The Real Reason Why 401(k) Offers Powerful Tax-Saving Benefits, Even Though You Pay Taxes Later

Let’s talk about something that I’m sure has crossed your mind. You’re doing the right thing, diligently putting money from every paycheck into your 401(k). You watch that balance grow, and it feels pretty good… right up until that nagging little voice in the back of your head whispers, “You know you’re going to have to pay taxes on all that, right?”

It’s a really common feeling. Is this whole 401(k) thing just a “tax trap”? Are we just kicking the can down the road, only to get hit with a massive tax bill in retirement exactly when we can’t afford it? It’s a scary thought, and to be honest, it’s a totally reasonable question to ask. You work hard for your money, and the idea of just handing a huge chunk of your life’s savings over to the government… well, it feels pretty deflating.

Today, we’re going to face that doubt head-on. We’ll break down why the 401(k) is not a scam, but instead, one of the most powerful and strategic wealth-building tools available to you. We’ll cover the math, a simple analogy that makes it all click, and the single most important action you need to take. Let’s get into it! 😊

The Big 401(k) Doubt: Is Tax Deferral Just a Trap? 🤔

The heart of the doubt is this: “Paying taxes now or paying taxes later… isn’t it all the same? In fact, what if I’m *losing*?”

This argument usually has a sophisticated-sounding part two. It goes something like this: “Hold on. If I invest in a *regular taxable brokerage account*, my long-term gains are taxed at lower capital gains rates (like 15% or 20%). But when I pull money out of my 401(k), it’s taxed as *ordinary income*, which could be 25%, 30%, or even higher! Am I actually getting a raw deal?”

This is a fantastic question. It shows you’re thinking critically about *how* your money is taxed. But this argument misses three crucial, game-changing advantages that a traditional, pre-tax 401(k) gives you. Let’s break them down one by one.

