The Home Sale Tax Break: How to Make $500k Tax-Free (The ‘2-in-5’ Rule Explained)

Selling your home is a huge financial moment, right? It’s often the biggest transaction of our lives. You watch the market, you fix the place up, and you finally get that amazing offer. But then, a nagging thought creeps in: “How much of this profit does the IRS get to keep?”

I get it. The idea of handing over a huge chunk of your hard-earned equity in taxes is painful. But what if I told you there’s a way for most homeowners to pocket a massive amount of that profit, completely tax-free? I’m talking about the home sale tax break, also known as the Section 121 exclusion. It’s an incredible benefit, but it’s also surrounded by some major confusion. Let’s dive in and clear it all up! 😊

What is the Home Sale Tax Break, Anyway? 💰

At its core, this tax break is beautifully simple. When you sell an asset for more than you paid for it, that profit is called a **”capital gain.”** Usually, you have to pay capital gains tax on that profit.

For example, if you bought a stock for $10,000 and sold it for $15,000, you have a $5,000 capital gain that you’ll be taxed on. But your main home is special. The government wants to encourage homeownership, so it created a rule that lets you *exclude* a huge portion of that gain from your income.

Here are the magic numbers:

- If you’re married filing jointly, you can exclude up to $500,000 of profit.

- If you’re a single filer, you can exclude up to $250,000 of profit.

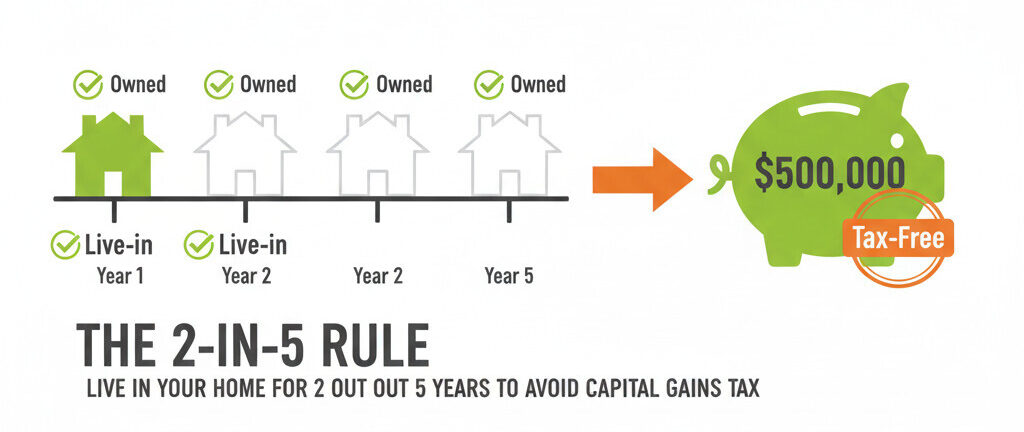

Let that sink in. A married couple could buy a home, live in it, and sell it later for a $500,000 profit… and pay zero dollars in federal tax on that gain. It’s honestly one of the best wealth-building tools available to the average person. But to get it, you have to follow the rules. And the most important one is the “2-in-5” rule.

The ‘2-in-5’ Rule: The Heart of the Exclusion ❤️

This is the single most important part of the entire tax break. To qualify for the full $250,000/$500,000 exclusion, you must pass two tests within the 5-year period leading up to the date of your home’s sale.

- The Ownership Test: You must have owned the home for at least two years (24 months or 730 days) during that 5-year period.

- The Use (Residency) Test: You must have lived in the home as your main home for at least two years during that 5-year period.

The 5-year window is a “look-back” from the day you close the sale. For example, if you sell your home on October 30, 2025, the 5-year period is from October 30, 2020, to October 30, 2025. Somewhere in that window, you need to have met both the 2-year ownership and 2-year residency requirements.

Here’s a great pro-tip: The two years of owning and the two years of living do not have to be the same two years! They also don’t have to be one continuous block of time. As long as you rack up a *total* of 24 months for each test somewhere in that 5-year window, you’re good to go.

What counts as your “main home”? It’s the one you live in most of the time. The IRS can look at things like your driver’s license, voter registration, and the address on your tax returns to determine which property is your primary residence.

Myth #1: “The Break is Prorated Based on Time” (Wrong!) 📊

This is one of the biggest and most costly myths I hear. People assume that if they live in the house for, say, two out of the five years they owned it, they must get 2/5ths (or 40%) of the tax break. It just *feels* logical, doesn’t it?

Well, I’m here to tell you that’s completely wrong.

