Joint Tenancy & Community Property Rules

I’ll bet that for most of us, our home is the single biggest asset we’ll ever own. It’s our slice of security, our family’s foundation. But what if I told you that just a few simple words on a piece of paper you signed years ago—or a seemingly generous gift from family—could be the difference between total financial security and a massive, heartbreaking family feud? It sounds dramatic, but it happens all the time.

Let’s look at a couple of *really* common situations that can go sideways, fast, if you don’t know the rules. Have you ever wondered about this? “My in-laws gave my spouse $1,000,000 for a down payment. We’re married, so the house is 50/50, right?” Or how about this one: “I co-own a house with my mom, and my name is on the title. When she passes, it just becomes all mine, right?” Don’t be so sure. The answers are probably not what you think, and getting them wrong can lead to some absolutely huge financial headaches down the road. Let’s dive in and break down what the law *actually* says. 😊

The $1M Gift: Community vs. Separate Property 💰

Let’s tackle that first “dream scenario.” Your in-laws are amazing and gift your spouse a cool million bucks to buy a house. You’re married, you find the perfect place, and you buy it together. It’s automatically 50/50 shared property, right? Well… maybe not. The answer hinges on a huge legal concept: Community Property vs. Separate Property.

This is a really big deal, and it’s all about *where the money came from*. First off, you need to know that property law varies wildly by state. In the U.S., only nine states are “community property” states (like California, Texas, and Washington). The other 41 states have different rules, often called “common law” or “equitable distribution” states. For this example, let’s pretend we’re in a community property state, as it’s the source of this common mix-up.

In community property states, the default setting is pretty simple. Think of your marriage as a business partnership. Any assets, income, or debts acquired *during* the marriage are generally considered to be owned equally by both spouses, 50/50. It doesn’t matter whose paycheck bought it; if it was earned or bought while you were married, it’s typically part of the “community.”

But—and you knew there was a “but” coming, right?—there’s a massive exception to this 50/50 rule. This exception is called Separate Property. So, what counts as separate?

- Any property or assets you owned *before* you got married.

- Any assets you receive as a *specific gift* addressed just to you, even if it’s during the marriage.

- Any assets you receive as an *inheritance* willed specifically to you.

Think of it like this: all the money you and your spouse earn during the marriage goes into a big “Community Pot” that’s 50/50. But a specific gift or inheritance given just to your spouse? That money *never even touches* the pot. It stays on the side, belonging 100% to them.

This brings us back to the $1M house. Because that $1,000,000 was a *specific gift* to your spouse, the law views that money as their separate property. And here’s the kicker: the house bought with that separate property money is *also* considered their separate property, not a 50/50 community asset. Yeah, surprising, isn’t it? (Note: If community funds are later used for the mortgage or upkeep, it can get commingled, but the initial ownership is based on the source of that down payment).

Co-owning with Mom: The “Joint” Ownership Trap 🤔

Okay, let’s switch gears and tackle that second puzzle—the one that happens all the time. You decide to buy a house with your mom, maybe to help her out. You have a brother and a sister, but hey, *your* name is on the deed right next to hers. You figure when your mom passes, the house just automatically becomes 100% yours. It seems logical. But this is one of the most dangerous assumptions in property law.

The problem is that the word “joint” on a deed can mean a couple of very, *very* different things, with totally different outcomes. The two most common forms are Joint Tenancy and Tenancy in Common.

