Real Estate Tax Saving: Cost Segregation + Bonus Depreciation

Have you ever had a great year—your income is growing, your business is thriving—but then you get your tax bill and feel like you’re on a treadmill? You’re working harder, but your tax burden is growing even faster, limiting your ability to reinvest and *really* grow your wealth. It’s a classic “good problem to have,” but let’s be honest, it’s still a problem! For high-income earners, this frustration is all too common. But what if there was a powerful, legal strategy that savvy real estate investors use to dramatically slash those tax bills? It’s called cost segregation, and it’s a game-changer. 😊

The “Paper Loss” Strategy: A (Legal) Tax Shelter 🤔

So, what’s this clever strategy? It revolves around creating something called a **”paper loss.”** Now, don’t let the word “loss” scare you. This has nothing to do with your property *actually* losing money or value. In fact, your cash flow can be fantastic!

A paper loss is a non-cash expense that reduces your taxable income, but doesn’t require any money to leave your pocket. The number one tool for creating this is **depreciation**.

If you qualify for what the IRS calls **”Real Estate Professional Status”** (which generally means you spend the majority of your working hours in real estate activities), you can use these paper losses from your properties to offset your *active* income. This means you can wipe out taxable income from your day job, your spouse’s job, or your other businesses. It’s incredibly powerful.

In simple terms, depreciation is the IRS’s acknowledgment that buildings and their components get old and wear out. To account for this, they let you “expense” or deduct a small piece of your property’s cost every single year. This deduction is the key to creating a paper loss.

The “Slow Burn” of Standard Depreciation 🐢

So, why doesn’t every property owner have massive paper losses? Because the *standard* way of doing depreciation is incredibly slow. The IRS has a very long timeline for how you deduct your property’s value.

When you buy a property, standard accounting lumps (almost) everything into one big bucket. This is where most investors leave a ton of money on the table without even realizing it.

Standard Depreciation Timelines

| Asset Type | Useful Life (Depreciation Period) |

|---|---|

| Residential Property (The building structure) | 27.5 Years |

| Commercial Property (The building structure) | 39 Years |

| Personal Property (Carpets, appliances, fixtures) | 5-7 Years |

The problem? Standard accounting forces you to depreciate the *entire* property (minus land value) over 27.5 or 39 years. This results in a tiny, almost insignificant, deduction each year. This is the “slow burn,” and it won’t create the meaningful paper loss you need to make a dent in your tax bill.

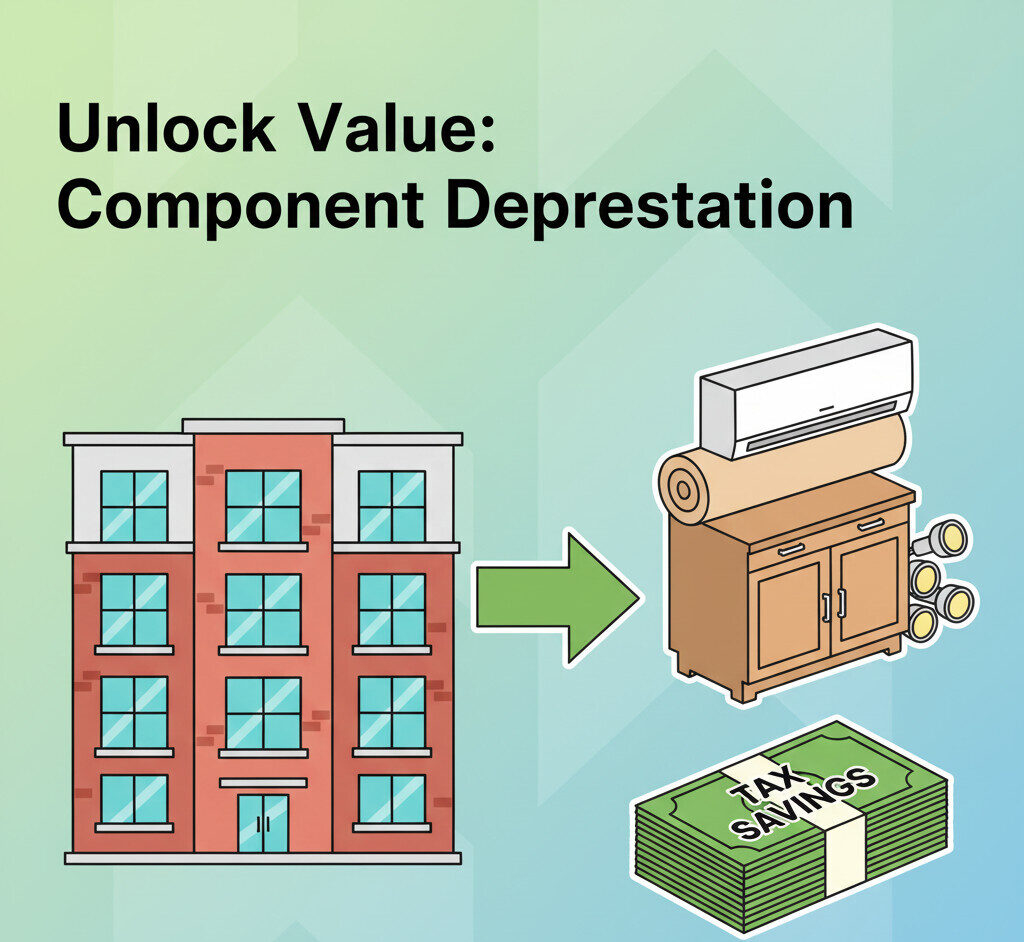

Accelerate! How Cost Segregation Unlocks Faster Deductions 🚀

This is where cost segregation changes everything. It’s a mindset shift. Instead of viewing your property as one single asset, you start to see it as a **collection of hundreds of smaller assets** all put together.

