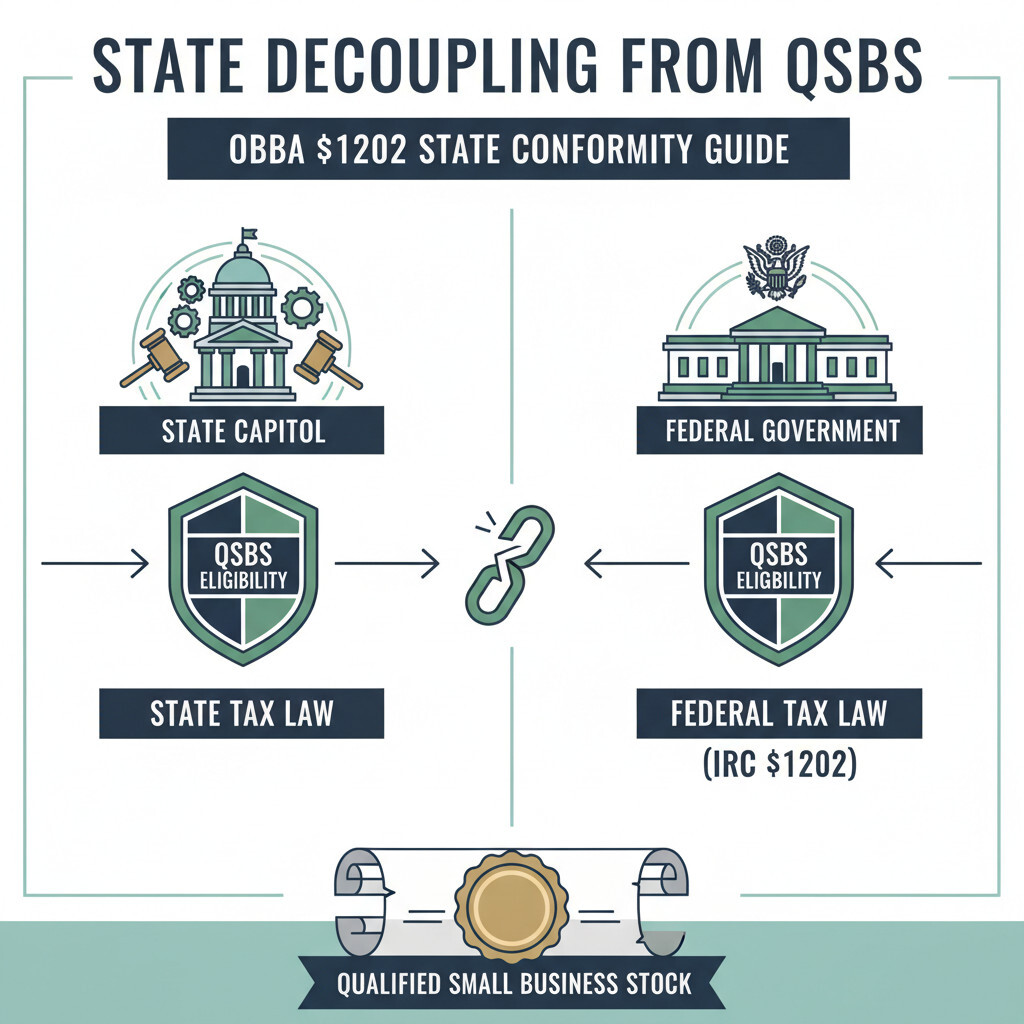

State Decoupling from QSBS: OBBBA §1202 State Conformity Guide

Recent federal tax policy has leaned hard into generous, often permanent incentives — and QSBS is the headline example, letting founders and early investors potentially eliminate federal tax on millions in gains. But state decoupling from federal tax rules has turned “do I qualify federally?” into only half the question. The other half: does my state conform — and if not, how much of the benefit survives?

At SW Accounting & Consulting Corp, we advise Los Angeles area founders, early-stage investors, and family offices on the after-tax reality of federal incentives once state conformity is factored in. Below: what OBBBA changed for QSBS, why states are decoupling, which states have acted, and how conformity risk reshapes planning — especially for California residents.

What is QSBS, and what did OBBBA change? 📈

Qualified Small Business Stock (QSBS) under IRC §1202 lets eligible holders of qualifying domestic C corporation stock exclude a large portion of capital gain from federal tax. OBBBA (Pub. L. No. 119-21) meaningfully expanded the benefit — raising exclusion caps and adding flexibility around holding periods and capital raises.

Core federal QSBS mechanics (post-OBBBA):

- Exclusion amount — permanently excludes the greater of $10 million (or $15 million for more recently issued stock) OR 10× the taxpayer’s basis, from federal capital gains tax on qualifying stock. The exact figure depends on when the stock was issued.

- Holding period — the long-standing five-year holding requirement continues for stock acquired on or before the relevant OBBBA date; OBBBA adds tiered flexibility for newly issued stock.

- Eligibility reopened — OBBBA expands eligibility for many scaling companies and adds flexibility around capital raises, equity compensation, and exit planning.