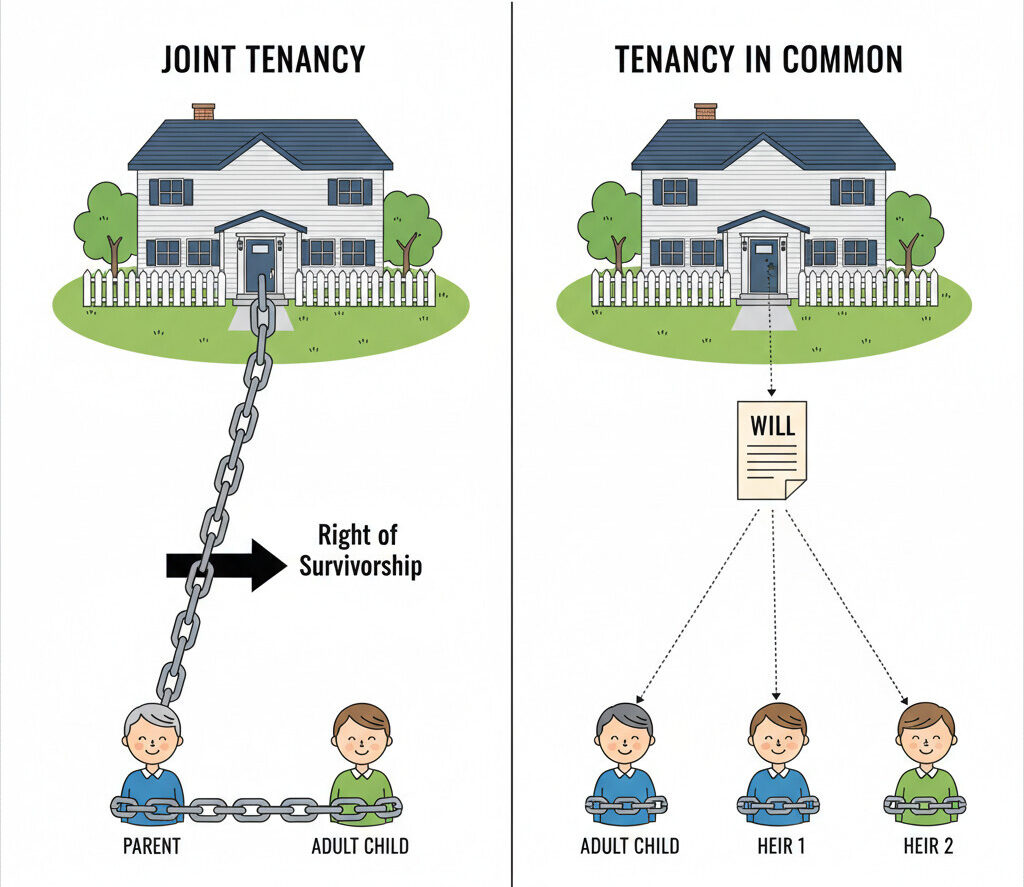

1. Joint Tenancy (What You *Think* You Have)

This is what most people, like in the scenario with mom, *think* they’re setting up. Joint tenancy has a powerful, magical feature that’s built right in. The magic words are the “Right of Survivorship.”

This right is totally automatic. It means that when one owner (your mom) passes away, their share of the property instantly and automatically vanishes and transfers to the other surviving owners (you). It doesn’t go through probate court. It doesn’t matter what your mom’s will says. The deed itself acts as the final word, making you the sole owner.

2. Tenancy in Common (What You *Probably* Have)

This is the other, and in many cases, the *default* form of co-ownership. A tenancy in common is a whole different ball game. In this setup, each owner (you and your mom) holds a separate, distinct share of the property. It’s almost like owning stock in a company. You each own your 50% (or 30/70, or whatever you decide).

Here’s the critical difference: there is NO right of survivorship. When your mom passes away, her 50% share *does not* automatically go to you. Instead, her share becomes part of her estate. It’s an asset that will be distributed according to her will (or by state law if she doesn’t have one). This means her 50% share will likely be split between *all* her heirs—which would include you, your brother, and your sister.

Comparison: Joint Tenancy vs. Tenancy in Common

Believe me, the difference here is absolutely everything. Let’s look at it side-by-side:

| Feature | ✅ Joint Tenancy | ❌ Tenancy in Common |

|---|---|---|

| Right of Survivorship? | Yes. This is the defining feature. | No. This is the critical difference. |

| What happens at death? | Owner’s share goes *automatically* to the other co-owner(s). Bypasses the will. | Owner’s share goes to their *estate* to be passed to heirs via a will or probate. |

| Are shares equal? | Yes, shares must always be equal. | No, shares can be unequal (e.g., 60/40). |

The Devil’s in the Details: A Common, Costly Mistake 📋

So, why doesn’t everyone just get a joint tenancy and call it a day? This leads us to the super common and super expensive mistake people make all the time. The thinking goes something like this: “I already own my home. To make things simple when I’m gone, I’ll just add my daughter’s name to my existing deed to create a joint tenancy.”

