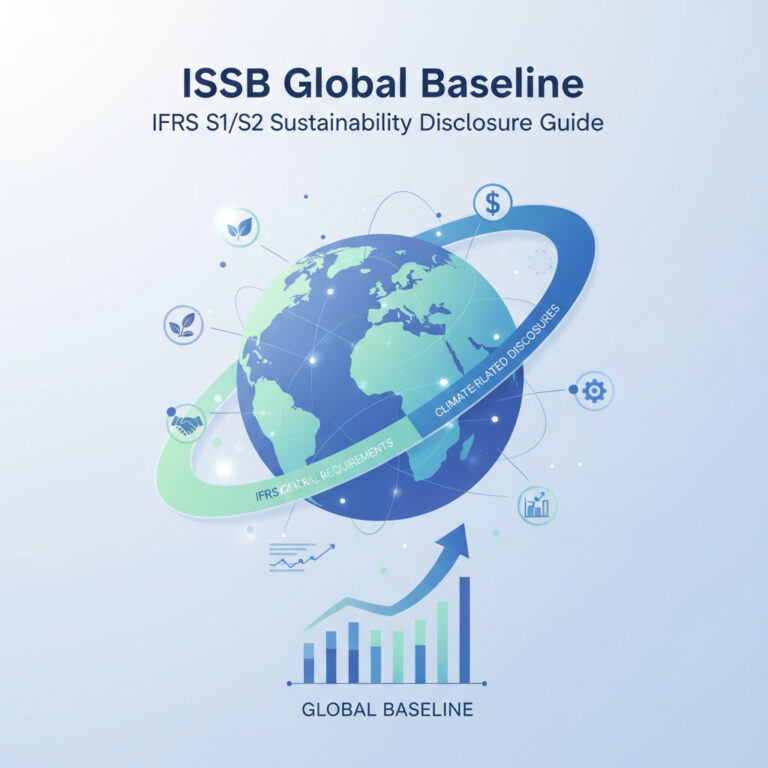

ISSB Global Baseline: IFRS S1/S2 Sustainability Disclosure Guide

What is the ISSB global baseline for sustainability disclosure, and why does it matter in 2026? The International Sustainability Standards Board (ISSB) — established by the IFRS Foundation — issued IFRS S1 (general sustainability-related financial disclosures) and IFRS S2 (climate-related disclosures) as a global baseline for how companies report sustainability information to investors. By 2026,…