How to Legally Offset Your W-2 Income with Real Estate

Ever get that sinking feeling after looking at your paycheck, seeing how much went to taxes, and thinking, “There *has* to be a better way”? If you’re a high-income earner, that feeling is probably all too familiar. You hear stories about wealthy investors using real estate to pay almost nothing in taxes, and it sounds almost too good to be true.

What if you could take your $200,000 salary and legally use a $200,000 “paper loss” from a rental property (thanks to a magic thing called depreciation) to make your taxable income… zero? Well, I’m here to tell you it *is* possible. But, it’s not simple. The IRS has built a massive, invisible wall to stop most people from doing exactly that. But the key word is *most*. Today, we’re going to talk about that wall, and more importantly, the three paths you can take to get around it. 😊

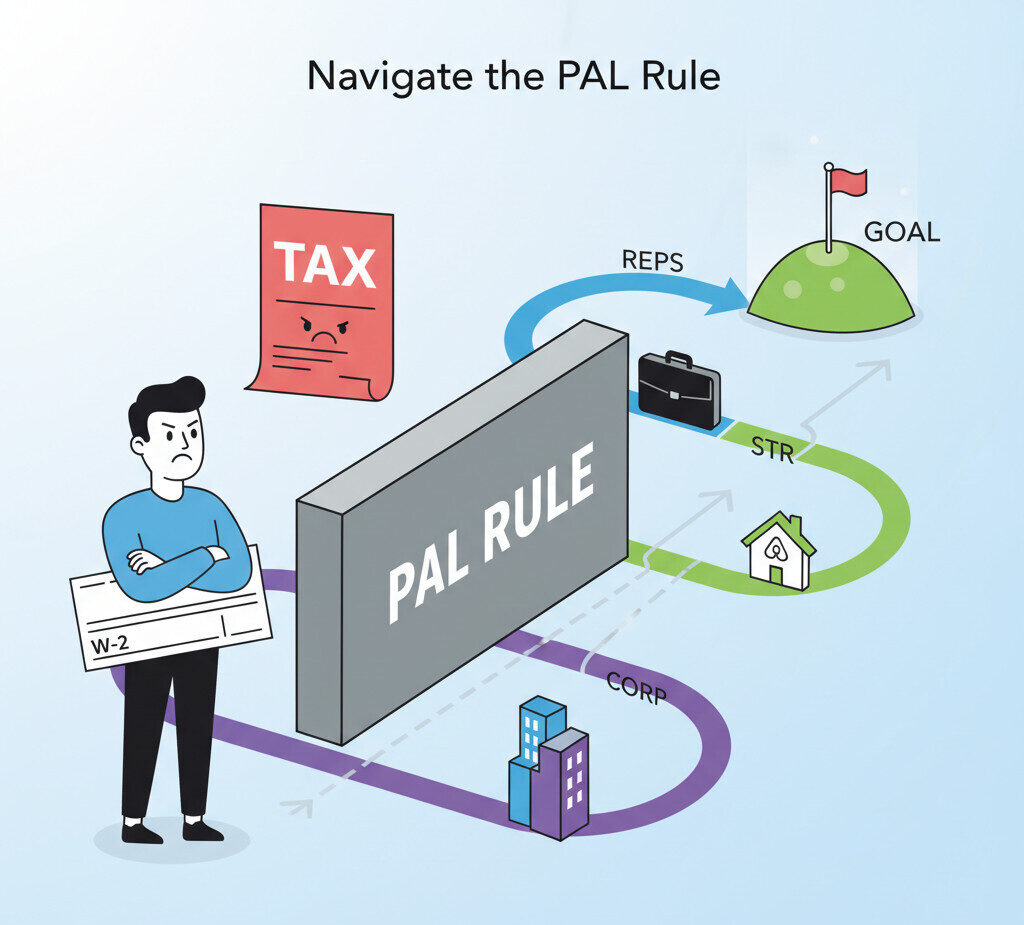

The IRS’s “Great Wall”: The Passive Activity Loss (PAL) Rule 🤔

Before we get to the fun stuff (the “loopholes”), we have to understand the problem. The IRS knows all about this strategy, and back in the 80s, they created the **Passive Activity Loss (PAL) Rule** to shut it down for most taxpayers.