Think about it: is the carpet in your rental property really going to last 27.5 years? What about the kitchen cabinets, the light fixtures, or the specialty plumbing? Of course not! These are “personal property” assets, not structural building assets. Cost segregation is the tool that lets you legally prove this to the IRS.

This is a formal, engineering-based study where specialists “unbundle” your property. They go through it with a fine-tooth comb and identify all the components that can be legally reclassified from their long 27.5/39-year life into a much, much faster 5, 7, or 15-year depreciation schedule. This “front-loads” your depreciation deductions into the first few years of ownership.

Putting It Together: A Real-World Example 🧮

Let’s use some real numbers to see just how powerful this is. The difference is not small—it’s dramatic.

📝 Case Study: A $500,000 Residential Property

- Scenario 1: Standard Depreciation (The Slow Burn)

Using the standard method, your first-year depreciation deduction might be around $5,500. It’s something, but it’s not going to move the needle on a six-figure tax bill. - Scenario 2: With Cost Segregation (The Accelerator)

A cost segregation study identifies that $150,000 (30%) of the property’s value is actually 5-year personal property. By reclassifying this, your first-year deduction (using simplified math) jumps to around $30,000!

That’s a massive difference. You’ve just created a much larger paper loss to offset your other income, all from the same property. But… we’re not done yet. Now it’s time to add the “supercharger.”

The “Bonus Supercharger”: Taking Deductions to the Next Level ⚡

This is where the strategy gets truly incredible. There is a separate tax rule called **Bonus Depreciation** that you can layer *on top* of your cost segregation study.

Bonus Depreciation allows you to immediately deduct a large percentage of the cost of assets with a useful life of 20 years or less. This includes *all* those 5, 7, and 15-year assets your cost segregation study just identified!

For assets placed in service in 2023, the bonus depreciation rate is 80%. (Note: This percentage is scheduled to phase down in the coming years, so the urgency to act is high!)

Let’s look at our example one more time, but now with the supercharger.

📝 Case Study Part 2: Adding Bonus Depreciation

We have our $150,000 in 5-year assets from the cost segregation study. Thanks to 80% bonus depreciation, you can *immediately deduct 80% of that value in Year 1*.

Calculation: $150,000 (Reclassified Assets) × 80% (Bonus) = $120,000 Deduction

Final Tally (First-Year Deduction)

- Standard Method: $5,500

- Cost Segregation Only: $30,000

- Cost Segregation + Bonus: $120,000+

Just like that, you’ve legally created a massive paper loss of over $120,000 that can potentially wipe out an equivalent amount of your active income. This is how real estate investors can earn high incomes and pay significantly less in taxes.

The Real Long-Term Payoff: Is It Just Robbing Peter to Pay Paul? 🧐

Right about now, you’re probably thinking, “Okay, this sounds amazing, but aren’t I just borrowing deductions from the future? I take the deduction now instead of later, but the total amount is the same. Isn’t this just a timing game?”

That is an excellent and logical question. But the answer is a resounding **NO**. It is so much more than just a timing trick, for two very important reasons:

- The Time Value of Money: A dollar in your pocket today is worth infinitely more than a dollar you *might* get 20 years from now. By taking these massive deductions today, you are getting a huge, immediate tax refund. You can use that capital—which is effectively an **interest-free loan from the government**—to reinvest, buy another property, expand your business, or pay down debt. You’re using today’s tax savings to build more wealth *now*.

- Long-Term Tax Strategy: This strategy pairs beautifully with other advanced tax laws. When you eventually sell the property, you may owe “depreciation recapture” tax. However, you can use a **1031 Exchange** to roll your gains (and the tax liability) into a new, larger property, deferring the tax bill indefinitely. Even better, if you pass the property on to your heirs, they receive a **”step-up in basis,”** which can wipe out the depreciation recapture tax bill *permanently*.

Important Considerations Before You Start 👩💼👨💻

Before you jump in, there are two crucial things you need to know.

You can’t just guess at these numbers. To stand up to IRS scrutiny, a cost segregation study must be a formal, detailed report conducted by a qualified team of engineers and tax specialists. It’s a specialized service, but the return on investment is almost always massive.

Did you buy a property 3, 5, or even 10 years ago and never do this? Great news! You can conduct a cost segregation study **retroactively**. You don’t even have to amend your old tax returns. You can file a Form 3115 (“Application for Change in Accounting Method”) and take all the missed “catch-up” depreciation in *one lump sum* in the current year!

Conclusion: Unlock Your Property’s Hidden Potential 🔑

Cost segregation is more than just a tax loophole; it’s a fundamental shift in how you view your assets. It’s a powerful, established, and completely legal strategy that allows you to leverage the tax code to your advantage, unlock hidden capital in your properties, and accelerate your wealth-building journey.

It all comes down to one question: How might re-evaluating your assets unlock hidden potential in your portfolio? If you’re a real estate investor paying significant taxes, this is a question you can’t afford to ignore.

Key Summary: The Power of Cost Segregation

Frequently Asked Questions ❓

I hope this breakdown was helpful! It’s one of the most powerful tools in the real estate investor’s toolkit. If you have any questions, feel free to ask in the comments~ 😊