How to Maximize FAFSA Aid: A Guide to Countable vs. Non-Countable Assets

It’s one of the most stressful times for a parent. You’ve worked hard and saved diligently for your child’s future, only to find that those very savings might *penalize* you when it’s time to apply for college financial aid. You fill out the FAFSA (Free Application for Federal Student Aid) and suddenly, your responsible saving looks like a liability. I’ve heard this from so many families: “I have this cash saved up, but my financial advisor says I should move it to an annuity so it doesn’t affect my child’s aid. Is that true?”

It’s a fantastic question, and the answer dives deep into the logic of how federal aid is calculated. Let’s break down how FAFSA “sees” your money and what you can (and can’t) do about it. 😊

The video this post was based on discussed the **EFC (Expected Family Contribution)**. Please be aware that starting with the **2024-2025 FAFSA**, the EFC has been officially replaced by the **SAI (Student Aid Index)**. This was part of the FAFSA Simplification Act. While the core concepts of “countable” vs. “non-countable” assets discussed here are still generally valid, the underlying formulas and specific rules have changed. See the updated FAQ section for other major changes!

The Most Important Acronym: SAI (Formerly EFC) 📊

When you submit your FAFSA, the government uses a formula to determine your **Student Aid Index (SAI)**. This new number, which replaces the old “Expected Family Contribution” (EFC), is the magic number that colleges use to figure out your family’s “need.” The formula is simple:

Cost of Attendance – Your SAI = Your Financial Need

From this, you can see the simple truth: the **lower your SAI, the higher your financial need,** and the more aid (like grants, scholarships, and subsidized loans) you’re likely to be offered. Therefore, the entire strategy for maximizing FAFSA aid is about one thing: legally and ethically lowering your SAI.

The FAFSA formula calculates your SAI based on two primary factors: your **income** and your **assets**. For most families, the asset part is where the most confusion—and opportunity—lies.

The FAFSA Asset Test: What Counts Against You? 🤔

The FAFSA form will ask you to report the current value of your assets. But here is the critical part: FAFSA does **not** treat all assets equally. Some are “countable” (they raise your SAI) and some are “non-countable” (they are ignored).

Knowing the difference is the key to the entire strategy.

