Can you deduct your college-aged child’s tuition as a business expense? You can receive both tax credits and expense deductions.

If you’re a small business owner with kids, you know this feeling all too well. You’re trying to figure out your taxes, but you’re also staring down this absolute *mountain* of college costs. And it always seems to happen at the worst time, right? The moment those massive tuition bills start rolling in, the child tax credits you’ve been relying on suddenly disappear.

It can feel like you’re caught in a financial vise. This leads to the big question that so many of us ask: Can I actually use my business to solve both problems? Is there a smart, legal, and legitimate way to turn those education costs into a business deduction and ease some of that pressure? Let’s find out. 😊

The Foundational Strategy: Hiring Your Child 👩💼👨💻

Before we even get to tuition, we have to start with the foundational strategy that almost every family business should consider: putting your kids on the payroll.

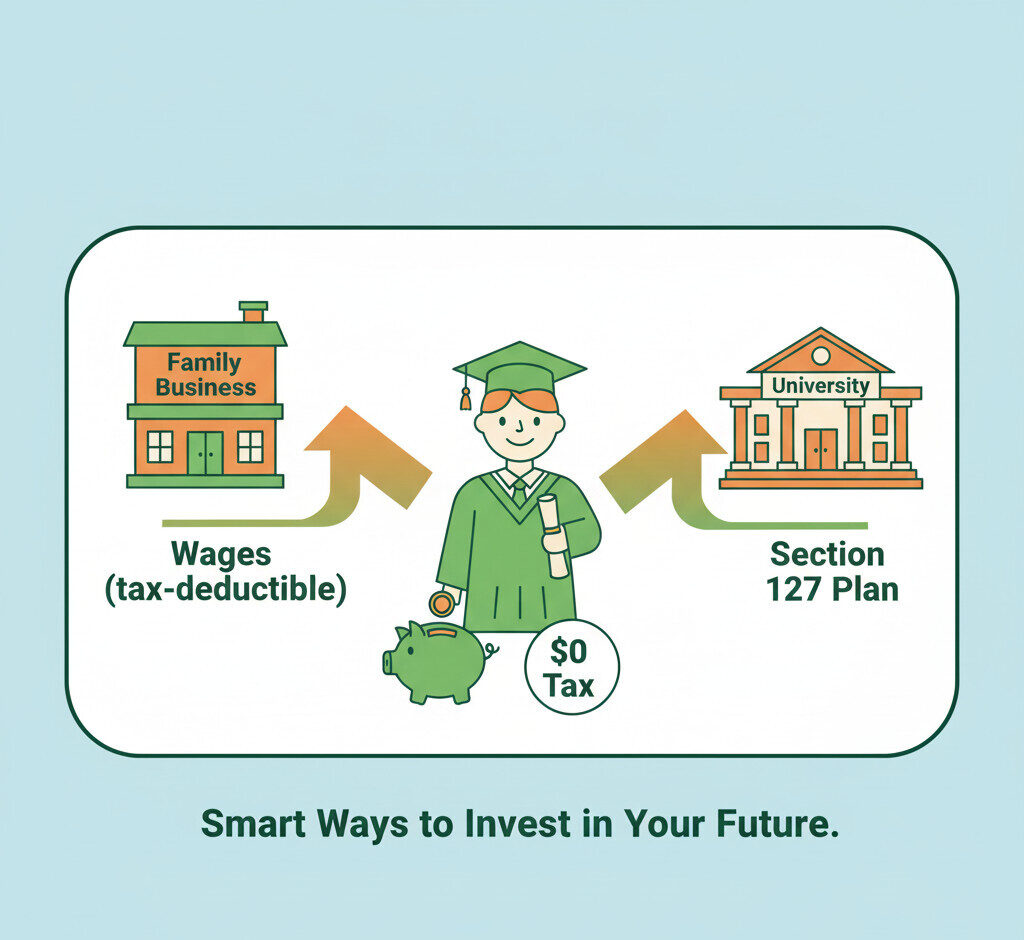

This is often the simplest, most direct way to start shifting income from your high tax bracket to your child’s (likely non-existent) tax bracket. This one move can cut down your overall family tax bill significantly. But to do it right, it can’t be an “allowance.” It has to be real.

This is the most important rule. You can’t just “pay” your child. You must hire them to do real, legitimate work for the business. This could be social media management, cleaning the office, filing, updating the website—whatever it is, it must be appropriate for their age and skills, and you must pay them a reasonable wage for that work.

When you do this, a wonderful tax-shifting event occurs. Let’s look at an example.

A Practical Example: Shifting $26,000 of Income 📊

Let’s meet a family running a great little business. After all their normal expenses, their business has a net income of $100,000. This $100k is the profit the IRS is going to tax.

Step 1: The Business Side (The Deduction)

The family hires their two children to do legitimate work. They decide to pay each of them a salary of $13,000 for the year. This $13,000 figure is very strategic, as we’ll see in a moment.

Look at what happens to the business’s profit immediately:

📝 Business Profit Calculation

Initial Net Income: $100,000

New Salary Expense (2 children x $13k): -$26,000

New Taxable Profit: $74,000

Just like that, the business has $26,000 in new, legitimate salary expenses, and its taxable income drops from $100,000 to $74,000. That’s a huge chunk of taxable income that just vanished.

Step 2: The Child’s Side (The Standard Deduction)

“Okay,” you’re thinking, “great for the business, but don’t the kids have to pay taxes on that $13,000 now?”

