FASB ASU 2026-01: PIK Dividends on Preferred Stock Explained

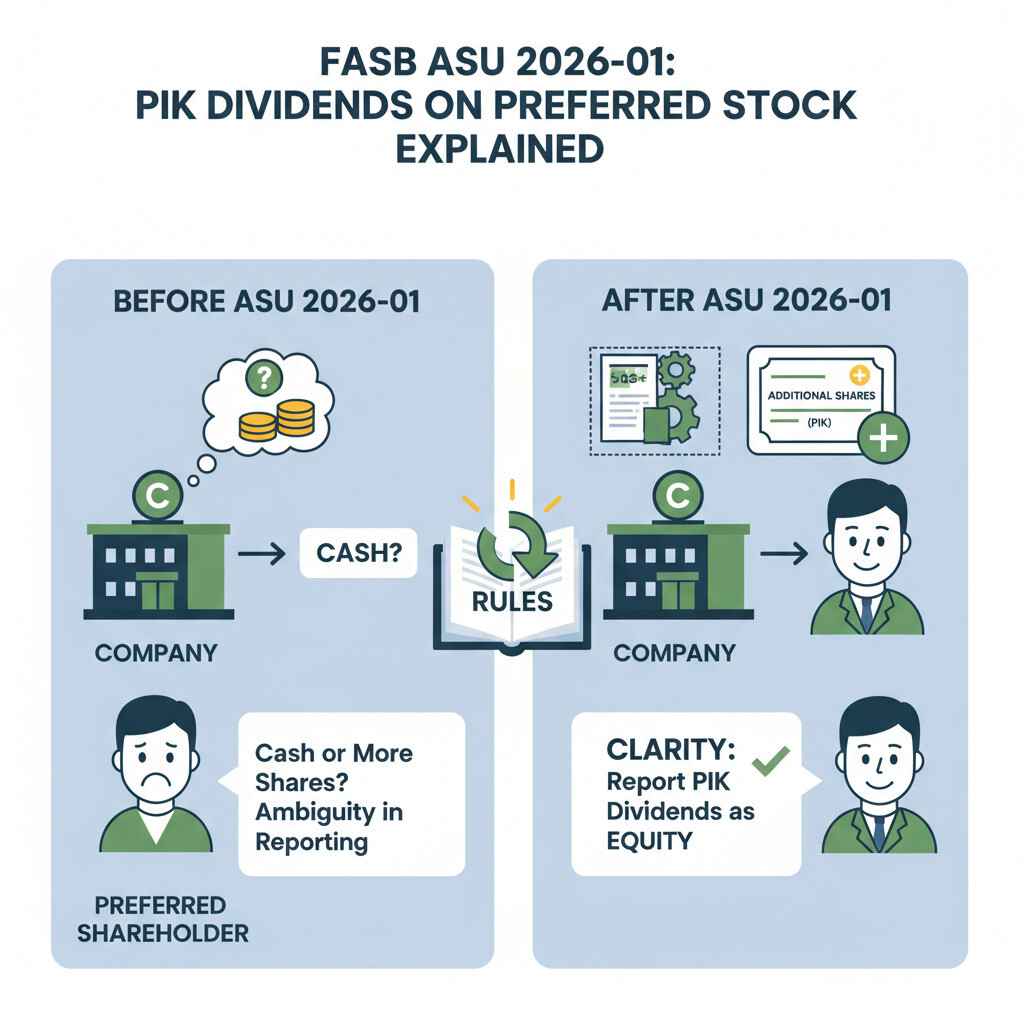

If your company has issued preferred stock that pays dividends “in kind” — more preferred shares or added liquidation value instead of cash — FASB ASU 2026-01 directly affects your equity accounting and your earnings-per-share math. This guide explains what PIK dividends are, the diversity-in-practice problem the FASB closed, the new rate-based measurement, the EPS impact, and the effective date and transition options.

At SW Accounting & Consulting Corp, we help Los Angeles area companies — especially venture- and private-equity-backed issuers with complex capital structures — apply new FASB guidance correctly. Below: the standard, the mechanics, and what to do before it takes effect.

What is a PIK dividend? 🪙

A paid-in-kind (PIK) dividend is a dividend paid not in cash, but “in kind” — typically by issuing additional preferred shares or by increasing the preferred stock’s liquidation value. Think of it like a savings account that pays interest by adding to the balance instead of cutting you a check.

PIK features are common in:

- Venture- and PE-backed companies — preferred stock with cumulative PIK dividends that compound until a liquidity event.

- Structured financings — instruments designed to preserve cash while still accruing a return to preferred holders.