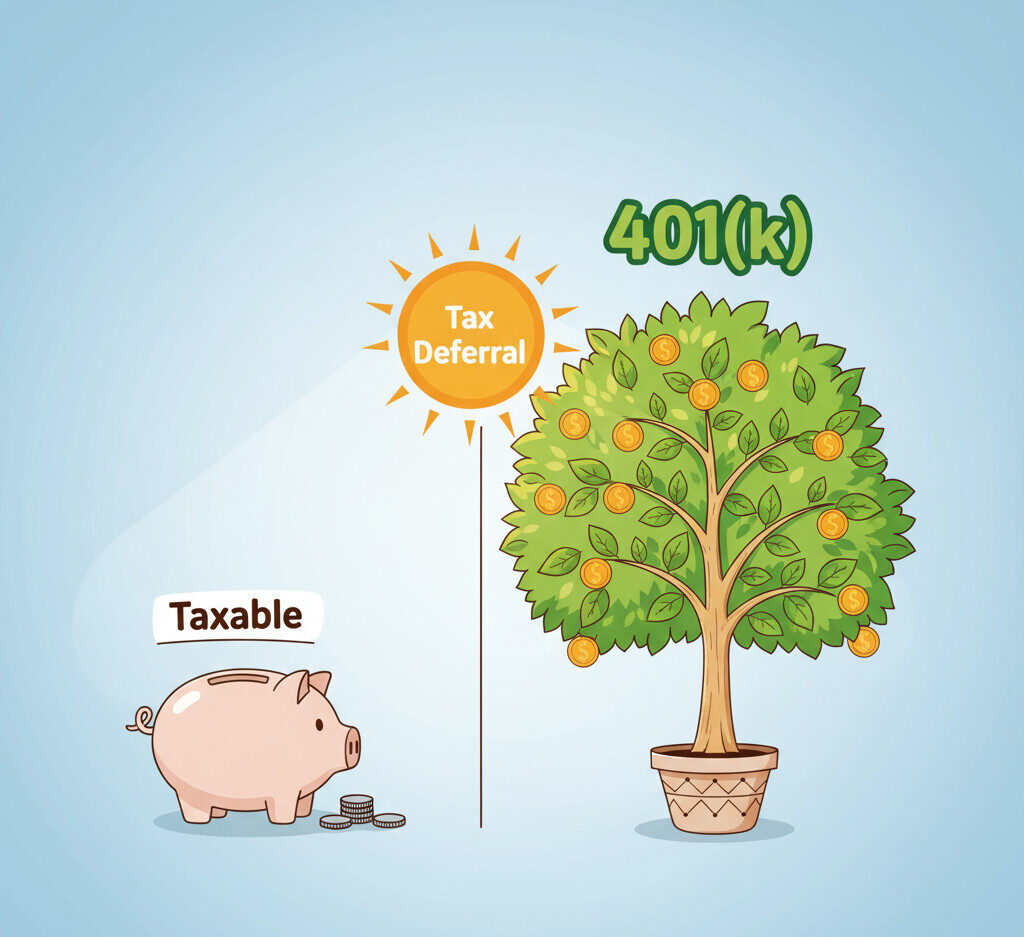

Answer #1: The Math (The Power of Pre-Tax Growth) 🧮

Feelings are one thing, but numbers don’t lie. The single biggest reason a 401(k) wins is that it lets you invest *more money* from day one. You’re not just investing your money; you’re investing the government’s money, too.

Let’s look at a simple side-by-side comparison. Imagine you have $5,000 of your income to invest, and your current combined federal and state tax rate is 25%.

Investment Growth: 401(k) vs. Taxable Account

| Feature | Scenario 1: Taxable Account | Scenario 2: Traditional 401(k) |

|---|---|---|

| Initial Income | $5,000 | $5,000 |

| Upfront Income Tax (25%) | -$1,250 (Paid immediately) | $0 (Tax is deferred) |

| Initial Investment | $3,750 | $5,000 |

| Investment Doubles Over Time | $7,500 | $10,000 |

| Taxes at Withdrawal | -$562.50 (15% capital gains on $3,750 gain) | -$2,500 (25% ordinary income on $10,000) |

| Final Take-Home Money | $6,937.50 | $7,500 |

Look at that! Even though you paid a *lower* tax rate (15%) in the taxable account, you still ended up with over $560 *less* than the 401(k), where you paid a *higher* tax rate (25%).

How is this possible? It’s not magic. It’s just compounding.

In Scenario 1, that $1,250 in tax money was taken away from you on day one. It was gone forever. In Scenario 2, that $1,250 was put to work *for you*. It was invested right alongside your own $3,750. That $1,250 *also* doubled, turning into $2,500. At the end, you paid the government its $2,500 (the original $1,250 you “borrowed” plus the $1,250 it earned), and you *still* came out ahead.

Answer #2: The Analogy (The Government’s Interest-Free Loan) 🏦

If the math made your eyes glaze over, don’t worry. Here’s a much more intuitive way to think about it that makes the whole concept “click.”

A traditional, pre-tax 401(k) contribution is essentially an **interest-free loan from the government, for decades.**

Think about it. In our example, by contributing $5,000 pre-tax, you avoided paying $1,250 in taxes *today*. The government is, in effect, letting you *borrow* that $1,250. What are the terms of this loan?

- Interest Rate: 0%.

- Loan Term: As long as you want, until you retire (up to 30, 40, or 50 years).

- Use of Funds: You *must* invest it and let it grow.

Who wouldn’t take that deal? You get to take the government’s money, invest it, keep all the profits it generates for yourself, and then just pay back the original “loan” (the tax) when you retire. That’s what tax deferral *is*. You are giving a bigger pile of money a longer time to grow, and that’s the undefeated champion of building wealth.

Answer #3: The Future Rate (The Tax Bracket Strategy) 📉

This brings us to the third, and maybe most strategic, piece of the puzzle. The doubt about 401(k)s often assumes you’ll pay the *same* 25% tax rate in retirement that you’re paying today.

