Scope 3 Supplier Emissions for SB 253: 5-Step Vendor Engagement Guide

For most companies, Scope 3 emissions account for roughly 75% of total carbon footprint — and for some categories of business, over 90%. That’s the punchline. You can decarbonize your own factories and switch to renewable electricity (Scope 1 and 2) and still leave the vast majority of your climate impact untouched. The CARB-enforced Scope 3 emissions reporting mandate under SB 253 is therefore not just a compliance exercise; it’s the part of climate accounting that actually moves the needle.

At SW Accounting & Consulting Corp, we work with Los Angeles area finance and sustainability teams preparing for SB 253’s 2027 Scope 3 disclosure deadline. Below: what SB 253 requires for Scope 3, what the GHG Protocol Standard actually says, the five-step program our clients use to engage suppliers, and what audit-ready means in practice.

What does SB 253 require for Scope 3 reporting? 🌍

SB 253 (Health & Safety Code §38532) requires reporting entities — U.S. companies with annual revenues over $1 billion doing business in California — to publicly disclose Scope 1, 2, and 3 greenhouse gas emissions annually. Scope 1 and 2 are due beginning January 1, 2026 (for fiscal year 2025 emissions). Scope 3 begins January 1, 2027 (for fiscal year 2026 emissions).

Key statutory requirements (from leginfo.ca.gov):

- Scope of disclosure — annual emissions across Scope 1 (direct), Scope 2 (purchased energy), Scope 3 (value chain), measured per the GHG Protocol Corporate Standard and GHG Protocol Corporate Value Chain (Scope 3) Standard.

- Assurance — Scope 1 and 2 require limited assurance starting 2026, transitioning to reasonable assurance by 2030. Scope 3 requires limited assurance starting 2030.

- Public disclosure — reporting entities must publicly disclose on a digital platform created by CARB; data is publicly searchable.

- Penalties — administrative penalties up to $500,000 per reporting year for non-compliance, enforced by the California Air Resources Board (CARB).

SB 253 provides limited safe harbor for the first Scope 3 reporting year (2027 disclosures based on 2026 data): CARB shall not impose penalties on misstatements for Scope 3 if disclosure is made with a reasonable basis and in good faith. This safe harbor is narrow — it does not excuse failure to file, missing categories, or use of methodologies inconsistent with the GHG Protocol. Document your methodology choices and the limits of your supplier data NOW.

What does the GHG Protocol require? 📊

The GHG Protocol Corporate Value Chain (Scope 3) Standard breaks value chain emissions into 15 categories. SB 253 incorporates this Standard by reference — you cannot pick your own methodology.

| Upstream Categories (1-8) | Downstream Categories (9-15) |

|---|---|

| 1. Purchased goods and services 2. Capital goods 3. Fuel- and energy-related activities 4. Upstream transportation and distribution 5. Waste generated in operations 6. Business travel 7. Employee commuting 8. Upstream leased assets | 9. Downstream transportation and distribution 10. Processing of sold products 11. Use of sold products 12. End-of-life treatment of sold products 13. Downstream leased assets 14. Franchises 15. Investments |

For most non-financial companies, Categories 1 (purchased goods/services), 4 (upstream transport), 11 (use of sold products), and 12 (end-of-life) dominate. For financial institutions, Category 15 (financed emissions) is almost everything. Identify your “hot” categories first — don’t spread audit effort evenly across 15 buckets when 80% of emissions are in 3 of them.