Nope! And this is the magic. In the U.S., every single person gets a “standard deduction” on their income. For 2024, the standard deduction for a single person is $14,600. The $13,000 salary in the example is strategically chosen to be *less* than this amount.

Since each child earned $13,000, they can use their *own* standard deduction to completely wipe out that income on their tax return.

The bottom line? Their taxable income is $0. They don’t owe a dime in federal income tax.

Let’s step back. The family is still using that $26,000 for the kids’ expenses—car, food, college savings, etc. But by structuring it as a salary for real work, they’ve effectively taken $26,000 from the parent’s high-tax bracket and moved it to the kids’ $0 tax bracket. The family’s overall cash flow hasn’t changed, but their *taxable income* has been reduced by $26,000.

The *Second* Win: Saving on Self-Employment Tax 🧮

The income tax savings are fantastic, but believe it or not, that might not even be the best part. For many small businesses, there’s *another* huge layer of savings you can get on top of that: the Self-Employment Tax.

Here’s the deal: If your business is a sole proprietorship or an LLC taxed as one, and your child is under 17 years old, the wages you pay them are completely exempt from that huge 15.3% FICA tax (Social Security and Medicare). This is a massive, massive bonus.

This is truly an “extra cherry on top” for hiring younger kids. Now, if your child is 18 or older, don’t worry! You *still* get all of those awesome income tax benefits we just talked about. You’ll just have to pay the standard payroll taxes, which is still a great deal. This FICA exemption is just a special perk for those with kids under 17.

The Big Question: Can Your Business Pay for College Tuition? 🎓

Hiring your kids is a total no-brainer. But now, let’s get back to that bigger, more ambitious question: Can the business *directly* pay for their college tuition and write it off?

The short answer is… it’s complex, but in many cases, yes! The good news is the IRS does have established programs that let businesses pay for their employees’ education. And your child, as a legitimate employee, can qualify for these programs.

But—and this is a really big but—there are two main ways to do this, and they have very, very different rules. Picking the wrong one can get your entire deduction thrown out, so you absolutely have to know the difference.

Two Programs, One Goal: A Head-to-Head Comparison ⚖️

Let’s put these two programs right next to each other. This is where the details really matter if you want to stay on the right side of the IRS.

| Program | Benefit Limit | Works for College? | Key Requirement |

|---|---|---|---|

| Working Condition Fringe Benefit | No Dollar Limit | Generally No | For skills for the *current* job. |

| Section 127 Plan (Educ. Assistance) | $5,250 / Year | Yes | A formal, written policy. |

At first glance, that top one, the “Working Condition Fringe,” looks amazing—no dollar limit! But here’s the trap: the education *must* be for skills needed in the employee’s *current* job. The IRS has ruled over and over that a general college degree (like a B.A. in English or History) does *not* qualify.

That’s why we are going to focus on the second one: the Section 127 Plan. This is the one that is actually designed to work for college tuition.

Deep Dive: How the Section 127 Plan Works 📝

The $5,250 “Magic Number”

This is the magic number you need to remember: $5,250. Under a formal Section 127 Educational Assistance Plan, your business can provide up to $5,250 per year, per employee, for education.

And here’s the double win:

- It is 100% deductible for the business.

- It is received completely tax-free by your child (the employee).

It’s a perfect tax scenario. But, to use this awesome benefit for your *own* child, you know the IRS is going to have some strict rules.

The Rules for Your *Own* Child (The 3 Checkpoints)

You can’t just give this benefit to your kid and no one else. The plan can’t discriminate. And to make sure it’s all above board when applied to your own family, the IRS has three specific checkpoints your child must pass:

To receive the Section 127 benefit, your child must:

- Be at least 21 years old.

- NOT be claimed as a dependent on your tax return. (They must be filing as an independent adult).

- NOT be a major owner of the business (owning more than 5%).

Your Action Plan: How to “Stack” Your Benefits (Legally) 🚀

So, we have the hiring strategy. And we have the tuition payment plan. How do we make them work together to get the absolute maximum benefit?

First, we have to talk about a super important tax principle: No “Double-Dipping.” The IRS is very clear about this. You can’t use the *exact same dollar* you spent to get two different tax breaks. For example, you can’t pay $5k for tuition, deduct it as a business expense, *and* also claim a personal tax credit for that very same $5k payment.

But… that doesn’t mean we can’t be strategic! This is how you *legally stack your benefits*.

Here is the 3-step play. It’s beautiful.

- Step 1: Pay Tuition. Your company pays the *first $5,250* of your child’s tuition using its formal, written Section 127 plan.

- Step 2: Get Deduction. That $5,250 is now a business expense (a deduction for the company) and is 100% tax-free to your child.

- Step 3: Claim Credits. For all the tuition costs *above* that $5,250 (say, the next $4,000), you, the parent, pay that amount personally. You can then claim personal education credits, like the American Opportunity Tax Credit (AOTC), on that *remaining* balance.

Conclusion: It’s an “And,” Not an “Or” 📝

This isn’t about replacing the tax strategies you already use. This is about taking the credits you already know about and then leveraging your family business to add a powerful new layer of tax savings right on top. It’s an “and,” not an “or.”

We’ve seen how hiring your child can shift income to a $0 tax bracket and how a Section 127 plan can turn a non-deductible college bill into a 100% deductible business expense. These are significant, IRS-approved tax savings.

This leaves just one final question to think about: Is your business structured in a way that lets you take full advantage of these strategies? Because having the right structure is the foundation that unlocks these powerful financial tools. If you have any more questions, feel free to ask in the comments~ 😊