- Qualifying stock — must be domestic C corporation stock meeting the §1202 active-business and gross-asset tests.

QSBS can permanently eliminate federal capital gains tax on a qualifying exit — but the state where you live and pay tax may not honor the exclusion at all. For a California founder, the federal §1202 exclusion does NOT carry over to California tax. Run the after-state-tax number before you assume the headline federal benefit.

Why are states decoupling? ⚖️

States are no longer automatically adopting federal tax rules. Federal incentives like QSBS reduce a state’s own tax base if the state conforms — so states increasingly take a provision-by-provision approach, choosing which federal benefits to honor and which to “decouple” from (add back for state purposes).

QSBS is the flashpoint, but it is not alone. States are applying selective conformity to multiple major federal incentives:

- QSBS / §1202 exclusion — the most visible and economically consequential post-OBBBA divergence.

- Qualified Opportunity Funds (QOZ) — state treatment of deferred/excluded gains varies.

- Bonus depreciation — many states cap or disallow federal bonus depreciation, requiring add-backs.

- Research & experimental (R&E) expensing — state conformity to federal R&E treatment is inconsistent.

Which states have decoupled from QSBS? 🗺

State QSBS treatment now spans full conformity, partial conformity, and outright decoupling. The map is shifting — what was a quiet conformity question is now active legislation.

| State | QSBS treatment | Authority |

|---|---|---|

| California | Taxes QSBS gains (no §1202 exclusion for CA purposes) — long-standing | Cal. Rev. & Tax. Code §§17024.5(a)(1)(E), 18038.5(a)(1)(E) |

| Maine | Enacted decoupling from the federal QSBS exclusion | Me. Rev. Stat. tit. 36, §5122(1)(UU) |

| Oregon | Enacted decoupling from the federal QSBS exclusion | Or. Rev. Stat. §316.047 |

| Washington / D.C. | Decoupling efforts surfaced (D.C. measure subject to Congressional review) | D.C. Code §47-1803.03(a)(4)(A) |

| New York | Proposed taxing federally-excluded QSBS gains (ultimately withdrawn) — signal of direction | Withdrawn proposal |

California does not conform to the §1202 QSBS exclusion, full stop. A California-resident founder selling qualifying stock owes California tax on the gain even when the federal tax is zero. Planning levers — residency timing relative to the sale, trust structures (e.g., non-grantor trusts in non-taxing states), and entity domicile — must be evaluated WELL before the liquidity event, not after.

How does conformity risk reshape planning? 🧭

QSBS eligibility is only half the analysis. A taxpayer’s state of residence — and whether that state conforms — can be just as consequential as federal qualification. The after-tax value of any federal incentive must be modeled at the state level.

Planning implications:

- Model the after-state-tax outcome — federal QSBS savings are real regardless of state, but state conformity materially changes the net benefit, especially in high-tax states.

- Residency planning — for founders nearing a liquidity event, the timing and bona fides of a residency change can significantly affect state tax — but must be done correctly and early.

- Trust structuring — non-grantor trusts situated in non-taxing states are a common planning tool, but carry their own complexity and must be established well in advance.

- Multi-incentive review — apply the same conformity check to QOZ, bonus depreciation, and R&E expensing; don’t assume any federal benefit flows through to your state return.

Frequently asked questions about state decoupling and QSBS

No. California taxes QSBS gains and does not provide the §1202 exclusion for state purposes (Cal. Rev. & Tax. Code §§17024.5, 18038.5). A California resident owes California tax on QSBS gain even when federal tax is zero.

It means a state chooses NOT to follow a specific federal tax provision. For QSBS, a decoupling state adds back the federally-excluded gain so it is taxed at the state level — even though the IRS excludes it.

Maine (Me. Rev. Stat. tit. 36 §5122(1)(UU)) and Oregon (Or. Rev. Stat. §316.047) have enacted decoupling. Washington and D.C. have seen efforts; New York proposed and then withdrew a measure. California has long taxed QSBS gains.

Yes. States apply selective conformity to Qualified Opportunity Funds, bonus depreciation, and R&E expensing as well. Always check state treatment before relying on the after-tax value of any federal incentive.

How can SW Accounting help? 💼

At SW Accounting & Consulting Corp, we model the true after-tax value of federal incentives once state conformity is factored in — QSBS §1202 analysis for California residents, residency and trust-structuring evaluation ahead of liquidity events, and multi-incentive conformity review (QOZ, bonus depreciation, R&E). For founders and investors, we help you avoid the surprise of a state tax bill on a gain you thought was tax-free.

📩 Schedule a QSBS state conformity review

Disclaimer: This article is for informational purposes only and is not legal or tax advice. Always consult a qualified professional regarding your specific facts. Primary sources: Internal Revenue Code §1202; One Big Beautiful Bill Act (Pub. L. No. 119-21); Cal. Rev. & Tax. Code §§17024.5, 18038.5; Me. Rev. Stat. tit. 36 §5122(1)(UU); Or. Rev. Stat. §316.047; D.C. Code §47-1803.03(a)(4)(A).