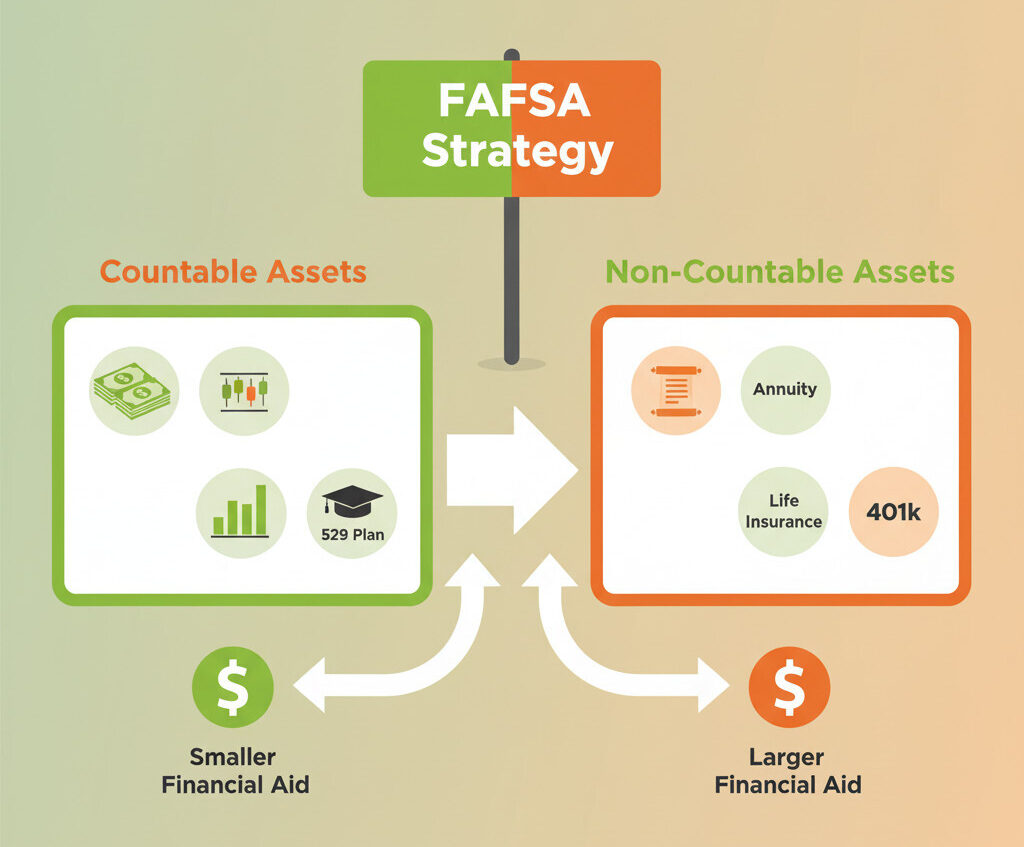

Countable vs. Non-Countable Parent Assets

| ❌ Countable Assets (Raise Your SAI) | ✅ Non-Countable Assets (Ignored by FAFSA/SAI) |

|---|---|

| Cash, Savings, & Checking Accounts | Your Primary Home (the house you live in) |

| Stocks, Bonds, Mutual Funds | Retirement Plans (401k, 403b, IRA, Pensions) |

| Rental Properties & Investment Real Estate | Life Insurance (the cash value of a policy) |

| 529 College Savings Plans (counted as a parent asset) | Annuities (non-retirement annuities) |

| CDs, Money Market Accounts, Trust Funds | Small Family Businesses (if you meet criteria) |

The strategy is *not* to get rid of your money. It’s to **move money from a “countable” column to a “non-countable” one.** That’s it. This is why the financial advisor suggested an annuity. By moving money from a “countable” savings account into a “non-countable” annuity, you are effectively making that asset invisible to the SAI formula.

What About the Income Test? 📝

The second piece of the puzzle is income. FAFSA looks at your income from your tax return (Form 1040). You can’t justdecide not to earn money, as that would be counter-productive. However, just like with assets, FAFSA is primarily concerned with *realized* income, not *unrealized* gains.

- Realized Income (Counts against you): This is money you actually received, like wages, interest from a savings account, dividends from stocks, or rental income. If you sell a stock for a profit, that’s a realized capital gain and it counts!

- Unrealized Gains (Generally Ignored): This is the *growth* of an asset that you haven’t sold yet. If your 401(k) grew by $20,000, that growth isn’t reported as income on your 1040.

This is the second benefit of assets like annuities and life insurance. During their “accumulation phase” (when they are just growing), that internal growth is **not** reported as income on your 1040. Therefore, the asset is both invisible and its growth is invisible, making it a double-win for lowering your SAI.

This is a critical disclaimer. This post is **not** financial advice on what makes the best *investment*. Stocks and mutual funds may have much higher returns over the long run than annuities or life insurance. This strategy is *purely* about FAFSA/SAI optimization. You might be trading potentially higher investment returns for a better chance at financial aid. You must weigh this trade-off with a qualified professional.

Conclusion: So, Is an Annuity a Good Idea for FAFSA/SAI? 📝

Based on the FAFSA/SAI rules, the financial advisor’s recommendation is a **valid strategy**. By moving a “countable asset” (like a large cash balance in a savings account) into a “non-countable asset” (like an annuity or the cash value of a life insurance policy), you are directly and legally lowering your SAI.

This strategy is most effective for families who have significant savings in countable accounts but whose income might still be low enough to qualify for aid *if* those assets weren’t counted. It’s a powerful planning tool that allows you to keep your hard-earned money while still presenting your family’s financial situation accurately (and favorably) to the federal aid system.

FAFSA/SAI Strategy Summary

Frequently Asked Questions ❓

Navigating the world of FAFSA can feel like a game, but knowing the new rules can make a huge difference. As always, this information is for educational purposes. Please consult with a qualified financial advisor who understands the new SAI rules to see what makes sense for your specific situation. If you have any more questions, feel free to ask in the comments~ 😊