Here’s the core concept: The IRS splits your financial life into two separate buckets:

- Active Income (or “Non-Passive”): This is money you actively work for. Think of your W-2 salary from your 9-to-5 job or the profits from a business you own and operate daily.

- Passive Income: This is money you earn from activities you *don’t* materially participate in. By default, the IRS throws almost *all* rental real estate into this bucket, regardless of how much you “manage” it on the side.

Think of these as two separate bank accounts. The PAL rule is like a bank teller who refuses to let you transfer money between them to cover a loss. The losses you generate in your “Passive” account (like that big paper loss from depreciation on your rental) can *only* be used to offset gains in that *same* “Passive” account. They get “stuck” there, unable to touch your “Active” income.

The Two-Bucket Problem

| Bucket 1: Active Income 🏃♂️ | Bucket 2: Passive Income passively 🛌 |

|---|---|

| W-2 Salary | Rental Property Income |

| Business Profit (you run) | Rental Property (Paper) Loss |

| Consulting Fees | Limited Partnership Income |

If you have $200,000 in W-2 Salary (Active) and a $200,000 Rental Loss (Passive), the PAL rule says your taxable income is… still $200,000! The $200k loss is “suspended” and carried forward until you either have passive *income* or sell the property. This is the default for 99% of people.

So, how do we get around this? We need to find a way to legally re-characterize those passive losses as *active* losses. And there are three main paths to do it.

Path 1: The “Golden Ticket” (Real Estate Professional Status) 👩💼👨💻

This is the most well-known path, the “golden ticket” from the IRS that lets you tear down the wall completely. It’s called the **Real Estate Professional Status (REPS)**. If you qualify, the IRS basically agrees that real estate *is* your active job, so your rental losses are now active losses. That $200k loss can now directly wipe out your $200k W-2 income (or your spouse’s!).

But… and this is a *massive* but… the tests to qualify are incredibly strict. You must meet *both* of these:

- The 750-Hour Test: You must spend more than 750 hours per year in “real property trades or businesses.” This is about 15 hours a week, every single week.

- The >50% Test: More than half of *all* your personal service time (i.e., all your working time) must be spent in those same real estate activities.

Let’s be honest: if you’re a doctor, a lawyer, a software engineer, or anyone with a demanding full-time W-2 job, it is practically impossible to meet the >50% test. If you work 2,000 hours a year at your day job, you’d need to work 2,001 hours in real estate. That’s two full-time jobs. For most high-income earners, this path is a non-starter.

Path 2: The “STR Loophole” (Short-Term Rentals) 🏡

Okay, so if Path 1 is out, what’s next? This is my favorite one because it’s a clever workaround that *doesn’t* require you to be a full-time real estate pro. It’s all about **re-classifying your property.**

Remember how the PAL rule applies to “rental activities”? Well, what if you could run your property in a way that the IRS no longer *sees* it as a “rental activity” but instead sees it as an **active business** (like a hotel)? If it’s not a “rental,” the PAL rules don’t automatically apply! The wall just… crumbles, *for that specific property*.

So, how do you do this? You have to meet one of two tests:

- Test 1: The 7-Day Rule. The average period of customer use for your property is **7 days or less**. This is your classic Airbnb or VRBO vacation rental.

- Test 2: The 30-Day Rule. The average period of customer use is **30 days or less**, AND you provide “substantial personal services” to the guests. (Think: daily cleaning, airport shuttles, providing meals. Just cleaning *between* guests doesn’t count).

If you meet that 7-day test (which many vacation rentals do), you’ve successfully reclassified your property. It’s now a “business.”

Wait! There’s One More Hoop: “Material Participation”

Just classifying it as a business isn’t quite enough. To use the losses against your *active* W-2 income, you still have to prove you **”materially participated”** in this new STR *business*. If you just buy an Airbnb and let a management company do 100% of the work, it’s still passive.

You must prove you’re the one *actually running the show*. The IRS offers 7 tests for this, but the most common ones for STR owners are:

- The 500-Hour Test: You (or your spouse) spent more than 500 hours on the business in the tax year.

- The 100-Hour Test: You spent more than 100 hours, *and* that was more time than *any other individual* (like your cleaner or property manager).