But is that true? Think about your life’s income path. For most people, your peak earning years—and therefore your highest tax bracket—are right in the middle of your career, from your 40s to your 60s. This is when you’re contributing the most.

When you retire, your income usually *drops*. You’re no longer earning that high salary. You’re living off your savings, Social Security, and maybe a pension. This means you will very likely be in a *lower tax bracket* than you were during your peak years.

This is the 401(k) grand strategy:

- You get a tax *deduction* today, saving you money at your HIGH peak tax rate (e.g., 25%).

- You pay taxes *later* in retirement at your LOW retirement tax rate (e.g., 12% or 15%).

This strategy *assumes* your tax rate will be lower in retirement. If you are young, just starting your career, and expect your income (and tax rates) to be *much higher* in the future, you might consider a **Roth 401(k)**. With a Roth, you pay taxes now at your current, lower rate, and all your withdrawals in retirement (including all the growth!) are 100% tax-free.

Your 2025 Action Plan: Contribution Limits & The “Super Catch-Up” 🚀

So, now that we know *why* the 401(k) is so powerful, what can you do about it *this year*? The government wants you to save, so they set annual contribution limits. And for 2025, the news is great!

2025 Retirement Contribution Limits

| Account Type | 2025 Limit (Under Age 50) | 2025 Catch-Up (Age 50+) |

|---|---|---|

| 401(k), 403(b), TSP | $23,500 (Up from $23,000) | +$7,500 (Total $31,000) |

| Traditional IRA / Roth IRA | $7,000 (Unchanged) | +$1,000 (Total $8,000) |

There’s a brand-new rule kicking in this year thanks to the SECURE 2.0 Act. If you are age 60, 61, 62, or 63, your 401(k) catch-up limit isn’t $7,500. It’s $11,250! That means people in that specific age window can contribute a massive $34,750 total to their 401(k) in 2025. This is a huge opportunity to supercharge your savings right before retirement.

The Final Takeaway: Your 3-Step Investment Priority 🥇

Okay, I know that was a lot of information. If you’re feeling a bit overwhelmed and just want to know “What’s the *one* thing I need to do?”—I’ve got you covered. Financial advisors are almost unanimous on the smart order of operations. Think of it as your 3-step priority list.

The Smart Investment Priority List 📝

- Step 1: Get the FULL Company Match.

Before you do *anything* else (before paying off low-interest debt, before saving in an IRA, before *anything*), you MUST contribute enough to your 401(k) to get the 100% full company match. - Step 2: Max Out Tax-Advantaged Accounts.

After you’ve secured the match, your next goal is to work toward maxing out your tax-advantaged accounts. This means your 401(k) (up to $23,500) and your IRA (up to $7,000). - Step 3: Invest More Elsewhere.

If you’re one of the lucky few who has maxed out *both* your 401(k) and IRA and *still* have money to invest, this is when you open a regular taxable brokerage account and invest more.

I have to say this one more time. If your company offers a 100% match (e.g., “we match dollar-for-dollar up to 5% of your salary”) and you *don’t* contribute that 5%, you are literally turning down a **100% guaranteed, risk-free return** on your money. It is part of your salary that you are just leaving on the table. Please, don’t do that!

The 401(k) Power Play

Frequently Asked Questions ❓

• Traditional 401(k): You contribute with *pre-tax* dollars. This lowers your taxable income today. Your money grows tax-deferred, and you pay ordinary income tax on all withdrawals in retirement.

• Roth 401(k): You contribute with *after-tax* dollars. It doesn’t lower your tax bill today. Your money grows 100% tax-free, and all your qualified withdrawals in retirement are also 100% tax-free.

The 401(k) isn’t a trap; it’s a map. It’s a strategy that the government *wants* you to use to build your own financial future. You know the power of tax deferral and the simple, 3-step priority list.

The only real question left is: What’s your next move going to be? 😊