- Distressed or growth situations — where conserving cash matters more than current distributions.

What problem did ASU 2026-01 solve? 🤔

Before this Update, U.S. GAAP did not address how an issuer should INITIALLY MEASURE a PIK dividend on equity-classified preferred stock. Stakeholders flagged the gap, and diversity in practice emerged — different issuers measured the same economic event differently, distorting comparability.

Why the gap mattered:

- Balance sheet effect — the measurement drives the carrying amount of equity-classified preferred stock on the statement of financial position.

- EPS effect — for entities that report earnings per share, PIK dividends reduce income available to common shareholders, so the measurement flows directly into EPS.

- Comparability — without a rule, two companies with identical preferred terms could report different numbers, undermining investor analysis.

What is the new measurement rule? 📐

Under ASU 2026-01, an issuer initially measures a PIK dividend on equity-classified preferred stock based on the PIK dividend RATE stated in the preferred stock agreement — not at fair value.

If the preferred stock agreement says PIK dividends are calculated by multiplying the PIK dividend rate by the liquidation value of the preferred stock outstanding, the issuer initially measures the PIK dividend at exactly that amount — the contractual rate applied to the liquidation value. The liquidation value (or liquidation preference) is the amount, defined in the agreement, that the preferred holder would receive on liquidation. The measurement follows the contract, which is simpler and more consistent than estimating fair value each period.

Two important boundaries:

- Initial measurement only — the amendments address HOW MUCH to record at initial measurement, using the stated rate.

- Recognition timing unchanged — the Update does NOT change WHEN an entity recognizes PIK dividends; existing guidance on timing still governs.

- Scope — equity-classified preferred stock (the amendments sit in Subtopic 505-10, Equity—Overall).

When is it effective, and how do you transition? 📅

The amendments are effective for all entities for annual reporting periods beginning after December 15, 2026, and interim periods within those annual periods. Early adoption is permitted in any interim or annual period for which financial statements have not yet been issued or made available for issuance.

| Item | Detail |

|---|---|

| Effective date | Annual periods beginning after December 15, 2026 (and interim periods within) |

| Early adoption | Permitted, if financial statements not yet issued/available |

| Transition options | (1) Prospective, OR (2) modified retrospective for equity-classified preferred stock outstanding at adoption |

| Interim adoption | Apply as of the beginning of the annual period that includes the interim period |

Who should pay attention — and what to do now 🛠

Any issuer with equity-classified preferred stock that pays PIK dividends should assess the impact before the effective date — especially companies reporting EPS.

- Inventory your preferred instruments — identify equity-classified preferred stock with PIK features and pull the stated PIK rate and liquidation-value definitions from each agreement.

- Compare to current practice — determine whether your existing measurement differs from the new rate-based approach, and quantify the difference.

- Model the EPS effect — if you report EPS, recompute income available to common shareholders under the new measurement.

- Choose a transition method — prospective vs. modified retrospective; model both and document the election.

- Consider early adoption — if it improves comparability or simplifies your close, and statements aren’t yet issued.

Frequently asked questions about ASU 2026-01

No. The Update addresses only INITIAL MEASUREMENT (how much), using the stated PIK rate. It does not change the timing of when an entity recognizes PIK dividends.

No. The amendments require measurement based on the PIK dividend rate stated in the preferred stock agreement (e.g., the rate applied to liquidation value), not fair value.

The amendments address equity-classified preferred stock (Subtopic 505-10). Instruments classified as liabilities follow other guidance — assess classification first.

Annual periods beginning after December 15, 2026 (and interim periods within). Early adoption is permitted if financial statements haven’t yet been issued or made available, using either prospective or modified retrospective transition.

How can SW Accounting help? 💼

At SW Accounting & Consulting Corp, we help LA-area issuers with complex capital structures adopt ASU 2026-01 — inventorying equity-classified preferred stock with PIK features, mapping each agreement’s stated rate and liquidation-value terms to the new measurement, modeling the EPS impact, selecting and documenting a transition method, and coordinating with auditors. If you have PIK preferred outstanding, let’s quantify the change before the effective date.

📩 Schedule an ASU 2026-01 readiness review

Disclaimer: This article is for informational purposes only and is not accounting, tax, or legal advice. Always consult a qualified professional regarding your specific facts. Primary source: FASB Accounting Standards Update No. 2026-01, Equity (Topic 505): Initial Measurement of Paid-in-Kind Dividends on Equity-Classified Preferred Stock (April 2026); FASB Accounting Standards Codification Subtopic 505-10.