s the thing: you don’t get *around* it. You use the absolutely massive exemption that’s built right into the tax code.

For 2024, every single U.S. resident has a lifetime gift and estate tax exemption of… get this… $13.61 million. Just let that number sink in. This means our dad in the story can gift up to that entire amount over his lifetime without paying “one red cent in U.S. gift tax.”

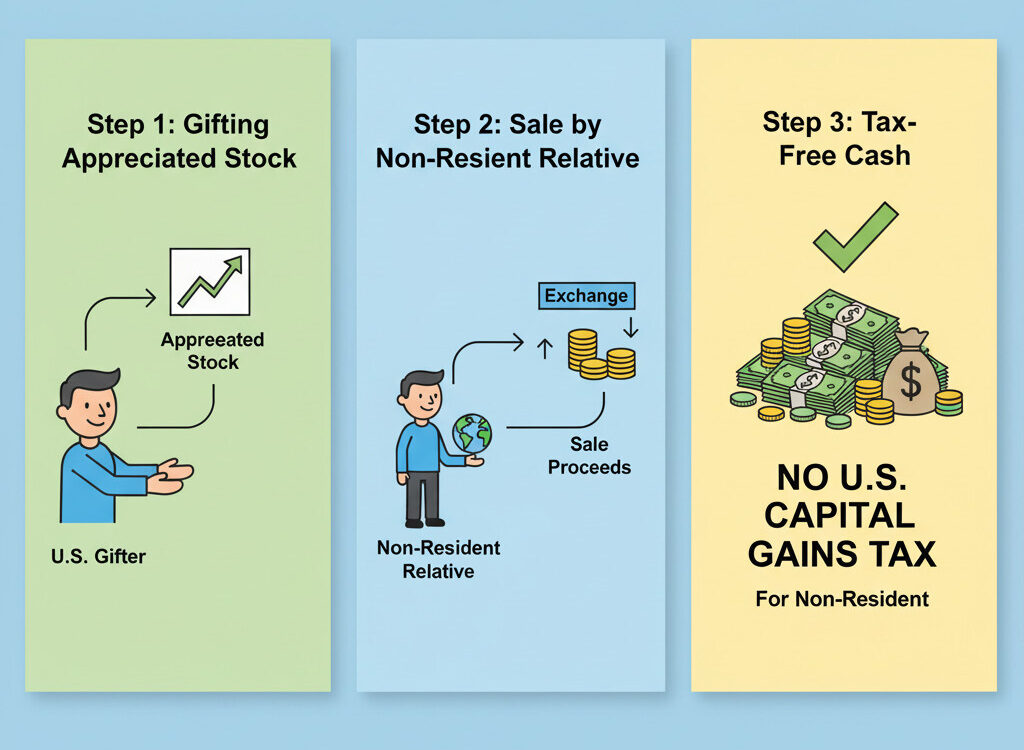

The 3-Step Tax-Free Playbook 📋

So now we have our two key puzzle pieces. Let’s put it all together and look at the actual playbook. Here’s the whole strategy in three simple steps.

The 3-Step Strategy 📝

- Step 1: Father Gifts. The U.S. father gifts the appreciated stock to his non-resident son. He uses a piece of his lifetime exemption, so… boom, no gift tax.

- Step 2: Son Owns. The son, living abroad, is now the official, legal owner of that stock.

- Step 3: Son Sells. The son sells the stock. Because he’s a non-resident, he pays $0 in U.S. capital gains tax.

The Final Result

The result is incredibly powerful. The family has successfully taken all that massive growth in the stock, turned it into cash, and legally sidestepped the entire U.S. capital gains tax bill that the father would have been on the hook for.

What to Watch Out For: The Critical Fine Print ⚠️

I know what you’re thinking. This sounds almost too good to be true. And while it is incredibly effective, I have to be really clear here: this is not a do-it-yourself weekend project. There are some huge potential landmines and critical details that you absolutely have to know about before you’d ever even dream of trying something like this.

Let’s get into the all-important fine print. First, a couple of key details:

- Reporting is Required: This is not done in secret. The father *absolutely must* file a gift tax return with the IRS to report the whole thing.

- Alternative Structure: It doesn’t just have to be a person-to-person gift. This can also work if the gift is made to a properly set up *foreign trust*.

But the most important point of all is the one that’s most often overlooked. Everything we’ve talked about so far only looks at U.S. law.

This brings us to the single most critical warning: You could execute a plan that is brilliant for U.S. tax purposes, but it could be an absolute financial disaster in the son’s home country. What happens when the son actually *receives* that gift or *sells* that stock in his country? His country’s tax laws could take your brilliant plan and turn it into a mess on his end.

Conclusion: Is This Loophole Right for You? 📝

So, what’s the bottom line? The takeaway is pretty clear: this gifting loophole can be an amazing tool for families spread across the globe. But it is not simple. It “demands a totally comprehensive, multinational strategy.”

It’s not just about solving the U.S. tax problem; it’s about making sure that solution doesn’t create a bigger problem somewhere else. So the final, multi-million dollar question is: is your plan *really* considering all the angles? If you’re in this situation, this is not a time for DIY. It’s time to talk to professionals who understand *both* sides of the equation.