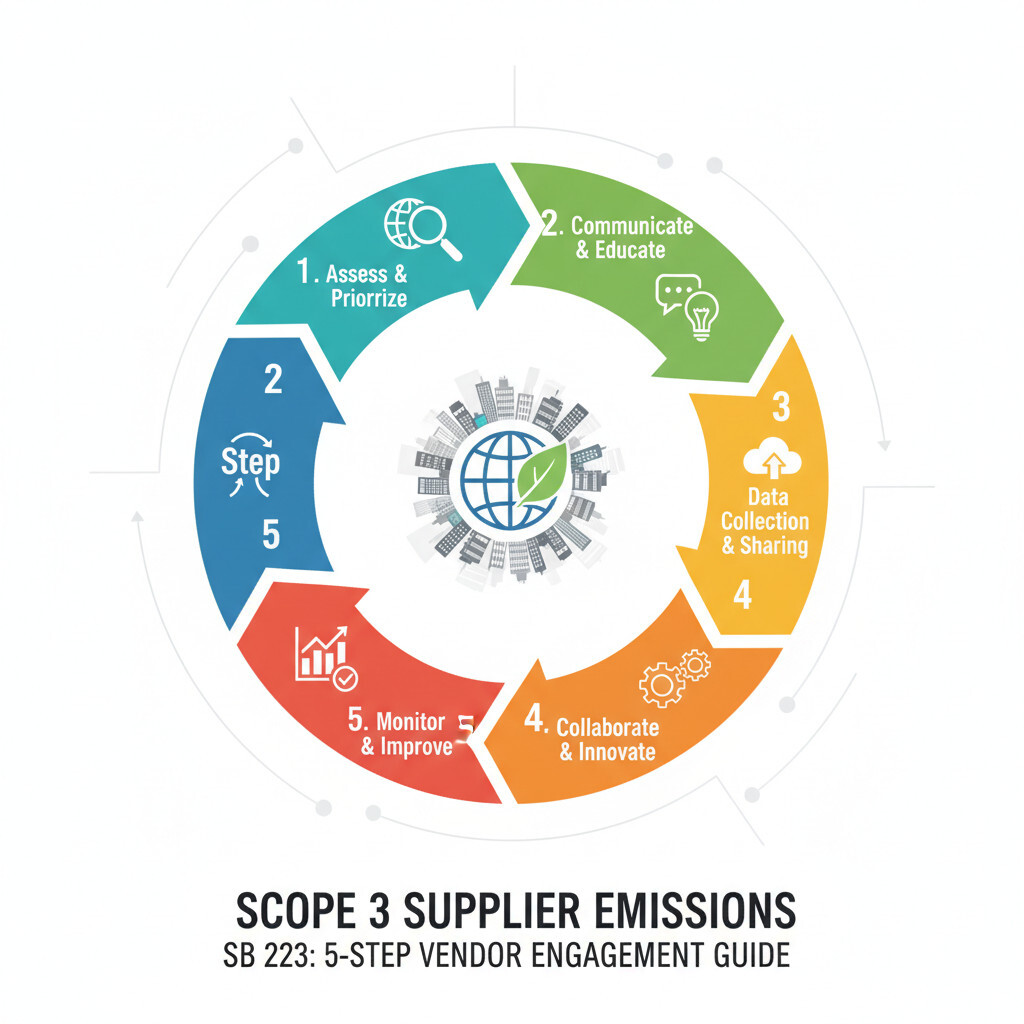

What 5-step supplier engagement program works? 🤝

The GHG Protocol expects a data-quality hierarchy: supplier-specific primary data (best) → industry-average secondary data → spend-based estimates (last resort). Audit assurance increases when you move higher in the hierarchy for material categories.

| Step | Action | Output |

|---|---|---|

| 1. Screen | Run a spend-based or sector-average screen across all 15 categories | Initial inventory; identify material categories (typically >5% of total Scope 3) |

| 2. Prioritize | Rank suppliers within material categories by spend or emissions exposure | Top 20-30 suppliers covering 80% of emissions |

| 3. Engage | Send standardized questionnaire (CDP Supply Chain or equivalent) to priority suppliers | Supplier-specific activity data + emission factors |

| 4. Contract | Embed disclosure obligations in supplier contracts and codes of conduct | Sustained year-over-year supplier participation |

| 5. Verify | Sample supplier-provided data for limited assurance; document methodology choices | Audit-ready inventory; lower assurance risk in 2030 |

The biggest failure pattern: companies wait until they have primary data from every supplier before reporting. The GHG Protocol explicitly anticipates an evolution from estimates to primary data over multiple reporting cycles. Filing with a defensible spend-based estimate in 2027 — and a documented plan to migrate top suppliers to primary data over the next three cycles — is materially safer than missing the deadline.

What does audit-ready look like? 🔍

Limited assurance under ISAE 3000 / AICPA SSAE 18 attestation standards is the SB 253 default starting 2030. Auditors will trace material Scope 3 numbers to the underlying methodology, data sources, and supplier records.

Documentation required at minimum:

- Boundary memo — which entities are in/out of the reporting boundary, which categories are screened in/out, why.

- Methodology log — for each material category, which calculation method (spend-based, average-data, supplier-specific) and why.

- Emission factor registry — every emission factor used, its source (EPA, IEA, ecoinvent, supplier-provided), version date, and applicability.

- Supplier data files — raw questionnaire responses or supplier-supplied calculation files, retained per record retention policy.

- Sample testing — auditor selects a sample of suppliers and re-performs the emissions calculation.

Frequently asked questions about Scope 3 emissions reporting

SB 253 applies to U.S. companies with annual revenues exceeding $1 billion that do business in California. There is no separate Scope 3 threshold — if you’re a reporting entity, you must report all three scopes.

Reporting begins January 1, 2027 for fiscal year 2026 emissions. Limited assurance is required beginning 2030.

SB 253 incorporates the GHG Protocol Corporate Value Chain (Scope 3) Standard by reference. You cannot use a non-GHG-Protocol methodology.

Use spend-based or industry-average estimates for non-responsive suppliers and document the limitation in your methodology log. Plan to escalate via contract language in the next renewal cycle.

How can SW Accounting help? 💼

At SW Accounting & Consulting Corp, we help LA finance and sustainability teams build SB 253-compliant Scope 3 inventories — supplier prioritization, GHG Protocol methodology design, documentation packs ready for limited assurance, and integration with your existing financial close calendar. We work alongside your sustainability team, not in place of them.

📩 Schedule a Scope 3 readiness consultation

Disclaimer: This article is for informational purposes only and is not legal, tax, or accounting advice. Always consult a qualified professional regarding your specific facts. Primary sources: California Health & Safety Code §38532 (SB 253), CARB rulemaking, GHG Protocol Corporate Value Chain (Scope 3) Standard.

Need help with SB 253 or climate disclosure? SW Accounting provides framework advisory, vendor data readiness, and formal CPA assurance (SSAE AT-C 210 / ISAE 3410). Explore our ESG & Climate Disclosure services →