The home sale tax break is NOT prorated based on your time there. It is a simple “all or nothing” test. You either meet the 2-year residency rule and qualify for the *full* $250,000/$500,000 exclusion, or you fail the test and get $0.

Let’s look at a practical example. This is where timing is everything.

📝 Case Study: The 5-Year Timeline

Imagine you buy a house on January 1, 2020. You plan to sell it on January 1, 2025 (exactly 5 years later). Here’s how you used it:

- Year 1 (2020): Owned, Rented Out

- Year 2 (2021): Owned, Rented Out

- Year 3 (2022): Owned, Lived In

- Year 4 (2023): Owned, Lived In

- Year 5 (2024): Owned, Rented Out

The Result:

You PASS the test! In the 5-year look-back period, you owned the home for 5 years (passes the 2-year ownership test) and you lived in it for a grand total of 2 years (passes the 2-year use test). You don’t get 2/5ths of the break—you get the ENTIRE $250k/$500k exclusion. You get all the money, even though you were renting it out right before you sold it!

This “all or nothing” rule is a crucial distinction. The only time proration *does* come into play is if you have to move early due to a few specific exceptions, like a new job, health reasons, or other unforeseen circumstances. In that case, you *may* be eligible for a partial exclusion, but that’s a different rule for a different day.

Myth #2: “It’s a Once-in-a-Lifetime Deal” (Nope!) 🔄

This myth is a stubborn one, and it’s usually passed down from our parents or grandparents. Why? Because it used to be true!

Before 1997, the tax law was different. There *was* a one-time $125,000 exclusion, but you had to be over age 55 to claim it. If you were younger or had already used it, you were out of luck. But that law is long gone!

Here’s the modern rule: You can use this incredible tax break over and over again. There is no limit to how many times you can use it in your lifetime.

The only real catch is a “cooldown” period. You generally cannot use the exclusion if you already used it for another home sale within the past two years.

This “repeatable” nature turns the tax break into a powerful wealth-building strategy. Think about it:

- You buy a home and live in it for 2 years (meeting the rule).

- You sell it and take your tax-free profit.

- You roll that profit into a new home, live there for 2 years…

- …and you can do the whole thing all over again. It’s not a once-in-a-lifetime ticket; it’s a repeatable strategy.

The Duplex Dilemma: What About Mixed-Use Properties? 🏠/💼

This is where things get really interesting. What happens when your “home” is also an “investment”? The most common example is a duplex, where you live in one unit and rent out the other.

Does the IRS look at this as one single building? Nope. They see it as two separate things: your home and your investment property. And they treat the tax implications very differently.

The rule is simple: The tax break only applies to the part of the property you actually use as your main home. The other part is treated like any other rental property, and the profit from it is subject to capital gains tax.

Let’s break it down with a super-simple 50/50 split example:

Duplex Sale Example

| Category | Total | Residential Half (Your Home) | Rental Half (Investment) |

|---|---|---|---|

| Sale Price | $900,000 | $450,000 | $450,000 |

| Cost Basis (Purchase Price) | $300,000 | $150,000 | $150,000 |

| Profit (Gain) | $600,000 | $300,000 | $300,000 |

| Tax Break Applies? | – | YES (Tax-Free!) | NO (Taxable) |

As you can see, you get to walk away with that $300,000 gain from your residential side completely tax-free (assuming you met the ‘2-in-5’ rule). But that other $300,000 gain from the rental side is considered investment income, and you’ll owe capital gains tax on it.

Here’s one more critical point for rental property: If you’ve been renting part of your home, you’ve (hopefully) been taking depreciation deductions on your taxes each year. This is a great benefit, but it has a catch. When you sell, the IRS wants that tax benefit back. You must pay a “depreciation recapture” tax on all the deductions you took. This is a separate tax from the capital gains tax. Please, if you’re in this situation, talk to a tax professional!

Home Sale Tax Break: Core Rules

Conclusion: Home or Financial Tool? 📝

When you really understand these rules, it completely changes how you look at your property. It stops being just a place to live and becomes one of the most powerful wealth-building tools you own. That $500,000 tax-free exclusion is a benefit most investments simply don’t have.

So, I’ll leave you with this question: Is your house just a home, or is it a powerful financial tool that you’re using to its full potential? When you know the rules, you can make smarter decisions that can set you up for a much brighter financial future.

This stuff can be confusing, I know! If you have any questions about your specific situation, feel free to ask in the comments. And it’s *always* a good idea to run your numbers by a qualified tax advisor. 😊