It feels smart. It feels easy. But legally, it’s a total trap. And here’s why it completely backfires.

The law is incredibly picky about creating that powerful Right of Survivorship. You can’t just declare it. To have a valid joint tenancy, the law in most states requires you to meet four very strict conditions, which lawyers call the “Four Unities (TTIP).”

The Four Unities (TTIP) 📝

For a joint tenancy to be valid, all owners must:

- Time: All owners must acquire their interest *at the exact same time*.

- Title: All owners must be on the *exact same deed/document*.

- Interest: All owners must have *equal shares* (e.g., 50/50 for two people, 33/33/33 for three).

- Possession: All owners must have an *equal right to possess* and use the entire property.

Now you can see exactly why the “let me just add a name” trick fails. When a parent who already owns a home adds their child to the deed later, they instantly violate the Four Unities:

- They violate the Unity of Time (the parent got their interest years ago; the child is getting it today).

- They often violate the Unity of Title (it’s a second, new document, not the original one).

When these unities are broken, the law just says, “Nope, that’s not a joint tenancy.” And what does it default to? You guessed it: a Tenancy in Common. This completely wipes out the automatic survivorship the parent wanted in the first place. The parent, thinking they made their daughter the sole inheritor, has *actually* just guaranteed that their 50% share will go to their estate and be split among all their heirs. It’s the exact opposite of what they intended.

Your Title, Your Future: Getting It Right 👩💼👨💻

So, what does this all boil down to? It’s one critical point: the way your property is titled isn’t just boring paperwork. It’s a set of legal commands that literally dictates the future of that asset and can control where hundreds of thousands, or even millions, of dollars go.

Let’s apply this and give the definitive answers to our two scenarios.

Case Study: The Final Verdict 📚

Scenario 1: The $1M Gift

- The Situation: In-laws gift $1M specifically to the husband, who uses it for a down payment on a house during the marriage.

- The Result: That $1M is a *gift*, making it the husband’s separate property. The house bought with those funds is also considered his separate property, *not* 50/50 community property (barring other commingling factors).

Scenario 2: The Co-owned House with Mom

- The Situation: A daughter co-owns a house with her mom. She has two other siblings. She assumes the house is all hers when her mom passes.

- The Result: It depends *entirely* on the deed’s exact wording.

- If the deed *explicitly and correctly* created a Joint Tenancy with Right of Survivorship (meeting the Four Unities), then yes, the daughter automatically becomes the 100% owner.

- If not (or if it was created by “adding her name later”), it’s almost certainly a Tenancy in Common. Mom’s 50% share goes to her estate and will be split among *all three children* (the daughter and her two siblings).

The bottom line is this: those few words on your property title—“as Joint Tenants with Right of Survivorship” versus “as Tenants in Common”—are not just legal mumbo jumbo. They are powerful instructions that can absolutely change a family’s financial future.

Conclusion: Don’t Assume, Check Your Deed 📝

This really just leaves one final, and maybe the most important, question. And this one isn’t for me; it’s for you.

Do you know exactly how you own your property?

Don’t just assume you know. I seriously encourage you to pull out the deed to your home and read the exact language. Do you see the words “Joint Tenancy with Right of Survivorship”? Do you see “Tenants in Common”? Or (in some states) “Community Property with Right of Survivorship”? Finding out now and fixing it if it’s wrong is a whole lot less painful, and a lot cheaper, than having your family fight over it and figure it out later.

I hope this clears up some major confusion! Property law is tricky, but knowing these basics can save you and your loved ones a world of trouble. If you have any questions or your own “whoops” story, feel free to share in the comments~ 😊