- The “Substantially All” Test: You (or your spouse) did substantially all of the work for the activity.

If you self-manage your STR (handle bookings, coordinate cleaners, answer guest questions) you can often hit that 100-hour test. If you do, congratulations! Your STR is an active business you materially participate in. Those big paper losses (especially from a Cost Segregation study) can now flow right through and offset your W-2 income.

This strategy has a huge trade-off. Because your STR is now a “business,” any *profits* you make are no longer simple rental income. They are now considered **active business income**, which is subject to **Self-Employment Tax** (about 15.3% for Social Security and Medicare). This is a big con, and you must weigh it against the potential tax-shield benefits from the losses.

Path 3: The Corporate Strategy (For Business Owners Only) 📊

This last path is different. It’s *not* for W-2 earners. This is for people who own their own active business (like an S-Corp or C-Corp).

The logic here is that the PAL rules are written to apply to *individuals*. The game changes when a *corporation* owns the real estate. The strategy is to have your corporation own both your active business (e.g., your consulting firm) AND your real estate investments (e.g., a rental property portfolio).

Inside that single corporate entity, the “wall” doesn’t exist in the same way. The passive paper losses from the real estate can be used to offset the active profits from your business, lowering your corporation’s overall taxable income.

| What this strategy CAN offset: | What this strategy CANNOT offset: |

|---|---|

| ✅ Your corporation’s active business profits. | ❌ Your personal W-2 salary. |

| ✅ Your spouse’s business profits (if in the same corp). | ❌ Your spouse’s W-2 salary. |

But, of course, the IRS has roadblocks for this, too. The PAL rules *do* come roaring back into the picture for two specific types of corporations:

The PAL rules *still apply* (and this strategy won’t work) if your company is a:

- Closely Held Corporation: Where 5 or fewer people own more than 50% of the company (which is… most small businesses).

- Personal Service Corporation (PSC): This covers most professional practices, like law firms, medical practices, accounting firms, consulting, and architecture.

Don’t Forget the “Default” Win! (No Strategies Needed) 💰

Okay. I know that was a *ton* of technical info. You might be thinking, “Great, all three of those advanced paths sound too complex or don’t apply to me.” And that’s perfectly fine!

Please do not think that real estate isn’t an amazing, tax-advantaged investment without these loopholes. It absolutely is. Even if you just buy a simple, long-term rental property and remain a “passive” investor, you still get two *huge* benefits.

- Tax-Free Cash Flow: That big “paper loss” from depreciation might be stuck in the passive bucket, but it can still work wonders. It can be used to offset the *rental income* (the cash flow) from the property itself.

Example: Your property brings in $10,000 in positive cash flow (profit) for the year. But your depreciation “paper loss” is $12,000. Your net *taxable* income from that property is -$2,000. You put $10,000 in your pocket, and on your tax return, it looks like you lost money. That’s $10,000 of tax-free income! - The Owner-Occupied Business Bonus: If you’re a business owner (Path 3) and you buy the building that your *own business operates out of*, that property is an *active part of your business*. All of its depreciation directly reduces your active business income. No special rules, no hoops to jump through.

Conclusion: Which Path Will You Build? 📝

We’ve laid out the map. We’ve shown you the “Great Wall” (the PAL rule) that the IRS builds to separate your Active and Passive income. And we’ve shown you the three paths to get around it:

- Path 1: Real Estate Professional (REPS): The “golden ticket” if you’re a full-time pro.

- Path 2: Short-Term Rentals (STRs): The “business loophole” for those who can meet the 7-day rule and materially participate.

- Path 3: The Corporate Strategy: A path for some business owners to offset *business* income.

And even if none of those fit, the “default” path of using depreciation to receive tax-free cash flow is a massive win that’s available to *everyone*.

Disclaimer: I have to say this—I am not your tax advisor, and this is not financial advice. The U.S. tax code is an absolute beast, and these strategies are complex and high-risk for audits. Before you *ever* attempt any of this, please, please talk to a qualified CPA who specializes in real estate.

I hope this helped demystify *how* these strategies work. What’s your biggest tax question or “ah-ha” moment from this? Let me know in the comments below! 😊